A nice piece at Dad’s Army today from Dr Patrick Carvalho of the Centre for Independent Studies:

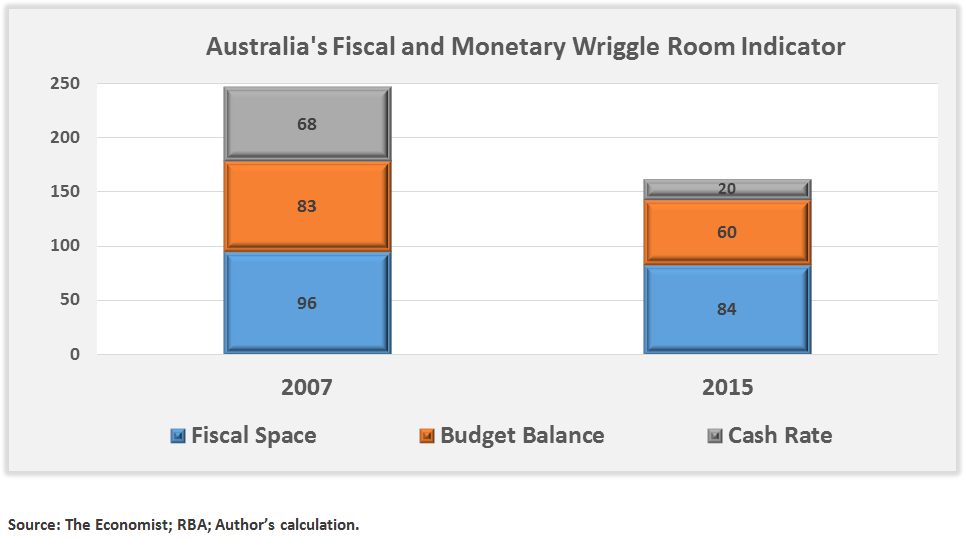

To determine how much wriggle room Australia might have when the next crisis strikes, we can use a tool recently devised by The Economist, a tripartite indicator, to gauge the ability to fight recession.

…A history of consistent and accelerating surges in both tax receipts and public deficits since the GFC has tarnished our ability to rely on more debt accumulation to counteract the effects of an eventual crisis.

Hence, Australia’s fiscal space buffer has diminished from 96 per cent of its theoretical debt limit before becoming insolvent (translating to 96 points in the 0–100 fiscal space metrics) in 2007 down to the current 84 per cent (84 points).

…Australia finished 2007 with a cash rate target of 6.75 per cent (68 points) — the highest level since 1996 — down to the current lowest historical level of 2 per cent (20 points), which leaves practically very little room for the RBA to assist when the next recession comes.

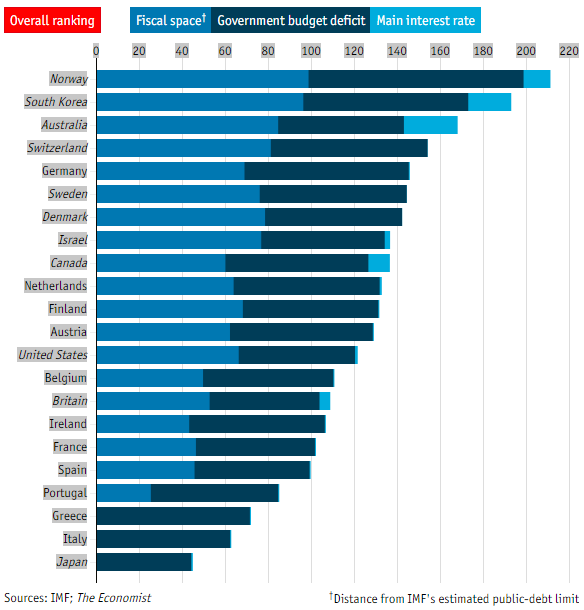

Carvalho concludes with The Economist that Australia’s scope for stimulus is relatively strong versus other countries if not our own past:

Advertisement

Solid analysis but it has some nasty flaws that lead it to misrepresent our strength.

I’m not sure how monetary policy can be seen to have diminished only from 83 points to 60 when the relative position of today versus 2007 is 2% versus 6.75% and we’ve been in an easing cycle for three years showing a lack of traction. I’d score remaining monetary policy firepower in a crisis at more like 20 points.

For fiscal policy it is similar. Australia is already on the verge of sovereign downgrades. That places a political limitation on what’s possible for counter-cyclical spending and more importantly an economic one. Given Australia is externally funded via its banks and that borrowing is guaranteed by the Budget, as monetary policy is exhausted, it is the state of the Budget that will determine real Australian interest rates depending upon what compensation offshore investors demand for Australian risk. I put it to you that that limits possible stimulus much more than a fall from 97 points in 2007 to 84 points today. Let’s call it 50 points.

Advertisement

Assuming the deficit component of The Economist scale remains the same that gives Australia a total score of 120, similar to the United States.

That still sounds OK but we must add one final element. The US has had its bust already and undertaken much structural repair in deleveraging, a corrected current account deficit and improved real exchange rate. Australia has had a little of the same courtesy of the mining boom but nowhere near enough so its next downturn will very likely include very strong structural headwinds as well as cyclical that will chew through stimulus ammunition very fast.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.