So much is written about China, and of late very little has been bullish. The notion of impending renminbi devaluation has taken root as traders worry that the dollar rally has pulled its reluctant Chinese counterpart higher, especially against the euro and the yen. Indeed, it seems that shorting the renminbi has become the new equivalent to the JGB short in macro circles. But having shared these doomsday prophecies back in 2010, when the consensus was less negative, I have recently become less concerned about China. Here’s why.

First China has recalibrated its growth model. Between 2001 and 2011, China had a very comparable decade to the US economy during the 1920s. Both boomed on surging productivity, high returns on capital, massive gross fixed capital formation and a fervent desire by the rest of the world to participate. We know that both economies should have boomed; indeed they did. However I would contend that they should have boomed even more.

That they didn’t was because of hawkish macro policy. In the 1920s, the Fed refused to allow the high powered money entering its economy via the gold standard to boost credit further. The Chinese discriminated against their household sector: the currency was never allowed to appreciate as much as the boom justified; wages never fully captured the dramatic gains in productivity; and real interest rates were consistently negative. Together, these measures robbed the household of anything between 5% and 7% of GDP per annum, statistically depressing income’s share of GDP and hence boosting involuntary saving. No one really complained, everyone felt better off, but they could have done even better.

However, with the rest of the world now languishing from insufficient demand, the policy is no longer practical and policy makers have acted consistently and repeatedly for the last two years to change this. The hand brake on Chinese household incomes has been lifted as the country pursues a different growth model. Clearly the currency is no longer deemed undervalued, and the surge in both the dollar and the renminbi has produced a tremendous redistribution in the global economy enriching US households and mainland Chinese consumers. Real and nominal interest rates are now high, and wages have been capturing more of the productivity bounty. Consumer spending is strong and probably underpins something like 4% GDP growth on its own. Why should policy makers undermine the one reliable motor of economic growth by choosing to devalue their currency? It just doesn’t add up.

Second, at the macro level not all countries are born equal. A select group of nations – the US, core European countries, Japan – belong to an elite ‘Tier One’ macro community. These countries have large non-tradable sectors and as demonstrated by the adoption of QE, have the firepower to determine interest rates without being constrained by the fear of inflation from a weakening currency. The appeal of China today rests on its graduation to this community. China is no Mexico, an oil exporting country feeling under pressure to raise interest rates in the face of a slowing economy and worsening terms of trade precisely because it fears the consequences of losing control of the peso. Rather, China seems to belong in the same camp as the US, Europe and Japan, the countries with the scope to determine their own monetary policy.

Nevertheless, economists have fretted as the renminbi has appreciated alongside the US dollar. The fear is that this will hit an already vulnerable domestic economy with a sharp reduction of the trade surplus. Valuing currencies is notoriously difficult as I tried to explain in my November report. Nevertheless I find it hard to demonstrate that the currency is substantially overvalued at a qualitative level. To start with, the trade surplus has gone on to reach a record nominal high. You may observe that this can be partly put down to a fall in the price of imports (of which more below), but China’s competitiveness in export markets seems to remain strong with its market share of global exports continuing to rise. Domestically, unemployment remains low in the major conurbations, and the GDP growth rate, whilst slowing and subject to the great bluster of its politically motivated national accounts methodology, still seems much healthier than elsewhere in the world.

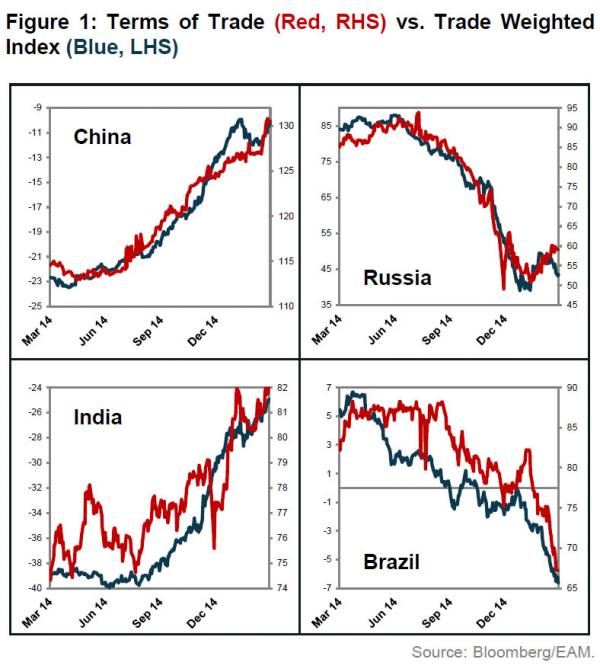

Perhaps it is more useful to look at the terms of trade. It has certainly done a good job at explaining the differentiation of emerging market currency moves over the last 18 months. The huge decline in China’s raw material costs, especially the slump in both iron ore and oil, have massively improved the country’s standing and the trade weighted currency has appreciated in tandem; it may be as simple as that. The same can be said for India where only the central bank’s accumulation of foreign exchange reserves has prevented further appreciation. In contrast, the free-fall in the currencies of Russia and Brazil seems to match the devastation in their terms of trade as their important raw material exports have suffered from tremendous deflation with no meaningful offset in other inputs.

Of course, the real bugbear for those less disposed to China’s prospects concerns the management of its currency peg with the US dollar. The combination of a bearishly disposed international macro community and the desire of businesses operating within China to hedge their FX exposure has pushed the currency to the top of its regulated trading band. The upshot of this has been that the PBOC has had to intervene: buying renminbi and selling dollars. This of course drains the Chinese economy of liquidity as can be seen by rate movements. For instance, despite two rate cuts and a reserve ratio reduction, the seven-day repo has risen 140bps to 4.8%. The withdrawal of liquidity can also be seen in the 10% fall in Shanghai A shares from the start of year to mid-February. Perhaps the macro community is right to worry after all?

Not so fast. Remember China is the only ‘Tier One’ economy not trapped by the zero lower bound, domestic interest rates are high by international standards and China has ample scope to reduce rates further. Indeed the policy looseness announced since last November’s first cut has pushed stock prices higher and the one year forward repo rate trades at 3.6% which suggests that domestic investors perceive this to be a temporary tightness in liquidity which will ultimately be addressed by the authorities.

Several years ago when seeking to chronicle the likely sequencing of crisis as deflationary forces swept across the globe we proclaimed “US first China last”. This has stood the test of time. Deflationary shocks in each of those economies caused sharp sell-offs in local financial markets, and brought forth a policy response which proved extremely beneficial for investors in those countries. Today, the global deflationary surge has finally humbled the Chinese growth engine, transforming the community of macro investors into bears and the local stock market has fallen 75% from the 2007 peak. In fact, the risk/reward set up in Chinese equities seems akin to investing in US stocks back in 2009, Japan in late 2012 or Europe in late 2014. Like then, the market seems to be underestimating the power of central banks to reduce policy rates and the likely positive reaction of risk assets.

Of course standalone delta one equity plays don’t always sit easily in a macro portfolio; the risk-reward is rarely sufficient for a manager who wants to have his cake and eat it. Eclectica is no different. Whilst we are long the equity market we hedge a lot of this risk by paying offshore interest rates. This allows us to run a more diversified risk book as well as exploit some of the peculiarities of the prevailing financial system and capitalise on the ongoing macro bearishness. Granted the notion of paying rates into a slowing economy that has high nominal rates (by international standards) and that has just embarked on a policy of rate cuts is contradictory to our argument so far. Allow me to explain…

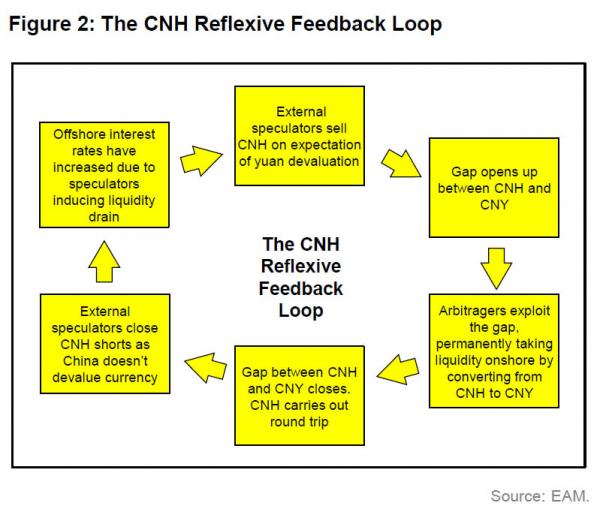

There are two prominent drivers. First, China is truly different. Its domestic financial system has been isolated from the rest of the world for many years and is riven by government intervention; it is almost unrecognisable to western eyes. Below the seeming order of the modern Chinese banking system lies a startling obfuscation of risk as well as a system of economic apartheid which rejects legitimate private sector credit demand from China’s household and SME sectors. Having shut out so much of the private sector from credit provision for so long it is not much of an exaggeration to suggest that there is a huge demand for liquidity at any price. Published rates simply do not reflect the much higher levels that many are willing to pay to access credit.

Fortunately the government’s attempt to open up the capital account has created a credit channel for this pent up demand. As the market liberalises and it becomes easier to bring liquidity onshore, the huge onshore market readily mops up the offshore liquidity pool, pushing offshore rates higher. Furthermore, the negative bias on China from asset managers and the renewed vigour of exporters to hedge their currency gains periodically leads to the currency trading cheaper offshore than onshore, creating an opportunity for arbitrage players to exchange their dollars for renminbi at a better rate. As the offshore currency is brought onshore, liquidity permanently leaves the international system and again pressures rates to rise further to the benefit of our paying position.

Think of our China trade as analogous to playing pinball. You get three balls and the objective is to maximise one’s score by having the balls strike different angles on the playing field. With the first ball, we are holding a long renminbi position via options. Above, I have argued that the currency is fairly valued. It is hard to rationalise that the authorities will seek to devalue in trade weighted terms. Indeed, when consideration is given for the extraordinary boost in the country’s terms of trade I am unsure that it even needs to lose ground versus the rapidly appreciating dollar. As we all know the macro community tends to have a short time span for blow-up trades and with the currency having come off the upper trading band in March, and the PBoC no longer intervening, trade size is probably being cut and the currency will likely return/appreciate to the middle of its band.

With the second ball we are long the stock market. The market having fallen 75% from its peak had discounted the bad news and indeed was increasingly pricing in the possibility of bankruptcy. However the shift in policy to favour the private sector has probably averted such a catastrophic outcome, and with further policy loosening to come the equity market is starting to value these businesses as ongoing concerns with modest price earnings multiples once more. Stocks have rallied 35% on two small rate cuts despite poor inter-bank liquidity and rising short-term rates. I am enthralled at what they may do if policy is genuinely loosened and the credit market truly thaws out. The persistent error of the macro community since 2009 has been to underestimate the ability of Tier One economies to loosen monetary policy to avert crisis. The same outcome seems plausible today in China and equities appear attractive.

And finally with our third ball we are paying short term rates in the offshore market, which acts as a bearish hedge as well as aligning us with an opening up of China’s convoluted capital account. The willingness of Chinese domestic borrowers to pay up for available credit when it is made available has been demonstrated by the more liberal offshore market where rates already trade above onshore levels. Further liberalisation is likely to push rates higher until demand is sated. Paying rates therefore seems sensible. And in the unlikely event that the situation deteriorates and inter-bank rates spike higher as the authorities fail to produce sufficient liquidity to the onshore market, our payers will provide a welcome hedge against our equity and FX positions.

A more than fair argument and I agree. Essentially China is a tier one command economy so can do what it likes with its macro management (for a very long time anyway).

What this doesn’t do is improve anything for Australia. Given the argument is based upon the notion of a successful Chinese rebalancing away from the investment growth drivers that drive commodity demand, it is the same outcome for us as hard landing.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.