The Australian Energy Market Operator (AEMO) updated its long and short term gas outlook today and the is good, sort of:

In December 2014, AEMO published the first National Gas Forecasting Report (NGFR) for easternand south-eastern. The forecasts in the NGFR form the basis of the outlooks for annual consumption and maximum demand for the 2015 GSOO.

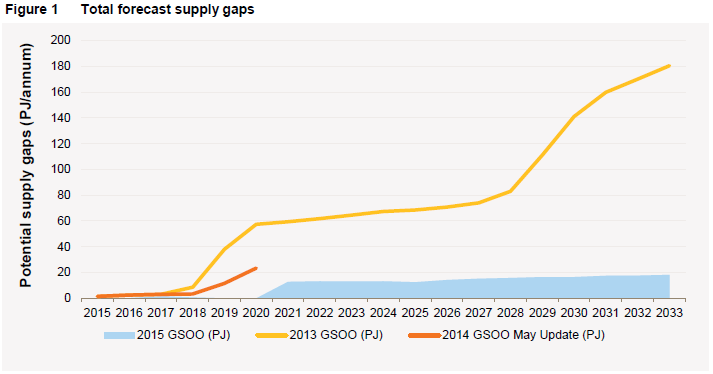

The 2015 GSOO signals ongoing shifts in consumption and supply positions in the dynamic eastern and south-eastern Australian gas markets. It details changes in supply adequacy over the short-term and further revises the 2013 GSOO’s medium-term and long-term supply assessments. AEMO expects that changes to infrastructure capacity and lower forecast consumption will result in short-term gas supply needs being met and potential medium and long-term gaps reduced.

A GSOO update published in May 2014 focused on the short-term effects of changes in forecast liquefied natural gas (LNG) exports and the withdrawal of the Swanbank E gas power station.

1.1 Gas consumption forecasts are lower

Forecast domestic gas consumption is lower than reported in the 2013 GSOO, which forecast industrial, residential and commercial gas consumption would rise to 615 PJ by 2033.

By contrast, the 2014 NGFR showed gas consumption for industrial, residential and commercial gas falling from 447 PJ in 2015 to 425 PJ in 2033.

Most of the change is due to a fall in industrial consumption across eastern and south-eastern Australian gas markets. This is particularly the case in NSW and Queensland, where a number of large gas industrial consumers are closing. The NGFR anticipates further declines in industrial consumption due to expected rises in domestic gas prices.

For LNG consumption, the 2013 GSOO forecast 1,446 PJ by 2033. The 2014 NGFR forecast LNG consumption of 1,425 PJ by 2033, further reducing gas consumption. This reduction is largely due to lower forecast gas required to power LNG export facilities.

1.2 System capability – pipeline capacity and storage have increased

The following infrastructure improvements will increase capacity for gas to flow to demand areas.

1.2.1 Victoria – New South Wales Interconnect upgrade

Upgrades to the Victoria – New South Wales Interconnect through Culcairn will be completed during 2015, providing increased flows to New South Wales by raising capacity from 57 TJ to 118 TJ per day. This reduces forecast gas supply gaps in NSW. More information is provided in Attachment B.

1.2.2 Moomba–Sydney Pipeline

Currently gas flow on the Moomba–Sydney Pipeline (MSP) is one-directional from Moomba to New South Wales. An upgrade of the MSP, due for completion during 2015, will allow gas to flow from New South Wales to Moomba, so gas produced in Southern Australia can be exported to Queensland.

1.2.3 Connection of South East Australia Gas pipeline and Moomba–Adelaide Pipeline System upgrade

The South East Australia Gas (SEA Gas) pipeline connects the Port Campbell production zone in Victoria with Adelaide, allowing bi-directional gas flow. The Moomba–Adelaide Pipeline System (MAPS) connects Adelaide with the Moomba Gas Plant, with one-directional flow from Moomba to Adelaide. These pipelines are expected to be directly connected later this year. Work is also underway to allow MAPS to flow in both directions, allowing for gas exports from Southern Australia to Queensland.

The NSW gas shortage is therefore fixed via the annihilation of manufacturing. Talk about a policy own goal.

Meanwhile the second of Australia’s hopeless manufacturing lobbies offers this:

Advertisement

Australia’s largest manufacturers have released a market reform plan they say could restore competition and confidence to the domestic gas market and help to avoid widespread manufacturing job losses.

The 13 point plan, launched today by Manufacturing Australia Chairman, Mark Chellew, urges joint action by Federal, State and Territory governments and industry, and says gas market reform should focus on four key goals: establishing transparent and functional gas markets; securing domestic and export supply, developing appropriate infrastructure and providing incentives for new production.

Mr Chellew described the gas supply and price challenges as a “severe threat” to domestic manufacturing, and warned that up to 83,000 direct manufacturing jobs could be lost if market reforms are not fast tracked to restore confidence amongst industrial gas users.

“The Energy White Paper has the right vision of a gas market with diverse suppliers, additional supply, appropriate infrastructure and competitive, transparent, trading markets,” said Mr Chellew.

“But we are a very long way from that ideal now and there is a lot of work to be done if the Australian gas market is going to enable long term manufacturing investment.”

The action plan outlines a highly dysfunctional gas market that has rapidly consolidated and transformed with the establishment of an export Liquefied Natural Gas industry.

“Just a handful of economic interests now control the vast majority of Australia’s current gas reserves, while regulatory barriers, infrastructure constraints and the lack of transparent markets and trading hubs prevent new gas supply, and new suppliers, from entering the market,” he said.

Amongst the recommendations are calls to establish functional, transparent, trading hubs for gas, fast-track gas infrastructure like the proposed Northern Territory pipeline, introduce “use it or lose it” policies to prevent gas being withheld from the market, and for governments to incentivise and stimulate investment in new gas production to get more competitors into the market.

Mr Chellew said last week’s announcement that the Australian Competition and Consumer Commission (ACCC) will examine competition in the Australian gas market is a very welcome start, but reforms must move quickly.

“None of this is easy. None of it is a silver bullet. But if we continue on the path we’re on Australia will lose much of our gas intensive manufacturing industries, and we’re not likely to get them back.”

It has dropped the call for domestic reservation which is the only measure that can work to stabilise local prices. Increased supply will simply trigger greater Asian exports.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.