Chris Weston, Chief Market Strategist at IG Markets

The idea of the efficient market hypothesis was put to the test yesterday, along with the principle that markets effectively price events in.

Greece and the outcomes of a rejection of austerity have always been a known unknown, but the timing and sheer defiance from the Greeks have startled markets, causing strong range expansion. This has been perhaps most noticeably seen in the various implied volatility measures across the markets, proving traders have been smacked into action and a real wake-up call has been provided.

Many have been talking about a level of complacency in markets, but the portfolio protection sought by market participants has been very aggressive.

One-month implied volatility in EUR/JPY spiked 20% yesterday, with 10-day volatility in the German DAX now at a multi-year high. The S&P 500 VIX (volatility index) pushed up 34% for the biggest move in two years, but this seems a function of leveraged and high-frequency funds running the largest net short position (in VIX futures) since mid-2013 and having to cover. Interestingly, the S&P 500 could be on for a weekly change of more than 1% – something it hasn’t managed in nine straight weeks and the fifth longest weekly run of all time!

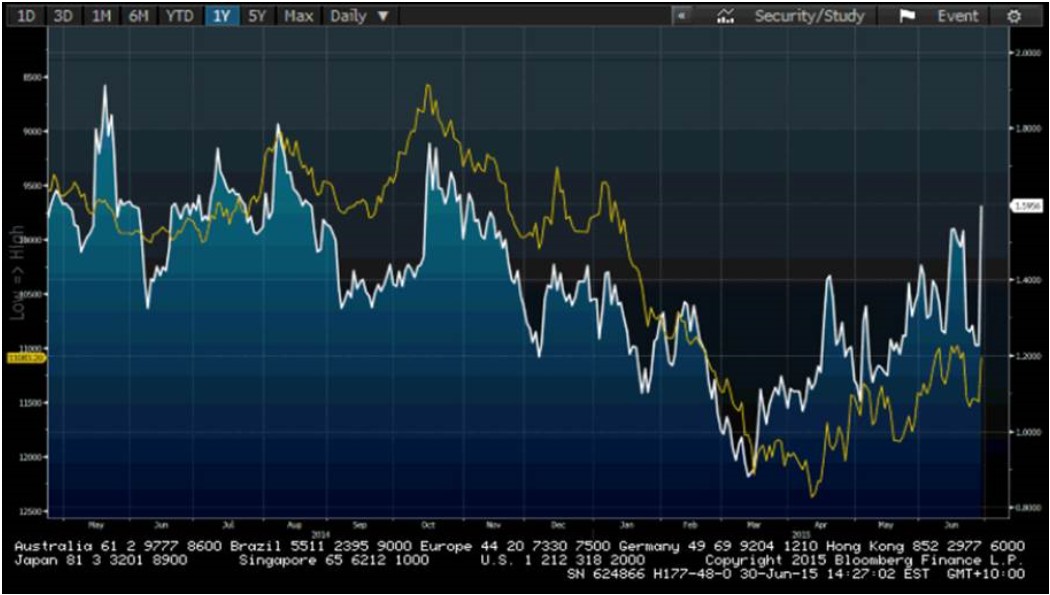

The bond market, however, is the place to take cues from. Most in the market will rightly point out that Greece accounts for a small percentage of Europe’s output but it is the contagion risk that will drive sentiment. The best way to measure contagion risk is through the German bund/Italian BTP or Spanish bond spread. Judging by the fairly aggressive (not to mention incorrect) narrowing of this yield spread from 16 June through to late last week, traders have had to perform a monumental about turn, pushing out spreads by over 150 basis points apiece. If this spread continues to widen, it will drive down developed market equities and increase implied volatility, although the ECB will look to mitigate this.

(Italian/German bond spread in white, DAX in yellow and inverted)

Source: Bloomberg

This yield spread though, like many risk assets, is now a slave to the Greek referendum polls and, while the two polls we saw yesterday threw the balance of probability into the ‘yes’ camp, the ‘no’ camp made some real traction. Price action should be watched closely this week and, although a snap back in sentiment could occur this week, it seems unlikely given the potential for a ‘no’ vote on Sunday. As European Commission President Jean-Claude Juncker detailed yesterday, a ‘no’ vote would effectively be seen as Greece turning its back on Europe. Monday’s Asian open promises to be one of the craziest for many years if the Greeks favour a ‘no’ vote and the prospect of gapping risk is once again sky high.

Saying all of that, most of Asia has seen subdued conditions, notably in the ASX 200 and Nikkei, although we haven’t seen a sufficient injection of confidence to boost our European equity calls. An extension of yesterday’s sell-off is on the cards.

Certainly, of these two markets the ASX 200 is in the weakest position and many will be glad to roll into the new financial year despite a fairly well pronounced downtrend in play. Traders have clearly ramped up portfolio protection, seen in the ASX volatility index spiking 17% yesterday (its flat today) while the ASX put/call ratio stood at 2.11x in early trade – the highest as far as the data goes back. Our own flow today has been much more nuanced and the moves have been two-way if we take the ASX 200.

China, as always, is a different beast. Our client business has been skewed to the buy side. 75% of all open positions on the CSI 300 are long and are therefore expecting a bounce. I see no other way but to trade China ultra-short term as the various indices could be 5% higher or lower if you hold onto a position for more than 30 minutes. This makes setting stops very tough and of course means keeping position sizing to a minimum. Still, the news flow has ramped up and the bias here has been very market friendly indeed. It is clear the authorities are keen to promote stability and we are seeing signs the various Chinese markets are responding.

Talk of putting a halt to the IPO process helped spur some buying yesterday and it will certainly help mitigate the prospect of traders selling existing stock holdings to take part in the IPO process if it plays out. There has also been talk of using the country’s endowment fund to buy equities, as well as cutting stamp duty, while the PBoC has furthermore cut the seven-day repo rate by 20 basis points to 2.5%. It seems that the market is keen to deleverage but for today the bulls are being enticed into longs courtesy of further (and potential) central bank and governmental initiatives.

Ahead of the European open we are calling the FTSE 6591 -29, DAX 11006 -77, CAC 4840 -29, IBEX 10768 -85 and MIB 22388 -188