The survey was conducted over the period 11 – 16 May. The Reserve Bank announced a 0.25% cut in its cash rate on May 5 and the Federal Budget was announced on the evening of May 12. A number of initiatives in the Budget had been signalled by the government prior to its official announcement.

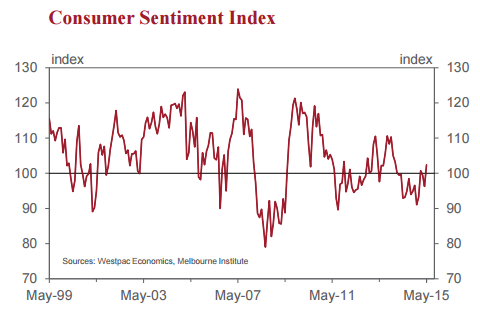

This is a very strong result. It is the first time since February this year that the Index has been above 100, the point above which optimists outnumber pessimists. It is the highest level of the Index since January last year.

The boost to confidence was apparent in all major states except Western Australia where confidence actually fell by a concerning 7.7%.

Clearly, the two driving forces behind this boost have been the Federal Budget and the interest rate cut which the Reserve Bank delivered in the first week in May.

We have a separate question in this survey which confirms the significance of the Federal Budget. The question specifically asks about the expected impact of the Federal Budget on family finances over the next 12 months. We have asked this question for the last six Budgets. With a net balance of minus 22.5 the score associated with the 2015 Budget is the highest since 2010. That score contrasts with the 2014 Budget of minus 56.1.

In recent times the Index has, typically, fallen in May (down in six of the last 10 years) with the Budget usually the key explanation. The surge in the Index this year represents the first time we have had a strong result in May since 2007.

The 6.4% lift in the Index is comparable with the boost to confidence from the generous budgets of the Howard/ Costello era where the Index surged by 7.5% (2007); 8.1% (2005) and 5.3% (2001).

Whilst undoubtedly positive the impact of the rate cut is likely to have been dominated by the response to the Budget. For example, the confidence of those respondents who hold a mortgage increased by a solid 4.8% although that rise was somewhat less than the overall lift for all respondents of 6.4%.

It was also encouraging that the Westpac Melbourne Institute Index of Unemployment Expectations fell by 5.8% to 147.3. (A lower read indicates more confidence around the employment outlook). The Index is now 3.2% below its average read over the last year but it is still pointing to fragile conditions in the labour market. For instance, this fall has only really largely offset the sharp increase we saw last month.

The finance and economic outlook components of the Index were strong. “Family finances vs a year ago” improved by 5.8%; “Family finances over the next 12 months” lifted by 2.2%. The outlooks for economic conditions over the next 12 months (up 9.2%) and next five years (up 20.2%) were both encouraging.

Surprisingly, the component “whether now is a good time to buy a major household item” fell by 1.0%. Whereas the overall Index has printed its highest level since January last year this component of the Index is14% below its January level. Confidence in housing recovered somewhat.

The Index “Whether now is a good time to purchase a dwelling” increased by 5.0%. The interest rate cut would have been a key factor in this regard. However, the Index is still 9.4% below its level in February following the previous rate cut.

The print on the Westpac Melbourne Institute Index of House Price Expectations fell by 3.2%.It is now only 3% above its level from a year ago. That move seems to be consistent with the somewhat cautious sentiment emerging in some housing markets.

The Reserve Bank board next meets on June 2. Having cut rates at its previous meeting in May there is little to no chance that the Bank would move again in June .The minutes from the May board meeting highlight that the Bank is relying on an ongoing boost to household expenditure to encourage businesses to invest and employ setting the economy onto a path of a falling unemployment rate and above trend growth in 2016.

Such a scenario would be consistent with an extended period of steady interest rates. The results from this survey will certainly provide some encouragement for the Bank that households might continue to lift the pace of expenditure growth.

“Our view, for now, is that the most likely scenario is for an extended period of steady rates whilst recognising that conditions in the labour market remain fragile and this latest boost to confidence will need to be sustained.

You’ll forgive me for being underwhelmed. The survey also coincided with a massive bounce in the iron ore price.

So, house prices going gangbusters, iron ore price through the roof, rate cut, easy Budget that allayed fears of a repeat of last year. What’s not to like? A six point bounce is a fair return but if any of this is going to stick we’ll need to see much more.

As iron ore resumes its downtrend the consumer bounce will fade in short order and there are more rate cuts to come, very likely this year. The dollar actually fell 10 pips on the release, quite rightly, not helped by the WA crater.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.