Financial markets are pricing in a 75 per cent chance of a rate cut when the RBA meets next week, which would be its second such move this year. However, the CAMA RBA Shadow Board advises against this. The central dilemma for the RBA persists: spur growth with loose monetary policy and risk exaggerated asset prices that lead to a misallocation of capital and costly adjustment in the future, or hold the line on monetary policy and risk an imminent weakening of aggregate demand.

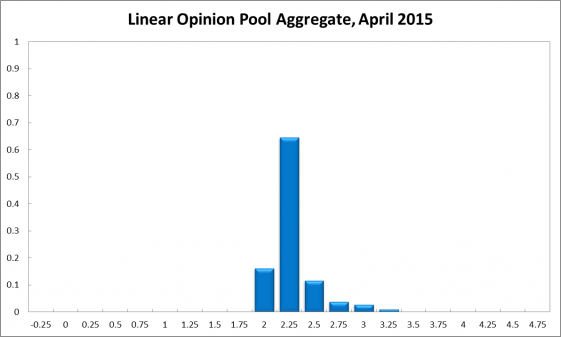

The CAMA RBA Shadow Board on balance prefers to hold firm but still considers it necessary that the cash rate is lifted in 6-12 months. In particular, the Shadow Board recommends with confidence that the cash rate be held at its current level of 2.25%; the Board attaches a 64% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals 16%, while the confidence in a required rate hike stands at 19%.

Australia’s jobless rate, according to the Australian Bureau of Statistics, edged down to 6.3% in February, due both to an increase in employment and a marginal decline in the participation rate.

There are no signs that wage growth is wakening from its torpor, making it unlikely that consumer spending will pick up significantly. The Aussie dollar continued to slide and now fetches about 75 US¢. As yields on Australian 10-year government bonds are now down to 2.35 percent, barely 40 basis points higher than for US Treasuries, global investors will search for yield elsewhere. A further decline of the Aussie dollar may well be on the cards.

Sydney’s inflated housing market remains cause for concern, as prices rose 3.3% month-on-month in March alone. The local stock market is also performing strongly, the ASX200 closing at 5900 just before Easter.

Global weakness and uncertainty keep battering the domestic economy. European growth remains soft while Germany is searching for solutions to the Greek debt crisis. Brazil is faltering and Russia, suffering from weak energy prices and political scandals, is experiencing a dramatic slowdown. China will aim for an annual growth rate of 7%, in line with previous announcements, while the US economy continues to expand modestly. The Federal Reserve Bank’s rhetoric points to a measured increase in the cash rate in the near future.

Confidence measures continue to be mixed. Consumer confidence slipped marginally, with the Westpac Consumer Sentiment Index coming in at 99.47 this month (100.7 in the previous month). Capacity utilization edged up from 79.94% in January to 80.42% the following month. The manufacturing PMI increased to 46.29 in March from 45.51 in February, while the services PMI advanced significantly, from 49.50 index points in January to 51.70 index points in February, the highest in more than a year. At the same time business confidence, as reported by the National Australia Bank, decreased to 0, the lowest in more than a year.

The Shadow Board’s confidence that the cash rate should remain at its current level of 2.25% is unchanged at 64%. There is far less confidence (16%, up from 14% in March) that another rate cut is appropriate whereas the Shadow Board considers it more likely (19%, down from 22% in March) that a rate increase, to 2.5% or higher, is the appropriate policy decision for this month.

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 2.25% equals 31% (unchanged from March). The estimated need for an interest rate increase lies at 53% (down from 56%), while the need for a rate decrease is estimated at 16% (up from 13%). A year out, the Shadow Board members’ confidence in a required cash rate increase equals 63% (down one percentage point), in a required cash rate decrease 16% (up four percentage points) and in a required hold of the cash rate 24% (down two percentage points).

All care and no responsibility in shadowland where Australia exports unicorns not iron ore.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.