The housing crash we had to have: A Gen Y perspective on the bubble

A weekend guest cross-post from Rational Radical

So bubble mania has finally hit the mainstream. The housing bubble question has landed squarely at the feet of the Prime Minister and his treasurer, and only 10 to 15 years late… What a relief it is then to hear our fearless leaders assure us that there is no bubble, endless house price rises are universally a good thing, and that only poor people try to live in houses they can’t afford.

Yet despite their best efforts, Hockey and Abbott cannot pull the veil back down over the hideous monster that is Australia’s 16 year long housing bubble. That veil has now been permanently lifted. The cat is out of the bag and roaming the remorseless realms of the internet meme, destined to immortalise 2015 as the year Australia woke up to the giant private debt and housing parasite leeching the country of prosperity, equality and egalitarianism. Here I was thinking that I enjoyed a monopoly on being a young person who understood that Australia enjoys the worst land/housing/mortgage bubble in our short history (a history with no less than 5 long forgotten housing bubbles that all ended in tears), and is on a collision course with economic and financial disaster.

But now I find out that I have to share my long held and evidence backed eyes-wide-open perspective on our impending financial and economic doom with other young folk who have correctly identified the real estate emperor’s missing clothes. My inner hipster has been crushed by the knowledge that I am no longer a trend setter in financial and economic literacy, and that my only consolation is being able to say “I knew about the bubble before it was cool”. How disappointing that I no longer retain the deeply scorned moral high ground of knowing better than the vast majority of the country’s Team Australia economists and journalists when it comes to the housing bubble.

Sadly I have to now share that honour with the country’s politicians, economists, journalists, and internet dwelling unwashed masses, most of whom have suddenly discovered that we do indeed have a bubble, after being reminded of such by no less than all four local economic regulators, a financial system inquiry, nearly the whole set of international ratings agencies and investment houses in the world, and a vast army of independent economists and analysts who long ago gave up on this country. For whatever reason the treasury secretary John Fraser was somehow able to point out to stunned audiences that there was indeed an elephant in the room, and that its ready to go on a rampage and trash the joint.

I suppose I should be grateful. Now we can all have a mature discussion about just how screwed we are. Which is where of course whingers like me come in. Belonging to the overseas-holiday-and-smart-phone-addicted, perpetually maligned, short of attention and financially illiterate Generation Y, I thought I’d offer my enlightened dissertation on the monumental balls-up that Australia now finds itself in. Aren’t we sick of being lectured by the existing landed classes, older generations and the real estate, banking, media and political circus that pretends to have half a clue about the largest financial, economic and social risk and injustice of our generation? It may surprise them to know that a lot of Gen Ys understand a lot more than we are taken for, and know a bubble when we see one. We do understand the slightest thing about risk, and are now ready to flip the bird in monumental fashion.

Feigned outrage aside, this is not just another hard-done-by social media rant, copied and pasted into blog form owing to the onerous character limit on Facebook posts. It is a serious condemnation of the current state of affairs with respect to housing in Australia. I hope to offer a rarely sought but valuable and unique perspective from a participant in the landless class/generations, who (as those who know me can attest) has been raging against the insane nature and consequences of the Australian real estate abomination for the last 5 years, alienating friends while railing on like some merchant of doom, only to swear he was on the right side of history. Which for the record I am.

Owing to the seriousness and late stage of Australia’s housing bubble, I no longer acknowledge any debate on the existence of the bubble itself. Like climate change, it is a fact. Time to accept it and mitigate the inevitable fallout. Like any rational and intelligent human being considering the question of anthropogenic climate change, I will only endeavour to engage in debate on the housing bubble definition, causes, scale, implications, consequences, solutions, and overall finger pointing.

If you wish to claim you know better, that’s fine, but don’t tell me about it until you’ve at least read the LF Economics submission to the House of Reps 2015 Inquiry into Home Ownership by Lindsay David and Philip Soos, which contains the full and inglorious detailed empirical evidence on the subjects that I summarise below, and is about 1000 times more informative than any real estate brainwashing and circle-jerk economic cheerleading you’ll get from the mainstream media.

So fair warning, this is an entitled Generation Y whinge to rival all others. A rant for the ages. The magnum opus of a landless youth with no one left to direct anger at that will listen. I promise it will be worth it though, so stick with me, you won’t want to miss the ending to this story.

The bubble facts, reason to panic

Let’s be honest, at the heart of their preposterous responses to the bubble subject this past week, is an attempt by Hockey and Abbott to fend off panic. Yes they have conflicts of interest like most parliamentarians including nice houses and investment properties. Yes they are staggeringly inept. Yes they want to see poor people punished for being poor. Yes they want to keep prices high both for their own interests and the interests of wealthy LNP voters. But it really goes without saying that the most politically damaging outcome for the terrible two would be the collapse of the housing market, with the financial system and economy following shortly afterwards. That is the real truth behind political inaction on affordability. No one wants to own the crash. I’m continually surprised by how few journalists identify that plain fact.

The proof of this fear is in the completely contradictory notion that the government wants prices to keep rising but wants to improve affordability. They must be seen to be doing something about affordability, while trying to defend price rises and pin any prospective price falls on Labor and all those meddling “recession clowns”. With real incomes falling for the last 4 years, and set to fall much further in coming years, achieving both of these aims is of course mutually exclusive. More on that later.

First consider that for Joe and Tony to be so clearly afraid of the bubble bursting, and with the hilarious and beautiful timing of Joe putting his $1.5million ranch up for sale, I argue that there must indeed be a bubble, and it will very soon meet the fate that all bubbles eventually meet by definition, and that is to burst. Joe and Tony have inadvertently called the top of the bubble. But don’t take their word for it. Let’s briefly consider the real evidence, definition, reasons and consequences of the housing bubble, and dispel the associated myths.

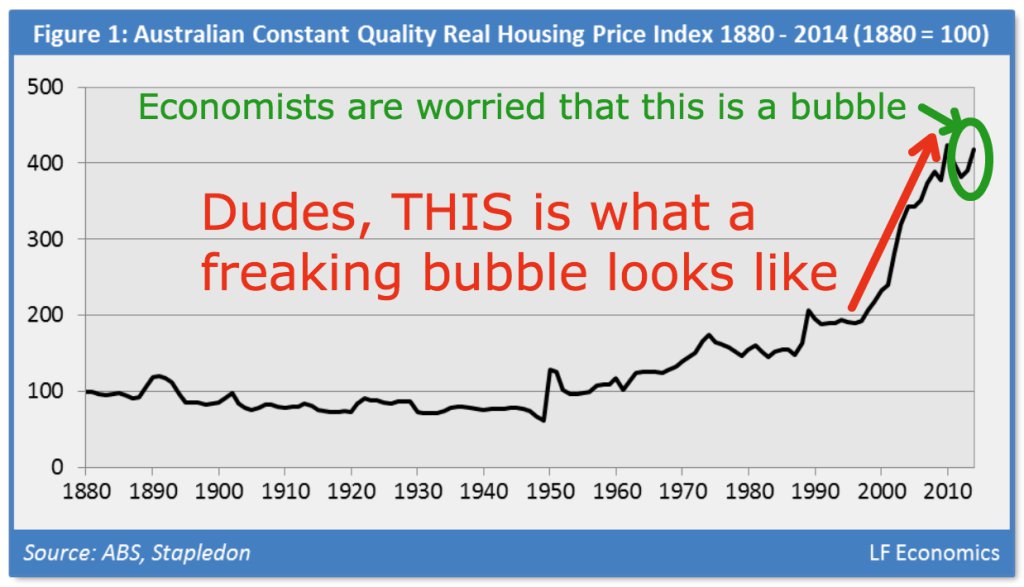

- The housing bubble is not new, and it’s not unique to Sydney and Melbourne. It’s not 3 years old, or even 10 years old. Australian housing has been in a nation-wide bubble since 1999, when John Howard cut the capital gains tax rate on residential property. Combined with falling interest rates, this set off an orgy of speculative investment, where speculators predictably saw the combination of negative gearing and capital gains tax concessions as the perfect tax shelter and a government sponsored get rich quick scheme.

- Economists and journalists like to quibble about whether the last 2-3 years of price action constitutes a bubble. Well there’s only one chart that matters when determining how big this bubble is, and when it started. And it’s truly magnificent:

- Since 1999, real house price growth (adjusted for inflation) has massively outstripped real income growth, real rental price growth and real economic growth. It is mathematically and historically impossible for that imbalance to go on forever. It has never happened in recorded human history, because people need to live in houses. If the average person can’t live in the average house there is no economy to speak of, no one to sell houses to, and nothing left to inflate house prices. If every member of Generation Y decided to go on a buyer’s strike tomorrow, the market collapse would be instant and complete.

- Like all bubbles, despite the many contributing causes such as tax incentives for speculation, failure to adequately tax land, policy supports, restricted supply, high population growth, greed, cultural obsessions etc, at the heart of the problem is always the cost and availability of debt.

- Structurally low interest rates and liberal lending standards combined with disposable incomes determine the ability of people to borrow money. People naturally pay what they can afford to borrow. As the saying goes, a house is worth what someone will pay for it. More debt = higher prices. Chronically low interest rates do not make housing affordable and prevent a crash, they cause bubbles, which is why the RBA is currently freaking out about the bubble, albeit many years too late.

- Private debt is therefore both the cause and the consequence of the housing bubble, and is also what is destroying our once diverse, productive and competitive economic structure, as it crowds out productive investment and lending, and drives up the cost of everything. And of course it’s what causes all the pain when prices finally crash.

- The most accurate academic definition of a bubble (from Hyman Minsky) is when investment returns (rent) do not cover the cost of investment (interest), so the investor is completely reliant (speculates) on capital appreciation to profit from the investment. This is the definition of the term speculator with respect to asset markets. The proliferation of negative gearing proves this to be the case in Australia. We have had overall net rental losses since 1999. When you have a market dominated by speculators who have negative cash flow, you have a bubble by definition.

- The national housing bubble has gone through minor corrections several times and each time been bailed out by massive cuts to interest rates, first home owner grants, relaxing of foreign investment laws, enabling self managed super funds to borrow to invest in residential real estate, and other fraudulent policies. We aren’t lucky or exceptional, we just geared our whole economic and taxation system to supporting house prices, and did everything to stop a crash. But with the coming economic downturn and smashed government finances, we are now out of ammo baby.

- We have almost the least affordable housing in the world compared to every single measure you can compare it to, yet Australia is not exceptional – it is not different here. We just had an extraordinary set of circumstances, and anyone who has studied first year economics understands that specific combinations of circumstances are always cyclical. Like all economies and societies in human history we have boom and bust cycles, and the larger the boom, the larger the bust.

- I don’t need to tell you that Australia has just had one of the largest economic booms in its history, comparable to the gold rush, when land values in Melbourne escalated dramatically over many years. But economic booms do not guarantee that bubbles don’t burst. Usually the opposite in fact. In the 1890s (post the gold rush), the land bubble burst, causing the Australian Banking Crisis, and real house prices took 50 years to recover from massive falls. If you were born in that era, you would no doubt have been told by parents, friends, bankers and media that house prices always go down. Imagine that.

- Australia has had no less than 5 prior housing bubbles, in the 1890s, 1920s, 1950s, 1970s and 1980s, and none of them ended well. What to speak of the lessons from the GFC. Why are we not lectured on these by the older generations? In every bubble there is the claim that this time it’s different. History proves that once you have a bubble, it’s never different. But we only learn that once it’s too late yet again.

- I don’t need to spend any time explaining the exact fallout from a crash. We all know its going to be bad. Can’t we just feel it in our bones?! If you want the gory details, go chat to some friendly folk in Ireland, Spain or the US.

And now to quickly dismiss some of those completely tiresome myths that are repeated ad nauseum by the real estate lobby, bankers and Team Australia economists, the same myths that characterise every bubble in recent history:

- There is no genuine lack of physical housing supply. If there was a genuine shortage, rents compared to incomes would also have experienced a similar level of growth as prices. That is not the case. Rental growth is currently at its lowest level in decades. While city rents are expensive, they mostly reflect the enormous wage gains that flowed from the mining boom, and not speculative demand fuelled by cheap debt. Although a serious issue for housing affordability, rents are not a bubble.

- Restricted supply of housing leads to steeper price falls when excess demand is removed. When supply is limited, a small increase in demand leads to a large increase in price. But the inverse is also true, where a small decrease in demand (from say, chronic unaffordability, rising interest rates, investor panic, forced sales owing to rising unemployment etc.) will lead to a large fall in prices, just as swiftly as the rises on the way up.

- This is exactly what happened in recent bubbles in Ireland, Spain and the US, where everyone insisted for years that there was a massive shortage of supply. Ireland in particular went through a massive surge in construction because of this claim, and suffered much worse price falls because of it. This is exactly what Australia is doing, building into the bust.

- We do not have safe banks, or responsible lending standards. The Australian Prudential Regulatory Authority is currently working with banks to raise their capital buffers, which have been shown to be woefully inadequate despite the myth of the opposite. This is because major banks have been able to decide for themselves how risky their mortgage portfolios are. When compared internationally, they are no less risky than Lehman Brothers before the US housing crash. APRA is also belatedly enforcing higher lending standards to residential mortgages, as there is deep concern about loan to value ratios, interest only loans and interest rate buffers, to name a few things.

- Even if we did have responsible lending standards and ultra safe banks, these things do not prevent a bubble from forming or bursting. They did not help Ireland, Spain or the US (or Australia in previous bubbles). All you need for a bubble to form and eventually collapse is cheap debt and the belief that prices will always rise. As discussed earlier, all you need is speculators who require capital gains to earn a profit.

- House price speculation is not good for the economy, its actually really bad. It has completely distorted our economy by diverting money and investment away from productive enterprise and business and into unproductive asset price speculation. It has made us uncompetitive, extremely indebted and debt addicted, utterly reliant on export income, un-diversified, and totally pro-cyclical, driving away bellwether value-added economic activity like manufacturing. When the current economic cycle driven by mining and housing fully turns for the worse (which it is already), our economy is toast. We have no resilience or diversity to see us through the hard times. That mythical beast, the “wealth effect” from rising prices, only works when there is more capacity for debt growth and price rises, and supportive economic conditions.

- Despite the claims of some short-sighted industry types, the currently falling prices in WA, NT and ACT are not proof that there is no national housing bubble, they are proof that the bubble is very close to the top, and majorly fraying at the seams. Only Sydney and Melbourne have been able to maintain the irrational exuberance at this late stage of the bubble with the help of international money laundering and general speculative insanity – proof that the nation’s housing market is on very shaky ground. Wherever you are in the country, the value of your house is at major risk from the coming correction.

- The last myth is my favourite, the one that seeks a scapegoat. There is no single cause for the bubble, nor a single party to blame. There has been an extraordinary swathe of cultural, policy and tax settings to get us to this stage, and nearly all of us bought the line about “this time it’s different” hook line and sinker, just like every other bubble in history. We gave into greed and ignorant exceptionalism, and when this one blows, we will all share the blame and the pain.

A bubble has a way of consuming the hearts and the minds of the country it infects, like a genuine parasite slowly eating its host alive. We have an inability to see things ever being different, until one day the fog clears, the tide goes out, and we see who is left standing with or without pants on. A common fear amongst the younger generations is that they will never own property. This is what I like to refer to as ‘grey sky thinking’, something I heard a property developer of all people once use to explain this psychological phenomenon. There is always a blue sky somewhere, you just forget it exists when you’re stuck in a storm cloud for 20 years.

As I’ve explained, and history shows, it is impossible for such circumstances to continue indefinitely. There is always a cycle at work, no matter how long the cycle. There is only one way out of this for young people, and that is price falls. The time for solutions like tax reform to save us from this fate has passed. We must still pursue these reforms to prevent the next bubble from kicking off down the road, but we cannot prevent the completion of the bubble cycle. All that is needed is patience. No one bothers to explain this whole back story and actually provide real advice to young Australians. All we get is stereotypes, platitudes and false dichotomy. We are constantly let down by people who should know better. People who should have learnt from Australian history and recent global history exactly how dangerous housing bubbles are.

But instead young people are hypnotised by the corrupt and sinister plea to “Buy now or forever miss out”. Ask yourself who it is giving this advice, and who the advice really serves. Apply a little ‘cui bono’ (who benefits) to those real estate industry pimps and pushers.

Its all about risk (and who it belongs to)

A whole generation of leaders and land owners is asking the current generations to accept the poisoned chalice that is Australian real estate. I’ve long said that housing affordability is only the main symptom of the disease, and that the greater injustice is the disease itself, an utterly broken economic model that is wholly reliant on housing speculation, and its sinister ‘comorbidity’ factor: unacceptable financial risk. Unacceptable financial risk is exactly what young Australians are being asked to take off the hands of the landed class, a giant intergenerational transfer of wealth in return for a broken system, just like climate change (apologies, but the analogy is such a good one).

The overwhelming expert consensus is that Australian housing has never been less affordable and more risky. Yet members of Gen X/Y are arrogantly dismissed as spoilt and entitled. Somehow I’m meant to be selfish for rightly pointing out the 20+ years of policy failure (policy rigging) serving the entitlements of existing home owners and speculators, which ruined the productive economy in the process, and for pointing out the terminal risks being thrust upon us. That I’m just an entitled youngster living at home with my folks with inflated expectations, who only cares about how to snag some trendy inner city dive.

This indefensible point of view has been a widespread phenomenon across the Western world in the last decade or so, as those who have benefited from global housing bubbles and rigged financial systems must shoulder at least part of the blame, but instead seek to alleviate guilt by disparaging those on the other side of the fence. Looking at the world post GFC, it’s pretty hard to see how young folks deciding they couldn’t afford a house because they spent too much money on iPhones and didn’t want to live 100km from where they worked, somehow caused the greatest financial meltdown since the great depression. Sorry folks, the answer is private debt and housing bubbles.

The cognitive dissonance of those who defend the status quo is astounding. My publicly professed aspirations as an eventual home owner are meant to somehow preclude me from being critical of economic policy and tax settings that completely ruined our economy, because I’m just entitled. That’s why young folks are finally calling bullshit, and like all bubbles, this one will collapse under the weight of its own hubris and internal contradiction. We’re not selfish, we’re just not financially suicidal. We’re f*ing sensible, and not ready to stand by and take another bolloxing from the powers that be and their indefensible protection of the worst housing bubble in a hundred years.

Young Australians are expected and encouraged – even conned and bribed – into taking on utterly crippling levels of mortgage debt in the assumption that the housing bubble party will continue forever, and that the only way to a secure retirement is to sell your soul for a slice of Aussie real estate. Meanwhile, there is nearly universal acceptance that our housing market is unsustainable in its current form, and a countless list of official warnings from global and local regulators and economic bodies such as the IMF, the OECD, the RBA, ASIC, APRA, international ratings agencies, the Murray Financial System Inquiry, and now arguably our top economic advisor and public servant, the head of the treasury John Fraser. They have all at some time in recent history said we should be very wary of our house prices and the possibility of collapse.

When do the economics editors of the country ever refer to this long list of warnings, and apply it in cautioning young Australians to be extremely careful when considering the risks of entering this current market? How dare these charlatans convince the impressionable younger generations to take on such astronomical risk with barely a mention of these warnings that have repeatedly issued forth from the most experienced and trusted economists in the world. Do Joe Hockey and the tabloid pro-housing spruiker journalists and garden variety real estate agents somehow know better? Are the worlds top economists and analysts just a bunch of doomsayers and clowns? No, they just understand what risk is, unlike the majority of Australians.

Falling prices are coming, and this time they will lead to a self-fulfilling crash

By now it is self evident that house prices must fall to restore affordability. I go further and argue that because of the universal characteristics of a bubble described above, and a backdrop of deteriorating economic conditions and falling incomes, a house price crash is the necessary and inevitable solution to housing affordability.

Given that fact, for young Australians like me, I want to paint a picture of the utterly improbable and devious situation that we are being asked to swallow, by drawing further attention to the contradictory view frequently shared by senior politicians, journalists and writers from an older landed gentry who profess to have a genuine concern for the ability of the next generations to own land at some point in the future, but do not wish to suffer price falls. Or if they begrudgingly admit price falls are needed, the admission is usually coupled with calls for some kind of mitigating policy (such as first home owner grants or allowing access to superannuation for housing deposits or cautioning advice), or counselling caution in reforms in order to ‘avoid distorting the market’, or to ‘avoid a crash’.

In taking this supposedly sensible position, these allegedly well meaning individuals in positions of influence are unavoidably acknowledging the very real threat of a market collapse, and the implications for the economy, financial system, and their own personal assets. But they also feel guilty enough (or possess a conscience enough) to want a solution to housing affordability. They don’t want the market to collapse, but they want young Australians to be able to buy into the market that they know is at risk of collapse…

Think about that for a minute. The notion that making necessary reforms to housing and tax policy might trigger a market downturn and should therefore be offset by some form of stimulus or ‘grandfathering’ of reforms, is a deeply troubling one. If the market is due for a collapse (which it is), it won’t be because of measures to correct the imbalances, it is because of the imbalances themselves.

In other words, most of the economists, journalists, politicians and the landed gentry that they represent, who occasionally advocate for housing reform and solutions to housing affordability, are asking the next generation of Australians to assume all of the risks of the massive imbalances in the housing market, while ensuring that the market is held up long enough for them to pass on that risk. They want us to inherit the enormous risks that they created, holding open the fire escape just long enough to get out before the collapse, which they quietly acknowledge is the most likely eventual outcome.

What a conceited set of leaders and commentators we have. I vainly hope for royal commissions and criminal charges to be laid in some not-so distant future when our livelihoods have been destroyed by the pedlars of Australian real estate who do know better. In Ireland, a country devastated by its own epic real estate bubble with striking similarities to our own, there have been no criminal charges. But there has been an official inquiry. And the results show that the Irish media were complicit and culpable in their unquestioning loyalty to booming real estate and their wilful blindness to the unfailing history of asset/credit bubbles to destroy at least as much wealth as they created on the way up. They were shown to be complicit due to their proven conflict of interest in deriving profits from real estate mania, and no doubt because of a desire to protect their own personal land holdings, and deny any existential threat to their paper wealth.

The long and shameful (and predictable) history of asset bubbles proves that the beneficiaries of the bubble are always victim to a certain exceptionalism, a notion of providence and intelligent decision making that enabled their participation in such windfall gains. The smart investor that got in at the right time. If only there was a way to alleviate the nagging guilt and subconscious fear that eventually there will run out a stock of greater fools to maintain the bubble. Because when there is no stock of greater fools, a self-fulfilling destiny of price collapse follows, as price falls at the margin trigger a rush for the exits by those speculators with negative cash flows who can no longer rely on ever rising prices.

The way to temporarily alleviate this guilt and fear is usually to argue for the economy to catch up to this imbalance between prices and economic fundamentals. The bubble deniers argue that for almost the first time in history, a price bubble will not have to deflate, but that the rest of the world will catch up, justifying the speculative wealth gains achieved by the bubble participants and their exceptional investment choices.

And worse, this exceedingly improbable plan to manage or ‘taper’ the bubble is in direct contradiction to the notion that it is in the interests of those excluded from the bubble to be granted help to participate at this late stage. It is an admission that the bubble cannot go on as it has, but must be preserved in a permanently high plateau to protect speculative wealth gains, and yet sold as a worthwhile risk and investment to the next generation of buyers who will falsely believe that recent price history will repeat itself, but that the long term history of prices matching economic fundamentals – like incomes, rents and economic growth – will not repeat itself. It is disingenuous in the extreme.

This is the cognitive dissonance that our political economy suffers from in huge measure. Everyone with land has a stake in preserving the status quo, even if they do not admit it, and when the vast majority of experts themselves are part of the landed class, we cannot trust their notions of bubble management that masquerade as altruism in assisting people to afford housing at the peak of the bubble. This can only be seen as an offensive disservice to young Australians who don’t know better.

Investment, finance and economics is all about understanding and managing risk, and when we cannot trust anyone to tell the truth about risk, be it media, politicians, family, friends, and certainly not real estate agents, it is the surest sign that we are reaching the zenith of the largest land bubble in Australian history. It should serve as a severe warning to the un-landed masses to avoid at all costs being drawn in to this apogee of risk, just to enable the winners to cash in on their paper wealth, and get out while they can. This is the hot potato that young Australians need to reject at all costs. Let it fail because it must.

For otherwise intelligent and expert commentators and leaders to accept the very real risk of collapse, but to convince the impressionable young to assume that risk is a deeply selfish and contradictory perspective that must be condemned. History will ensure that it is condemned, so for your own sake, don’t fall for the greatest con in living memory. It is inevitable that we will see at least some price falls, and that these price falls will lead to a rush for the exits when there is no longer any policy or monetary levers left to bail out the market. Therefore you have nothing to lose from waiting this out and shunning the housing bubble, and everything to lose from gambling on this sinister and severe level of risk that we will shortly come to understand in all of its emergent horror.

Because what comes next is the housing crash we had to have.