The credit rating agencies are clearly becoming concerned by Australia across the board. S&P is hammering the Budget and Moody’s is intensifying its critique of the bubble. From a new report:

Australia is going through a period of sustained house price appreciation and increases in household debt. These trends pose a threat to Australian banks because they increase the risk of an eventual correction in the housing market. Although Australian banks’ asset quality metrics and portfolio quality currently remain strong, we expect the tail risks embedded in the housing market to pose an increasing credit challenge over time. In this context, more banks are finetuning their underwriting discipline and capital adjustment to preserve their credit profiles, which will provide some relief to their ratings.

»

Australia’s housing market risks are skewed towards the downside. Elevated and rising house prices are intensifying imbalances in the housing market. Mortgage affordability is declining: despite low interest rates, the fraction of income household used to make mortgage repayments is increasing (27% nationally and a record 35% in Sydney). In addition, aggregate housing debt levels are now at an all-time high of 140% of disposable incomes. Low affordability has led to imbalances in mortgage product takeup with a sharp drop in the number of first home buyers, who are finding it increasingly difficult to access the housing market, offset by rapid increases in residential property investment activity.

» These developments pose a long-term challenge to Australian banks’ credit profiles. In the short run, stability in the housing market will be supported by low interest rates and the healthy state of Australian households ‘ balance sheets. In the long run, however, addressing affordability imbalances will necessitate house price growth more commensurate with income growth. While we expect such an adjustment to be gradual, execution risk is significant and the likelihood of an outright house price correction is rising.

» Underwriting discipline is a key mitigating factor. Latest data suggests that banks have turned more conservative in their underwriting, and curtailed their exposure to high loan-to-value ratio (LVR) loans. However, growth in investment lending remains high. We expect banks to adjust their origination practices to comply with APRA guidelines released in December 2014. We see ongoing adjustment to banks’ underwriting practices as supportive of high rating levels. Conversely, signs of loosening underwriting would be a material credit and rating negative.

»

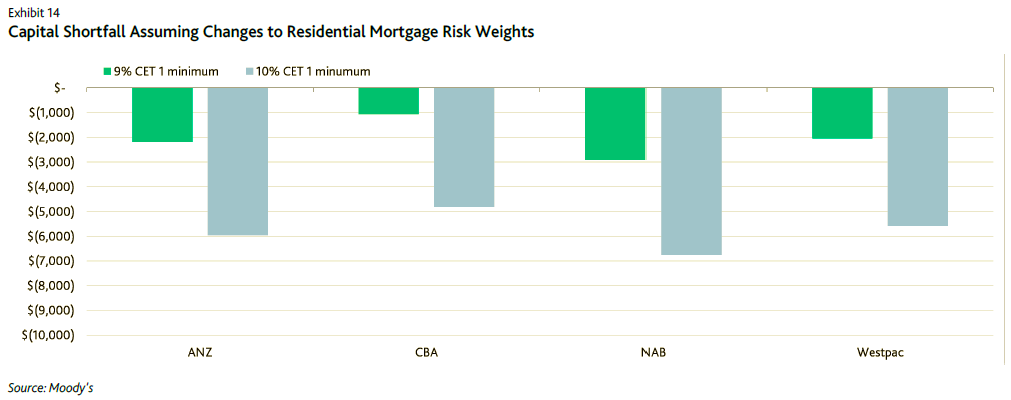

We see capital as the key variable to maintaining the health of the banks’ credit profiles. We expect Australian banks to revise up their mortgage risk weights and capital levels to better recognize the rising tail risks embedded in their housing portfolios. Our assessment is that average end-point mortgage risk weights for Australian major banks are likely to land in the 20%-25% range, up from the current 15%-20%. This would have a modest capital impact that would require an increase in capital of

approximately AUD8 billion, which banks are well-positioned to absorb. More likely, however, is a broader increase in capital requirements beyond mortgage risk weights, which would necessitate deeper adjustments to the banks’ dividend policies, and potentially the raising of new capital. We see the dividend policy initiatives and, in the case of National Australia Bank, a capital raise, announced by Australian banks as the start of a capital accumulation phase that is likely to extend well into 2016.

You can’t put it more plain than that. Australian needs strong macroprudential tightening or the downgrades will flow.

The kicker of course is that in our circumstances of a massive mining bust, strong macroprudenital tightening will bust the property market, which is why our regulators are dragging their feet.

That’s what you get when you blow the dumbest property bubble in history.