From national treasures Tim Toohey and Andrew Boak at Goldman Sachs:

Official projections for population look far too optimistic

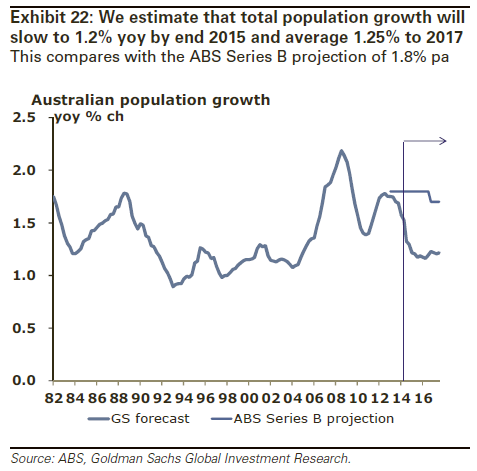

Australia’s population growth has been strong since 2006 and official estimates, including the widely used Series B projection from the ABS, assume population growth averages 1.7%-1.8% over the next three years.

However, we believe these projections are far too optimistic and forecast population growth will slow to 1.25% during the 2015-2017 period.

Birth rate is at historical lows and deaths at historical highs

Australia’s birth rate is declining at its fastest pace on record and the growth in deaths is at a cyclical high, resulting in a marked slowdown in ‘natural increase’. We demonstrate that a combination of a lack of income certainty and a one-off deferral by females in having children in the early 2000s explains most of the fall in births. We also suggest the rate of growth of deaths will easily double its historical average over the coming decade as the sheer number of individuals moving into age brackets with higher mortality rates swamps any further extension to average years lived.

Net migration is falling fast

Net migration has supplied 60% of population growth in recent years. However, our proxy for net migration suggests migration is now falling sharply. We show that over half of all net migrants are directly looking for a form of employment and over two-thirds enter Australia looking for either education or employment. As such, relative labour market conditions are a key determinant of net migration growth, and on this score the outlook is for further deterioration in net migration trends.

We cut potential growth and forecast a 2017 housing surplus

Relative to the path for population growth suggested by Series B, we estimate that Australia’s population will be 530,000 smaller by the end of 2017. There are two crucial consequences of such a change. First, we reduce our estimate of ‘potential’ economic growth from 2.9% to 2.5% over the 2015-2017 period. Second, we change our estimate of underlying demographic demand for housing from a 140k underlying deficit for established homes by the end of 2017 into a 75k underlying surplus. Both adjustments complicate the outlook for monetary policy.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.