The equity is expected to bolster NAB’s balance sheet and give new chief executive officer Andrew Thorburn and chief financial officer Craig Drummond optionality as they study a number of potentially significant deals.

NAB last raised equity in 2008 when it took $3 billion in an institutional placement through Merrill Lynch, UBS and Goldman Sachs.

…Morgan Stanley’s equities research team reckons the Big Four banks will need to raise $38 billion by the end of their respective 2017 financial years.

Apparently some of this is cover guarantees for the UK operation that NAB is exiting,from The Australian:

To enable the exit of Clydesdale, NAB (NAB) is providing £1.7bn ($3.2bn) to cover potential future losses from legacy conduct costs, such as the mis-selling of payments protection insurance.

The equity raising will help fund the £1.7bn — which will be deducted from NAB’s common equity tier one (CET1) capital ratio — and provide the group headroom against rising future capital requirements.

I very much doubt that the bank is doing this voluntarily. This is financial system stabilisation and good work by APRA. Now is the time while equity prices are high and the chase for yield intact. The fact is the banks have paid too much out, have run down capital and now the shareholders must pay.

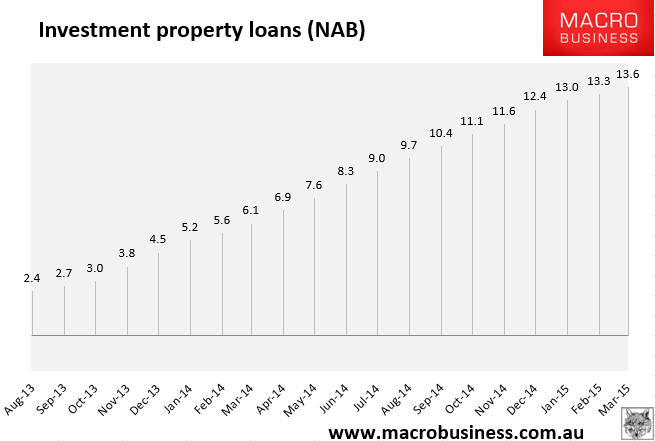

Now, APRA, you’ve got to shove NAB back from its runaway 13.6% investor mortgage growth:

The highest among the majors and definitely requiring redress with above average capital charges.