This week is the all important private capex update from the ABS and today Bloxo offers an orthodox take on where it’s headed:

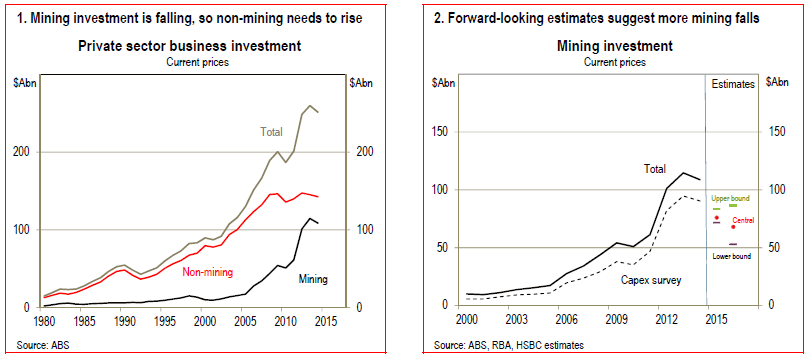

After driving growth for several years, mining investment has peaked and is declining significantly, in line with falling commodity prices. The rebalancing of growth away from mining investment is progressing, but only slowly. Low interest rates have sparked greater housing investment and stronger household demand, but the next stage of the rebalancing of growth – a ramp-up in non-mining business investment – has, so far, been tepid. This is despite low interest rates, strong population growth and limited investment in recent years: the key ingredients in the usual recipe for a business investment upswing.

Indeed, non-mining business investment has barely grown since 2008. This is not just a story in Australia, but one that is reverberating around the world. One of the major factors has been low business confidence. Years of uncertainty over the state of the global economy, the domestic outlook and government policy have contributed to this.

The collection of forward-looking indicators of non-mining business investment intentions continue to suggest little growth over the coming year. But, because there is significant herd behaviour in investment planning, these measures need to be watched carefully as small changes in sentiment can often presage large swings in investment intentions. There are also measurement challenges. The often-cited ABS capital expenditure (capex) survey showed weak forward-looking readings for 2015-2016 in February, but only covers about half of all non-mining capex and suffers from severe measurement error. Watching employment trends is also important, as capital investment often goes hand-in-hand with hiring. The recent lift in jobs growth is a positive sign.

For Australia’s growth to return to trend, greater investment in new capacity will be needed. The level of interest rates does not appear to be a constraint. This year’s more positive fiscal plans, including support for small businesses, may help lift investment. But, overall, what is clearly needed is a lift in business confidence. How to spark that remains highly uncertain, though when it comes, it usually does so quickly.

Some nice charts there but it’s not terribly difficult to critique the argument. If it were only confidence that were missing then we’d have cured that long ago. What’s missing is viable economic structure and everybody knows it.

Put another way, the demand side of the services economy (households) has too much debt and doesn’t want any more. So long as it won’t leverage up even more then there is oversupply in the economy and no need to invest. The capex survey is volatile but over the stretch it is very likely to miss expectations in this environment.

Advertisement

What we need is for rebalancing to focus on competitiveness not confidence so that we can tap external demand while households repair their balance sheets.

That something so obvious can be so overlooked is exceedingly odd. Full report.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

The collection of forward-looking indicators of non-mining business investment intentions continue to suggest little growth over the coming year. But, because there is significant herd behaviour in investment planning, these measures need to be watched carefully as small changes in sentiment can often presage large swings in investment intentions. There are also measurement challenges. The often-cited ABS capital expenditure (capex) survey showed weak forward-looking readings for 2015-2016 in February, but only covers about half of all non-mining capex and suffers from severe measurement error. Watching employment trends is also important, as capital investment often goes hand-in-hand with hiring. The recent lift in jobs growth is a positive sign.

For Australia’s growth to return to trend, greater investment in new capacity will be needed. The level of interest rates does not appear to be a constraint. This year’s more positive fiscal plans, including support for small businesses, may help lift investment. But, overall, what is clearly needed is a lift in business confidence. How to spark that remains highly uncertain, though when it comes, it usually does so quickly.