Bonds and stocks crash! Australian dollar rockets! Budget toast! Jobs market improving! Iron ore busts, no booms! RBA cuts, no hikes! Pass the popcorn!

The financial press and its many market sources are all over the shop this week trying to explain the volatility that is consuming the Australian economy. As usual most of it is short term and based on quick cycles. None of it looks at structure and hence it’s as confusing as Hell.

One guy that does aim to cut through is Michael Stutchbury, editor at the AFR, who offers a potted history of the Australian economy:

…the two decades of great prosperity divides into distinct halves: a homegrown productivity dividend from the economic reforms of the 1980s and ’90s, followed by the crazy luck of the biggest resources boom in Australia’s history.

The reform agenda kicked off by Bob Hawke and Keating deregulated much of the Australian economy and opened it up to the disciplines of foreign competition. Until then, the car industry, for example, had responded to the competitive threat from more efficient Asian car factories by politically lobbying for protection. So, under Malcolm Fraser’s government, tariffs and quotas guaranteed up to 80 per cent of domestic car demand was met by costly local car makers. Under Hawke’s industry minister, John Button, Labor began dismantling this protective tariff wall.

…the Keating tax reforms of the mid-1980s sharpened incentives throughout the economy by lowering the 60 per cent top rate of personal income tax, paid for by a broadening of the tax base to include capital gains and employees’ fringe benefits. They also ended the double taxation of company profits through dividend imputation. All this helped drive the productivity-based prosperity of the 1990s.

At that very time, Australia was about to be blessed by the extraordinary but then little-appreciated chain of events set off by new Chinese leader Deng Xiaoping from 1978. After being impressed by Lee Kuan Yew in Singapore, Deng and his fellow reformers liberalised the Chinese economy, ended farm collectivisation, opened up to foreign investment and allowed entrepreneurs to set up business. The world’s most populous – but politically repressed –nation started posting a string of 10 per cent annual growth rates driven by investment in industrial equipment, urbanisation and manufactured exports. Through the 2000s, China became the world’s factory, its biggest steel producer and biggest exporter.

…It was as good as it got. Amid the triumphalism, the peaking of the iron ore price in 2011 was about to expose the weak flank of Australia’s great prosperity. In the rush of Australia’s biggest ever resource development, the economy’s productivity performance had sagged.

…So, unless productivity growth recovers, living standards this decade will grow more weakly than in any of the previous five. Even if productivity growth recovers to its longer-term average, Australians’ per capita income will struggle to grow by 1 per cent a year, as in the doleful 1970s and ’80s.

…The question for the Abbott government is whether it can properly respond to the public’s gradually rising alarm before Australia’s great prosperity degenerates into a genuine crisis. This requires the budget to be put back on the rails and for governments to embrace a 1980s-style wave of productivity-enhancing policy reforms that would help Australians grab the opportunities of the new digitally disrupted business world and to exploit the demands of Asia’s rising middle classes.

Very good and true and much needed in the debate.

However, it misses one very important boom. Australia’s golden era was not a game of two halves but three. There was the productivity boom of the late nineties, then the housing boom across the millennium and then the commodities boom after 2003.

You can’t miss out the middle step. If you do you miss out on today’s crucial dynamic in the economy because that housing boom never stopped. It has continued non-stop through fifteen years, powered by offshore borrowing by liberalised banks that have transformed into giant current account deficit driving machines.

While Australian productivity has declined, we’ve been saved by a mining boom and massive household borrowing for mortgage speculation. In terms of how we compete in the global economy, that has worsened everything, inflating every input cost, keeping interest rates and the currency higher than anywhere else.

This has caused a hollowing out of non-mining tradables so severe that as mining income declines there is bugger all to take its place in generating income.

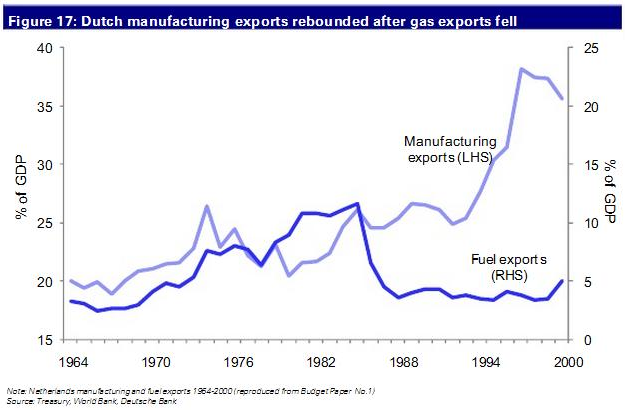

A quick example of the famous “Dutch Disease” episode in Holland makes the case. Ironically, Dutch Disease for the Dutch was short, sharp and quickly cured:

It was over in seven years and by the time the Dutch gas boom ended its manufacturing sector had rebounded and then powered up.

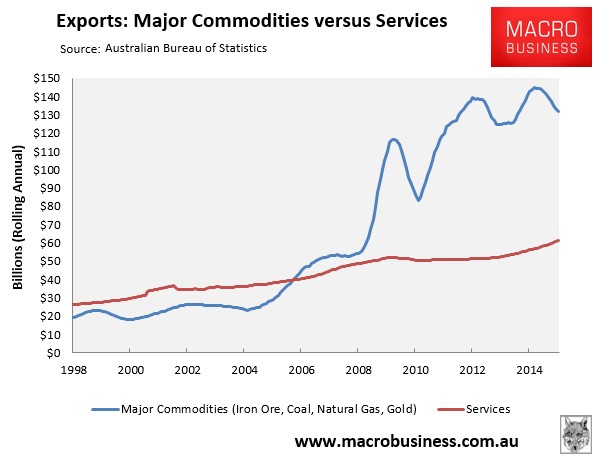

In Australia the Dutch Disease is vastly worse. Manufacturing has been driven to down to 7% of GDP on its way to 5%. And services export income can’t fill the gap as commodity values decline:

This is not to say that Stutch is wrong. He’s right. The answer is productivity gains. Lot’s of them, to release income growth at home and increase competitiveness so that we increase our earnings abroad.

What Stutch’s omission does do, however, is to disguise just how bad is Australia’s situation. The gap between our living standards and productive economy is gigantic, filled not by income but by mortgage debt, borrowed offshore and, more recently, guaranteed by the Budget, which is now also sinking as it seeks to fill the growing income hole.

So, as you survey the growing volatility in Australia’s vital macro statistics, remember that the third boom,ommitted by Stutch, has given us what Michael Pettis describes as an “inverted balance sheet”:

A hedged balance sheet is simply one that is structured to minimise the overall volatility of the economic entity, whether it is a business or a country.

When the balance sheet is fully hedged, the only thing that changes its overall value is a real increase in productivity. Any exogenous shock that affects the value of liabilities and assets, or that affects income and expenditure, will have opposite effects on the various assts and liabilities, and together these will add to zero. Of course the closer an economic entity is to having a perfectly hedged balance sheet, the lower the cost of capital, the lower the rate at which expected earnings or growth is discounted over time, the easier it is for businesses to maximise operating earnings without worrying about unexpected shocks, and the longer the time horizon available for both policymakers and businesses in planning.

An inverted balance sheet is the opposite of a “hedged” balance sheet, and involves liabilities whose values are inversely correlated with asset values. These embed a kind of pro-cyclical mechanism that reinforces external shocks by automatically causing values or behavior to change in ways that exacerbate the impact of the shock. When asset values rise, in other words, the value of liabilities falls (or, to put it differently, the cost of the liabilities rise), and vice versa.

It is housing debt that has done this and as the income that sustained the borrowing drains away the volatility will get worse and worse.

That is why MB spends so much time and effort tracking iron ore market dynamics. In the end it is everything. It is the sustaining income that keeps the inverted balance sheet aloft and while it falls volatility can only rise.

So, when watching the media chickens run around with their heads cut off squawking at which price is going where on any given day just remember that as iron ore reverts to mean at $30 (and below) the following is virtually certain over the cycle: lower interest rates, higher bond prices (until we run out of rate cuts), a lower dollar, a ruined Budget, sovereign downgrades and, sooner rather than later, much higher unemployment, deflating assets and very troubled banks.