Australia’s last sane man standing – Saul Eslake – nailed the bubble over the weekend:

“I would say they are causing social harm because they are widening the gap between those who have houses and those who don’t, and freezing younger generations out of home ownership,” he told Fairfax Media.

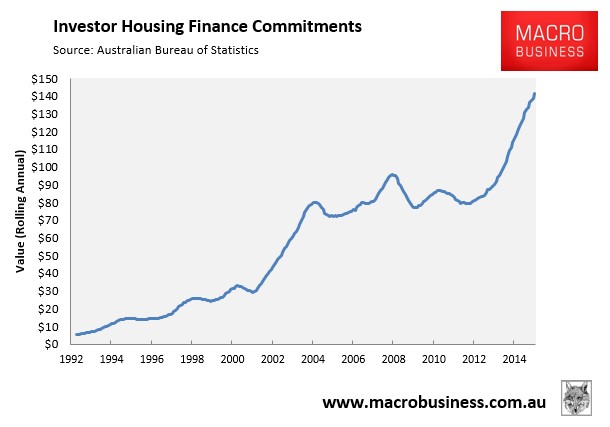

The social harm is far more widespread than that. At the top of the list is the political economy, which has disappeared into its own cloaca. Take, for example, weekend coverage of said bubble. At the AFR the lead story was by a rentier quotathon from Robert Harley:

On consensus, Sydney housing is not yet in bubble territory. Price growth elsewhere in the country is now moderate, though specific markets show bubble characteristics. In the resource towns of the Pilbara and central Queensland, the bubble has clearly burst. In Melbourne’s CBD, the sheer volume of new supply looks like a bubble in the making.

…ANZ senior economist, David Cannington says investors should not look to the past for guidance because the market drivers are changing “pretty quickly”. For Cannington, the current exuberance is a “rational” response to the step down in mortgage rates.

The “current mix is pretty unusual”, says Westpac senior economist Matthew Hassan. “How those pieces of the puzzle fit together is hard to know. It’s about trying to guess where the surprise will come from,” he adds.

“Interest rates are pretty accommodating, so you are trying to second guess non-standard policy measures. It is very hard to gauge their effectiveness and the willingness of regulators to apply pressure.”

For Macquarie Capital’s head of real estate strategy, Rod Cornish, the key is affordability – measured as the proportion of household income needed to meet mortgage payments. Significantly Sydney’s affordability has hardly changed in the past year, with falls in interest rates and rises in household income offsetting the jump in prices.

…So what does a price collapse look like? Over the past 45 years, Australia has had six house price corrections. Prices did correct after each boom but, according to numbers from Westpac, not very far.

More accurately, a consensus of vested interests bank economists says Sydney is not a bubble. Lost your non-bank sources, Robert? If 2003 was a bubble then what is this?

At The Australian the Abbott Government’s support for the bubble generated sympathy from Liberal Party stalwart Henry Ergas:

To suggest Australia is poised for a catastrophic collapse in housing prices therefore seems an exaggeration, if not an example of what Julia Gillard termed “hyper-bowl”. Rather, the market shows more signs of localised froth than of a generalised speculative wave that will end in disaster.

To say that is not to deny that housing price inflation is running at around 8 per cent and auction clearance rates have been high in Sydney and Melbourne; but seen over the longer term, the pattern of housing price rises largely reflects that of population growth, with Sydney prices, which had lagged the national average, now catching up.

Moreover, if low interest rates are to stimulate dwelling construction, it must be by increasing the price of existing properties, otherwise there would be no impetus for the housing stock to expand. And the costlier and more complex it is to build new houses, the greater the rise in prices for existing dwellings must be before new construction picks up.

To that extent, Hockey is right: if Sydney housing inflation is high, it is in large part because the supply of greenfield land in the Sydney area remains at near historic lows, while there has been virtually no progress in reforming the planning laws that make infill construction arduous, slow and expensive. The Treasurer is also right that without the latest round of price increases, it is unlikely dwelling investment would have increased by 8 per cent last year, contributing nearly half a percentage point to growth in our gross domestic product.

This is a blowoff in a fifteen year bubble. You can’t just look at the recent two years, the rest of it matters too, leading to by far the highest prices and indebtedness in the nation’s history.

Meanwhile the Government itself appeared at the ABC:

JOSH FRYDENBERG: Well, I’m saying that we need to watch the housing price growth, and APRA and the RBA, which are the regulators, are doing that. But at the same time, we have seen strong housing prices before. In the early 2000s, housing prices increased by 20 per cent for three years in a row and then were steady for a decade and there wasn’t a bubble that led to a major correction. So, we have seen these sort of rises in housing. It’s a function of a number of things. It’s a function of population growth, it’s a function of, you know, state governments not engaging in enough land release. It’s a function also of foreign investment and that’s why we’re introducing changes around foreign investment too.

Instead of the Government using policy to lean against or reform away the bubble, it uses policy to argue that it doesn’t exist.

Fairfax’s David Potts took the cake:

I don’t know what possessed the head of Treasury to say Sydney and parts of Melbourne are unequivocally in a bubble, a description the Reserve Bank has studiously avoided.

What did he expect? With the lowest lending rates ever, this is the property boom we had to have.

In any case, a true bubble requires over-the-top borrowing, which the banks say ain’t happening, and the regulator is making sure by limiting loans for investment properties to 10 per cent growth. Besides, everybody knows mainland Chinese pay cash.

Which is illegal, not a reason to support it.

The economy, the Government, the media, the very social fabric has developed some kind of extreme bubble personality disorder in which black is white, wrong is right, illegal is legal, excellence is density, advertorial is culture, selfishness is fairness, infanticide is parenting, investment is speculation, fiction is truth, private is public and obsession is health.

There have been bigger bubbles elsewhere but after three business cycles of inflation in a nation with a nebulous identity there has never been one that so completely engulfed a country.