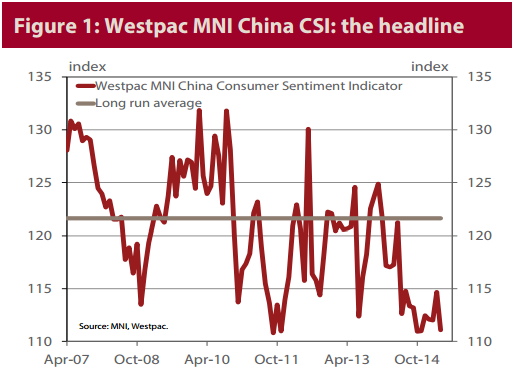

The absolute level of the Westpac MNI China CSI indicates that Chinese consumers are still anxious about their personal financial wellbeing and the economy more broadly.

The post Lunar New Year rate cut has clearly faded from the minds of consumers already, just as the November 2014 cut failed to inspire anything more than a one-month knee jerk gain.

Each of the five components that go into the calculation of the Westpac MNI China CSI decreased from their March levels. The major negative impulse was a steep decline in current and expected family finances, which more than reversed March’s rate-cut infused gains. Forward looking assessments of business conditions also declined, but to a lesser extent. Current business conditions (not part of the composite, but highly correlated with the PMIs and IP) were a touch firmer.

Investment preferences tilted in a risk-seeking direction in April. Both domestic real estate and, naturally, the booming share market, attracted a greater share of adherents than in March. However, the scale of these gains is relatively small, implying there remains plenty of room for a rebalancing of portfolios towards these asset classes. For now though, there is little sign that the spectacular gain in share prices is having more than a marginal impact on the conservative financial mind-set of the ordinary Chinese citizen. See page 8 for a range of insights on the booming equity market.

The employment indicator declined by a cumulative 11.3% between May and October 2014 and has since increased by just 2.2%. The April reading (–1.1pt from March) is 9.1% below long run average. Ergo, in absolute terms job security remains in short supply. Consumers are awaiting a more durable pick-up in growth before they fundamentally reassess the job outlook. We noted a month ago that the softer employment reading argued that the observed improvement in family finances was highly dependent on the interest rate cut. The weak aforementioned update on family finances validates that position.

The consumers’ attitude towards real estate (see table 3 on page 4 of the bulletin) was mixed in April, following on from the modest cumulative improvement in Nov-Mar. Expectations for house pricesdeclined; but the share of respondents reporting it was a ‘good time to buy a house’ moved higher; while more consumers nominated domestic real estate as the ‘wisest place for their savings’. Back on the negative side, the proportion of consumers nominating a housing purchase as their primary motivation for saving fell modestly, following on from four straight gains. We interpret these outcomes as somewhat disappointing, given the increase in max LVRs, which we hoped would produce a more definitive positive overall read. However, we note a) the firmer March official house price figures, b) that survey respondents expect listed real estate firms to perform well, and c) that policy has been eased further since this survey was taken. Will it be a case of delayed gratification?

Finally, regarding the specific responses around spending plans and buying conditions (table 6, page 6), there was mixed information on anticipated discretionary expenditures. Dining out (both traditional restaurants and western style fast food) was higher, “Shopping” was flat, while “Entertainment” spending plans were weaker. Buying conditions were mixed, with cars weaker, but major household items, IT products, other appliances and communications devices all flat or higher. Despite the more negative assessment of buying conditions in the auto market, the proportion planning to buy a car in the next 12 months increased from 12.8% in March to 17.3% in April, which is well above the long term average of 12.6%.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.