Westpac has released its superb consumer Red Book and it does not make very good reading.

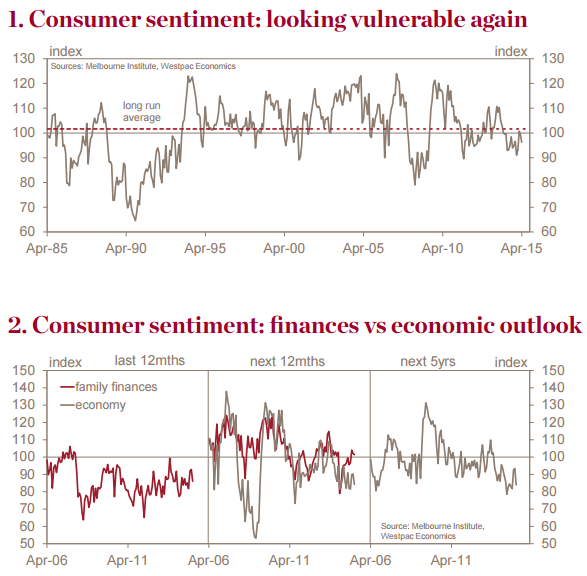

― The Westpac–Melbourne Institute Consumer Sentiment Index recorded a mildly disappointing 3.2% decline in Apr taking the index to 96.2 from 99.5 in Mar.

― While modest, the decline takes sentiment from around the ‘neutral’ 100 level to a more firmly pessimistic read.

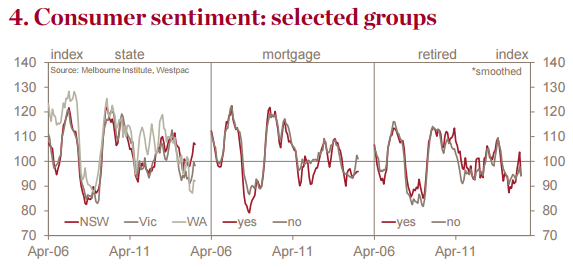

― Several factors likely contributed to the decline, including: the RBA’s decision to leave rates on hold at its Apr meeting despite market expectations of a follow-on cut; rising petrol prices which have now reversed all of the decline seen earlier in the year; the continued slide in iron ore prices; and possibly some concerns about the Federal Budget due out next month (recall that sentiment fell sharply following last year’s Budget).

― The state breakdown shows a widening divergence with sentiment relatively upbeat in NSW, a touch below neutral in Vic and Tas but firmly pessimistic in Qld, WA and SA.

― Our CSI± measure – a modified sentiment indicator that we favour as a guide to actual spending – was essentially unchanged and continues to point to modest, sub-trend growth in per capita spending of around ½%yr, implying growth of just over 2%yr in aggregate consumer spending.

― The sub-index on ‘time to buy a major item’ rebounded 5.9% in Apr after a surprisingly weak 5.1% fall in Mar. Recent declines in the AUD and the link to the cost of imported goods may have been a factor in recent months.

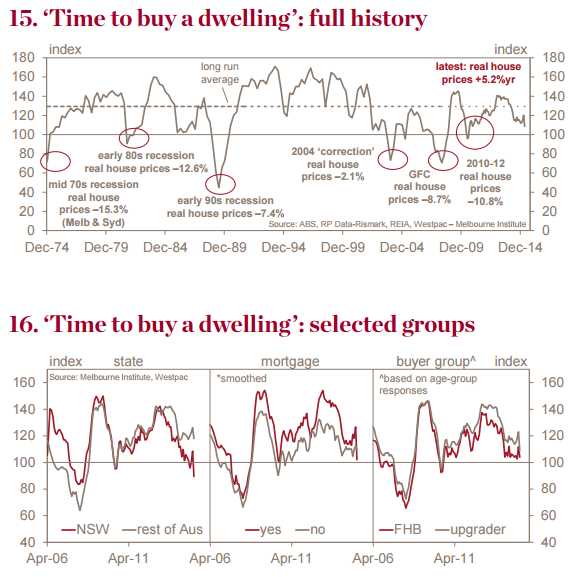

― The ‘time to buy a dwelling’ index fell 10% in Apr to be materially below its long run average. Buyer sentiment nationally points to a cooling off in demand. However buyer sentiment in NSW is below the ‘neutral’ 100 level and points to more pronounced weakness.

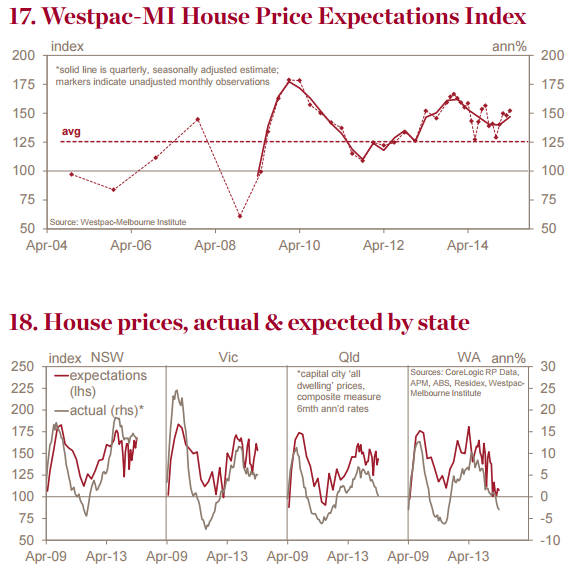

― The Westpac-Melbourne Institute Consumer House Price Expectations Index rose 2.8% in Apr to 152.1, the highest reading since this time last year. Consumers in NSW are the most bullish with expectations less bullish in Qld and weak in WA, where optimists and pessimists are nearly evenly balanced.

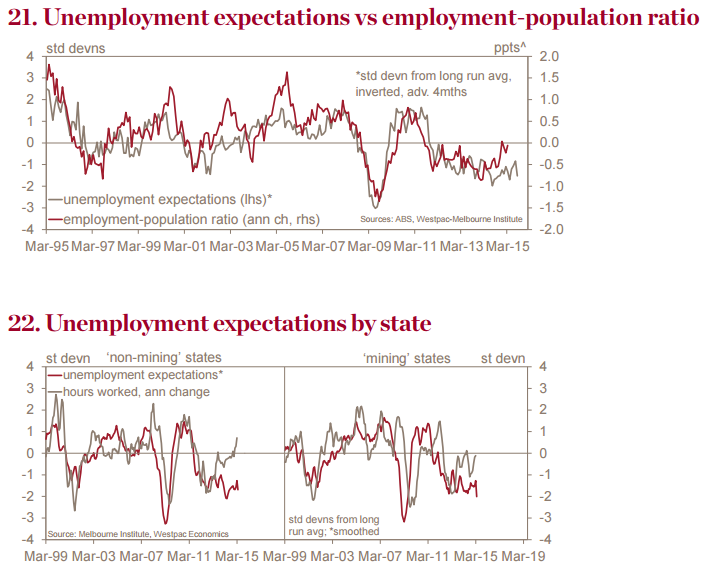

― The Westpac-Melbourne Institute Unemployment Expectations Index jumped 8.5% to 156.3 (higher readings indicate more consumers expect unemployment to rise). The Apr jump is the biggest rise since Dec 2012 and reverses most the promising improvement seen over the previous 3mths. While below the highs in 2014 and the peak in mid-2013, the Apr Index is the 7th highest reading since 2009.

That looks to me like a very vulnerable consumer. One final note on implications for interest rates. Bill Evans is expressing a similar concern for the health of the consumer owing to the iron ore crash which has lowered all of his forecasts and led him to this:

Delaying the decision until May is consistent with a cautious approach near the end of a long easing cycle. The unexpected 21% fall in the iron ore price with its associated implications for the terms of trade and nominal income growth strengthens the case for more rate relief. Further complicating the picture has been the sudden jump in the AUD to near USD0.78 in the aftermath of the March Employment Report. Markets have sharply lowered the probability of a move in May. We doubt such a response given the complication of a revised seasonal treatment and the well – established observation that the RBA has rarely changed policy on the basis of a single Employment Report.

Advertisement

Sure, but the RBA knew of the iron ore crash at its last meeting and didn’t cut and the jobs report is just another reason to wait and see what happens to the real object of policy: house prices.

More to the point, Westpac is of the view that iron ore has basically bottomed so its bearings here are way off and its forecasts will have to drop much further.

Unless auction clearances weaken in the next few weeks then despite its weaknesses this Red Book does not look look to me enough to push the RBA to cut in May. But given the iron ore outlook is actually a lot worse than our Bill (and most others) think, in reality the central bank is falling further and further behind the curve, risking a tipping point in household attitudes.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.