Cross-posted from Investing in Chinese Stocks.

The monetary reforms taking place in China are good, necessary and inevitable in the long run, but the immediate impact of an open capital account is in dispute, with many (myself included) expecting depreciation as a result if current forces remain in effect. One reason China may be rushing for SDR inclusion is it cannot keep the yuan propped up forever given the trend in the internal economy, private investment, monetary policy, overseas interest rates and the U.S. dollar.

Earlier this week I posted China May Pay A High Price For SDR Push, which centered on an Economic Observer article covering the risks of the SDR push, including the risk of currency depreciation. More evidence supporting this view is out at the WSJ: China Pushes Yuan Against the Tide

iFeng 翻译: 中国逆势力挺人民币

As pressure mounts on China’s currency to fall, Beijing is stepping up efforts to keep it strong.

On Thursday, the central bank set the yuan at its highest level against the U.S. dollar in more than a year, defying a raft of poor economic reports this week, signs of mounting capital outflows and the launch of a broad stimulus package aimed at juicing up the economy.

The forced upward path of China’s currency is challenging policy and financial-market norms. In other countries, monetary easing as aggressive as the stimulus package would typically send a currency tumbling, as it did in Japan, Europe and the U.S. But China is in the midst of a push to get its currency more widely traded abroad and to gain reserve-currency status with the International Monetary Fund, goals that could grow harder to reach if the yuan were to significantly weaken or show instability.

Beijing’s economic priorities are also changing. China is seeking to shift toward a consumption-based economy that isn’t so reliant on cheap exports and investments. This would give it more room to keep the yuan, also known as the renminbi, strong and stable.

Don’t forget money printing in years prior either. China does not have a market exchange rate and the debate over the yuan being under- or over-valued is an academic one when there isn’t a free market. Though even without a free market, the The Informational Power of the Offshore Yuan Exchange Rate can still pull the yuan lower as it did in 2011 and 2012.

A CASS researcher sees market forces pushing the yuan lower again. The headline asks: After full convertibility, will the yuan appreciate or depreciate?

iFeng: 人民币可自由兑换后是升值还是贬值?

CASS financial researcher Yi Xianrong writes: However, the internationalization of the RMB, the Chinese government should be faced with difficult choices. That is, if you want to keep the yuan’s strong and powerful, the yuan will not be fully liberalized, the yuan freely convertible schedule becomes quite uncertain, since after the opening the Chinese government will not be able to hold the initiative on the yuan.

…And to be included in SDR, its criteria for access the renminbi freely convertible. If the yuan freely convertible, the Chinese government will be incapable of keeping the yuan strong or preventing devaluation.

CICC’s latest report predicts that China will soon launch a series of measures to improve the yuan “freely usable” level, and by the end of the year the renminbi will be called a fully convertible currency.

From the CICC Report:

In conclusion

We expect that China will soon launch a series of major policy measures to enhance the yuan’s “freely usable” level, The yuan to join SDR. Although the “free to use” Without a clear definition, but it is SDR basket of goods

The main criteria credits (currently SDR currencies including the dollar, euro, sterling and yen). SDR assessment of this year’s big Shall be held in October, we believe the planned financial liberalization measures, such as the Qualified Domestic individual investors (QDII2) Plans and expand market access to qualified foreign institutional investors, will soon be implemented. We expect the renminbi Before the end of this year will be referred to as fully convertible.At the same time, China’s financial markets, especially the bond market will be rapid development, which will also Chinese state sector assets, restructuring of the balance sheet to support. Earlier this year, the Ministry of Finance increased the amount of government bonds issued, and launched a Local government debt swap plan Ge 7. Financial deepening is to provide adequate tools for domestic and foreign investors to invest an inevitable step.

These developments will boost the yuan as a reserve currency. If the yuan successfully joined the SDR basket of currencies will be international Social passed one yuan as “hard currency” favorable signals.Internationalization of the RMB will not be a simple linear Process, and may go through the accumulation and development for a longer period may be possible to reach a dominant currency in the current Competing critical point. RMB internationalization could still have a long way to go, but in any case, the rise of the renminbi are It will be a significant event noteworthy, for China, Asia and even the whole world will have a profound impact.

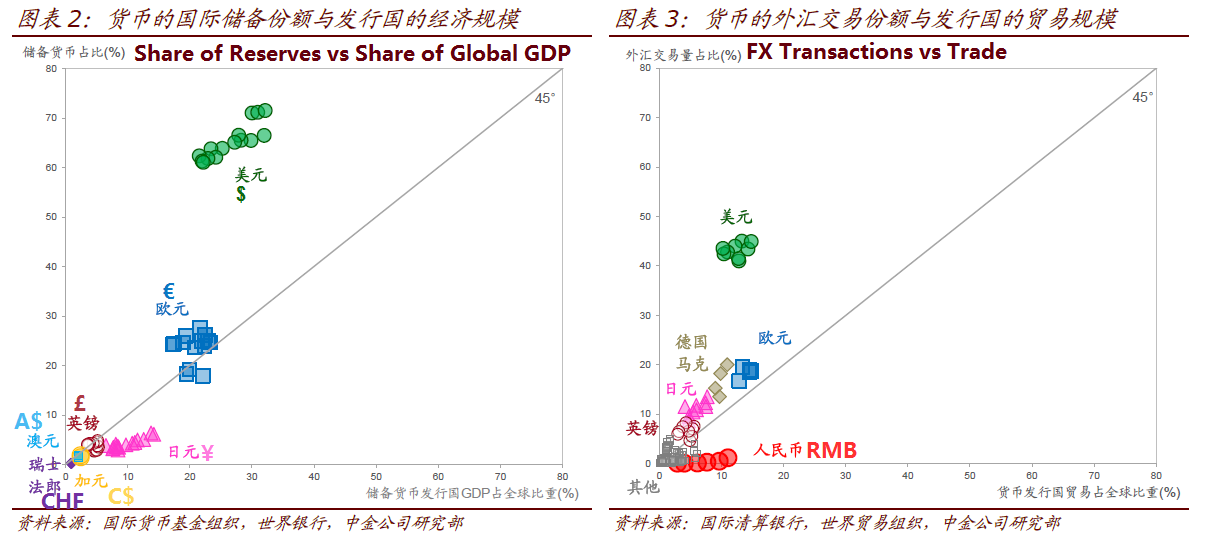

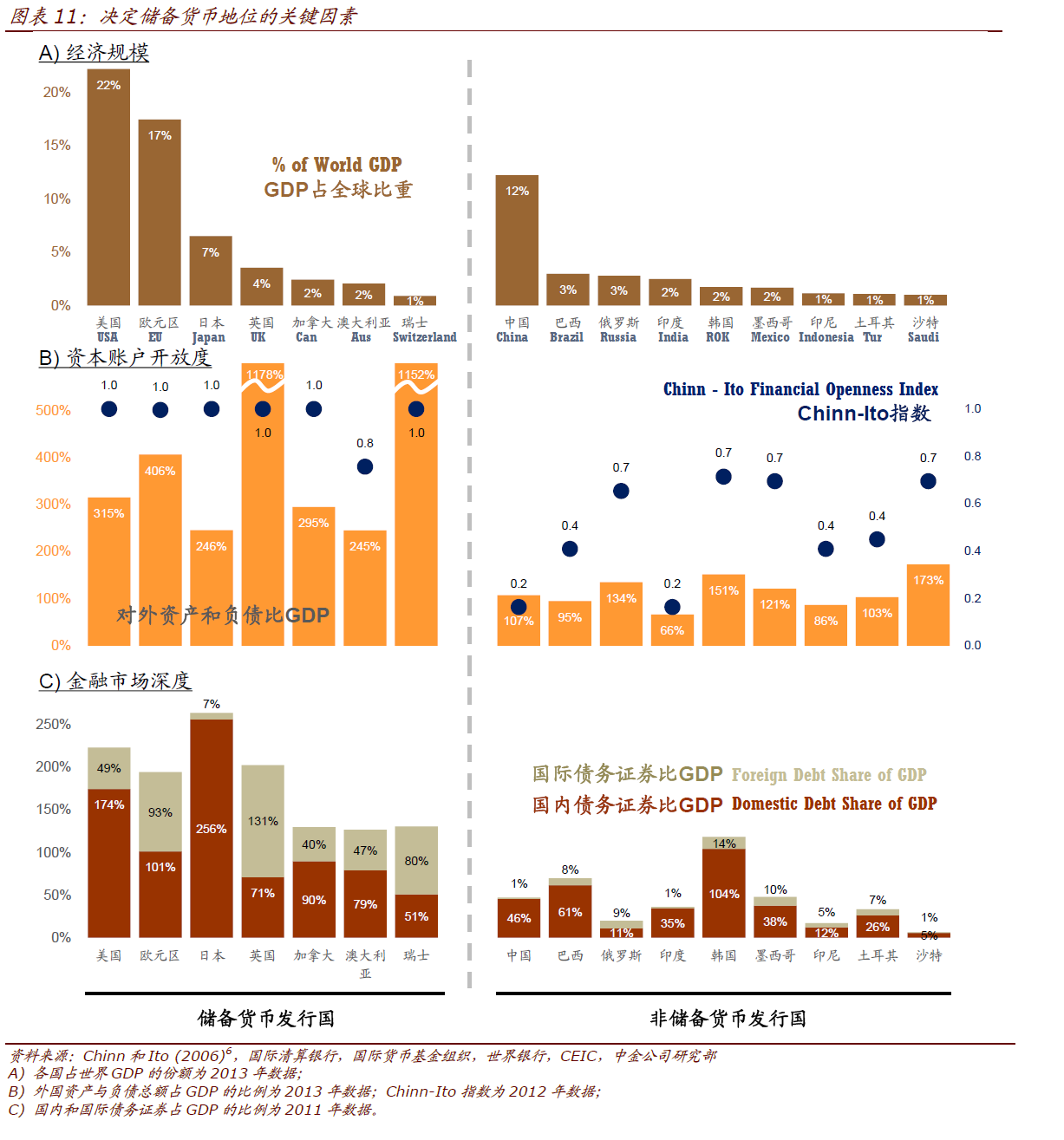

Also from the CICC report are some charts showing why China can make a strong case for inclusion of RMB in the SDR basket:

Back to the Yi Xianrong article (bold in original):

Therefore, investors must be aware that even if the yuan included in SDR, does not necessarily make the yuan appreciation, the renminbi is not necessarily a strong currency.

Now the most critical question is, under the current circumstances, further reform and opening of China’s financial markets, all kinds of capital controls lifted, or full liberalization of capital and the free convertibility of the yuan, the appreciation or depreciation of the RMB is?

Because the current domestic and international market situation, one depends on what time the United States to raise interest rates; the second is to look at the trend of China’s monetary policy.

Start with the situation in the US, the current US employment data support the Fed’s exit QE policy, allowing interest rates to return to normal.

Thus, despite the Fed’s rate hikes are cautious attitude and pace, but in September this year to raise interest rates, but the probability is very high. If the Fed rate hike this year, the yuan to maintain the current strength is not easy.

If US interest rates and the dollar strong, there may be disadvantaged or devaluation of the renminbi (against the dollar) start. Especially in the case of the more the possibility of the yuan freely convertible.

We look at China in the global dollar market waiting for the occasion to raise interest rates, China’s central bank cut interest rates RRR has been very frequent. Cut interest rates three times in six months time.

And the central bank launched a comprehensive easing of monetary policy, interest rates drop after registration, real economic data has not significantly improved, for example, downward pressure on economic growth did not slow down, CPI for 8 months at “1” level, PPI lasted nearly 40 months of negative growth.

Import data released last week continued to deteriorate for many months, which shows the lack of domestic demand. If the government to reverse this economic situation, we will further launch a series of policies of excessive credit expansion, such as RRR cut interest rates, market liquidity will certainly increase, coupled with the recent analysis of a large number of institutions of international hot money out of China, devaluation The probability will rise.

Therefore, if the yuan at the end of free convertibility of the RMB appreciation not exist but the risk of devaluation. In this regard, the investor is to pay attention

Another article asks “Why Hasn’t China Joined The Currency War? 为何中国没有加入全球“货币战”大军? The answer is the SDR.