April fool! The manufacturing recession rolls endlessly on and really is the butt of all jokes:

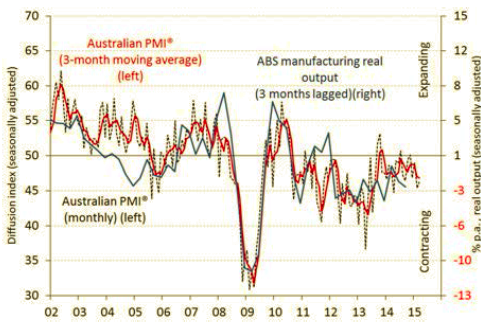

The Australian Industry Group Australian Performance of Manufacturing Index (Australian PMI®) moved up by 0.9 points to 46.3 points in March (seasonally adjusted). This indicated a fourth consecutive month of contraction in activity (readings below 50 points indicate contraction) across the manufacturing sector following a brief stabilisation in November 2014.

The Australian PMI® typically ‘leads’ ABS data for manufacturing output by around 3 months. Recent results from the Australian PMI® suggest growth in manufacturing output (measured as ‘value added’ by the ABS) is likely to be slightly negative again in the March quarter of 2015.

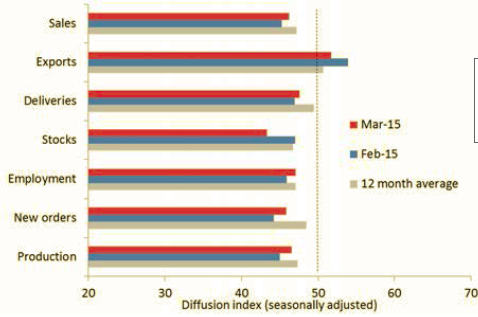

Manufacturing exports expanded for a fourth consecutive month in March as the impacts of the lower dollar continue to flow through. Much of this growth was concentrated in food and beverages exports, although other manufacturing sub-sectors also experienced a boost in the value of their exports, either due to higher export volumes or a lower dollar.

Other activity indicators in the Australian PMI® continued to indicate very weak domestic demand. Manufacturing production contracted (i.e. below 50 points) for a fifth consecutive month while new orders fell for a fourth month. Manufacturing sales declined for a 10th month in March. Supplier deliveries and stock levels also contracted for a second month in March after a brief expansion in January, while manufacturing employment contracted for a third month.

Four of the eight manufacturing sub-sectors in the Australian PMI® expanded (i.e. above 50 points) in March: food and beverages (for a 10th month); non-metallic mineral products (mainly building materials, for a fifth month); wood and paper; and printing and recorded media.

The lower Australian dollar continues to boost manufacturing export volumes. However, survey participants also noted that the lower dollar is increasing prices for imported inputs. And despite stronger residential building activity, weak local demand continues to weigh heavily on activity. This month manufacturers noted the further drop in mining construction, the progressive closure of automotive assembly, subdued local business investment in equipment, as well as political uncertainties in Canberra and in New South Wales ahead of the state election.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.