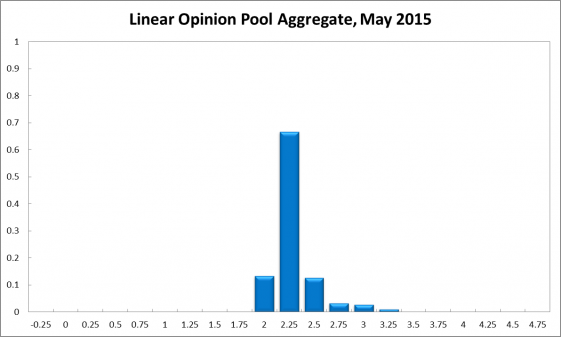

Economic data is once again painting a motley picture of the Australian economy. Slight improvements in the labour market, stronger commodity prices, and a headline inflation rate near the centre of the official target band stand opposed weakening consumer sentiment and a deterioration of the international economy. Appreciable risks exist on both the upside and the downside. The CAMA RBA Shadow Board on balance prefers to hold firm but still considers it necessary that the cash rate is lifted in 6-12 months. In particular, the Shadow Board recommends with confidence that the cash rate be held at its current level of 2.25%; the Board attaches a 67% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals 13%, while the confidence in a required rate hike stands at 20%.

Australia’s jobless rate, according to the Australian Bureau of Statistics, fell slightly to 6.1% in March, accompanied by a marginal increase in employment and the participation rate. Wage growth remains muted. The Aussie dollar rebounded from its recent low and now fetches close to 80 US¢. Yields on Australian 10-year government bonds have also rebounded from a recent low to 2.59%. Both these developments suggest markets are cautiously optimistic about Australia’s near economic future.

Sydney’s housing market and domestic asset prices remain buoyant.

International conditions are deteriorating somewhat. European growth remains soft. A Greek default in the near future is a real possibility, along with a concomitant shock to the European financial system. China is looking to curtail the adverse consequences of excessive private debt. Recent statistics from the US are showing a weaker than expected first quarter of economic activity. Consequently, the Federal Reserve Bank’s increase of the cash rate may be delayed. On the plus side, international commodity prices have rebounded, benefiting Australia’s mining companies.

Confidence measures continue to be mixed. Consumer confidence slipped further, with the Westpac Consumer Sentiment Index coming in at 96.2 this month (99.47 in the previous month). Capacity utilization is virtually unchanged. Coming off a recent high, the services PMI dropped slightly, from 51.70 in February to 50.2 in March. Business confidence, as reported by the National Australia Bank, increased from its temporary low of 0 to 3.

The Shadow Board’s confidence that the cash rate should remain at its current level of 2.25% is up three percentage points, to 67%. The confidence that a rate cut is appropriate has fallen from 16% in April to 13%; the Shadow Board considers it more likely (20%, up from 19% in April) that a rate increase, to 2.5% or higher, is the appropriate policy decision for this month.

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 2.25% equals 29% (down from 31% in April). The estimated need for an interest rate increase lies at 55% (up from 53%), while the need for a rate decrease is estimated at 16% (unchanged). A year out, the Shadow Board members’ confidence in a required cash rate increase equals 65% (up two percentage points), in a required cash rate decrease 16% (unchanged) and in a required hold of the cash rate 19% (down five percentage points).

65% chance of a rate increase in 6 months. These folks sure don’t look at the iron ore price. Markets are now pricing an 80% chance of a cut tomorrow. I agree.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.