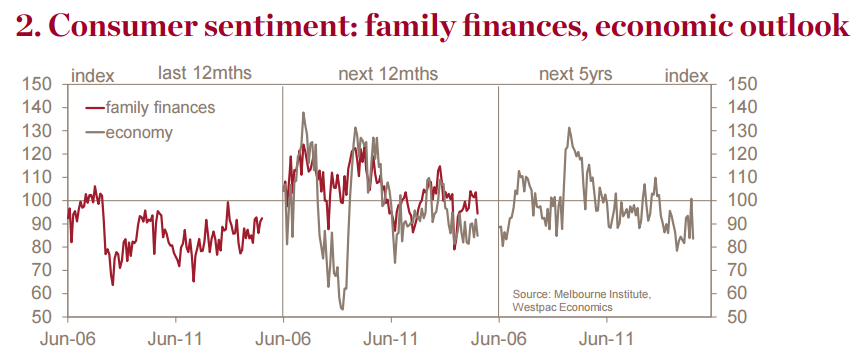

― The Westpac–Melbourne Institute Consumer Sentiment Index fell 6.9% in Jun to 95.3 from 102.4 in May. This is a surprisingly weak result that reverses all of last month’s promising postnBudget and post-rate cut rally.

― The reversal likely reflects a range of factors with renewed concerns about the economic outlook a key theme – sub-indexes tracking expectations for economic conditions showed particularly sharp falls, reversing sharp gains in May.

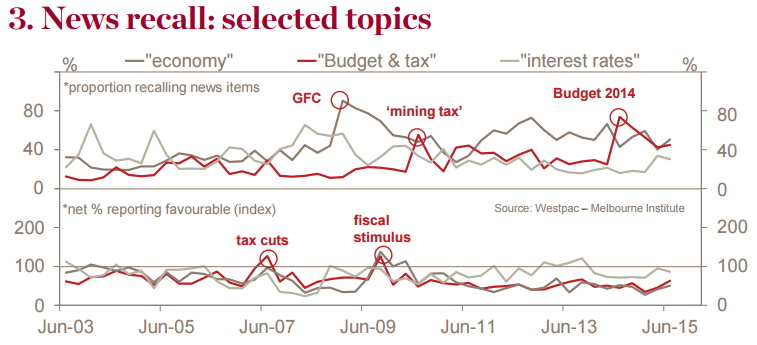

― Additional questions on news recall showed news on ‘the economy’ was more dominant than ‘budget & taxation’

– a switch on 3mths and notable shift compared to a year ago. News on both of these topics and on other high recall topic continued to be viewed as unfavourable albeit marginally less unfavourable than in Mar and Dec.

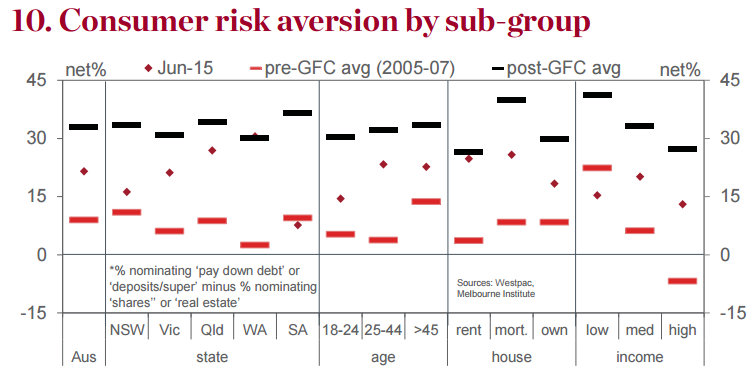

― Updates on the ‘wisest place for savings’ question show little change since Mar. Consumers continue to favour ‘bank deposits’, ‘real estate’ and ‘debt repayment’ as the wisest place for savings, with 29.4%, 24.6% and 16.5% nominating these options respectively in Jun. The mix is almost identical to that in Mar with the Westpac Risk Aversion Index essentially unchanged at 22.3 but still showing an easing in risk aversion since Dec’s reading of 36.7.

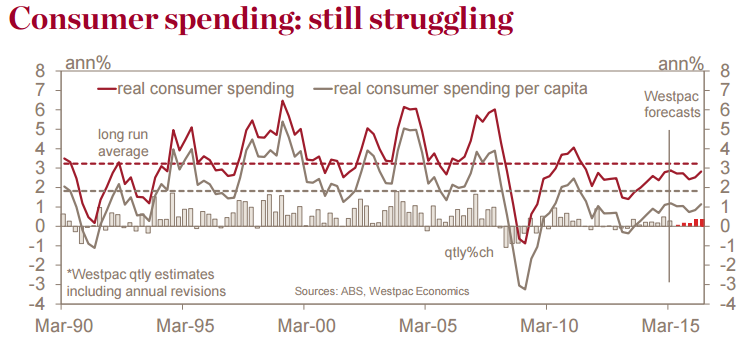

― Our CSI± measure – a modified sentiment indicator that we favour as a guide to actual spending – posted a 2.8% dip in Jun, a somewhat milder decline than the 6.9% fall in sentiment overall but showing a similar decline over the last two months. CSI± is pointing to weak spending over the H2 2015 with per capita spending growth in the 0-½%yr range. Including population gains of 1.6%yr, this points to aggregate consumer spending growth of under 2%yr, a further loss of momentum from an already sub-trend pace.

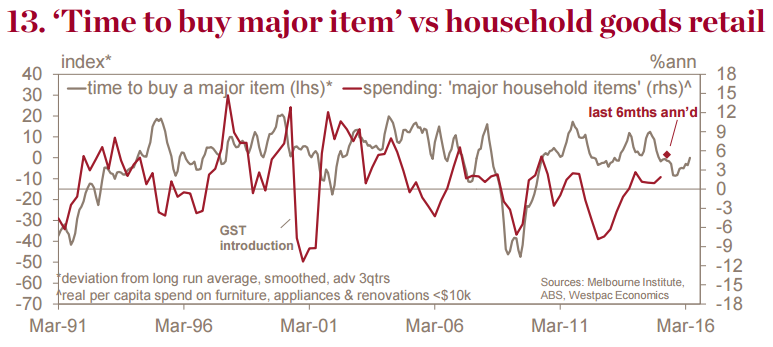

― Attitudes towards spending softened in Jun. The ‘time to buy a major item’ sub-index declined a further 2.5% after slipping 1% in May to be down 5.6% on a year ago. Despite this, spending on ‘major household items’ has shown some improvement over the last 6mths.

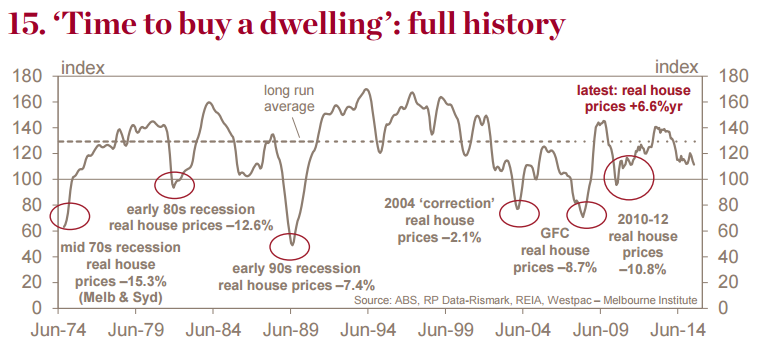

― The index tracking views on ‘time to buy a dwelling’ declined 1.6% , but is still 3.4% above its pre-rate cut level in Apr. At 111.5, the index is below its 15yr avg of 116.6 but still well above the lows seen heading market corrections historically. Buyer sentiment is notably stronger in Qld.

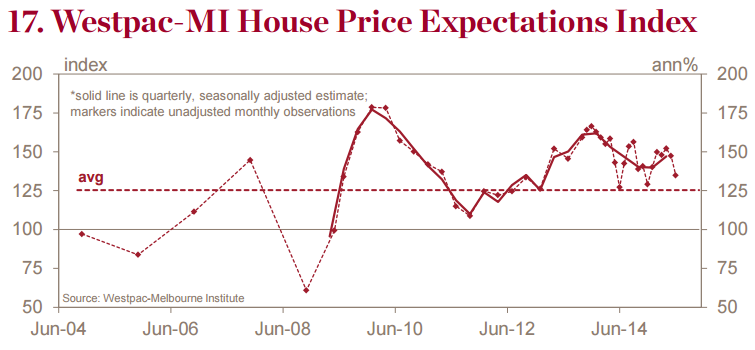

― Consumers appear more nervous about the outlook for house prices. The Westpac Melbourne Institute Consumer House Price Expectations Index The Westpac-Melbourne Institute Consumer House Price Expectations Index fell 8.5% in Jun to be down 11.4% in 2mths. At 134.9, the index is still in solidly positive territory. Evidence suggests some of the recent decline may also be seasonal. Price expectations are much weaker in WA.

― Job loss fears remain a major source of concern for households. The Westpac-Melbourne Institute Unemployment Expectations Index rose 3.8% to 152.8 (recall that higher readings indicate increased expectations that unemployment will rise over the year ahead). High readings on unemployment expectations have been a persistent feature over the last 4yrs and point to a perceived lack of job security as a key restraining factor for consumers. This is despite other measures of employment conditions suggesting some improvement in over the last 12mths.

The cautious consumer marches proudly, structurally, on.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.