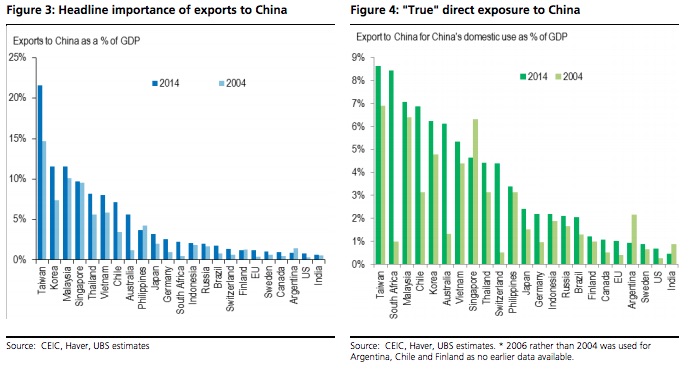

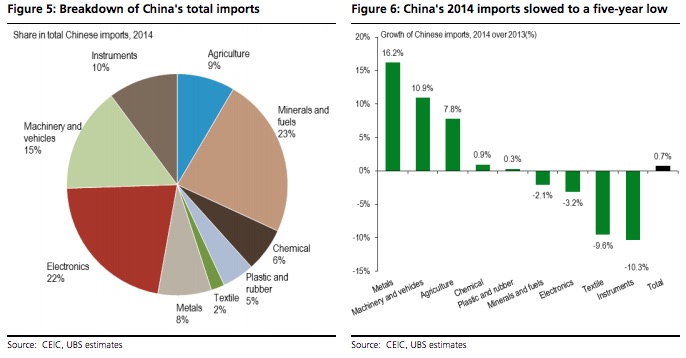

In the decade to 2014, China quadrupled the number of countries to which it was the biggest export market, as the US almost halved the number of countries for which it held the same title. Over the same period, all countries under our coverage saw China’s share of their exports hold broadly steady or rise up to four-fold. The jump in their direct “true” reliance on China (excluding reprocessing trade) was even more dramatic, with South Africa’s and Switzerland’s up by more than 8 times, and Australia’s by almost 5 times.

Two factors have made global exporters more directly reliant on Chinese domestic demand and thus more vulnerable to the ongoing property-led downturn in recent years: 1) rapid growth of China’s domestic market; and 2) processing trade’s declining share of Chinese trade due to China’s expanding productive capacity.

In this year’s version of our annual China export exposure chart book (available upon request), we show how China’s slowing economy is affecting commodity, reprocessing, and developed country exporters alike…with China’s property construction deceleration set to deepen this year in a multi-year slowdown, we may see a longer-term decline in China’s appetite for foreign industrial imports.

I am always amazed at how significantly these kinds of surveys underplay the importance of China to Australia. Simple ratios of exports to GDP do not capture two very important ways that China influences Australian standards of living. The first is income which has been hugely boosted over time owing to the immense profits available in a very small number of commodities. The second is how that income flows through the economy, most especially supporting the health of the Federal Budget, enabling its guarantee of the offshore borrowing that drives the services economy.

The indirect exposure of Australian exposure to China is almost unquantifiable in the same way that a small sub-section of the US housing market called “sub prime” was thought to be an innocent and easily absorbed aberration.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.