Fresh from Westpac comes the leading index driving through the rear vision mirror:

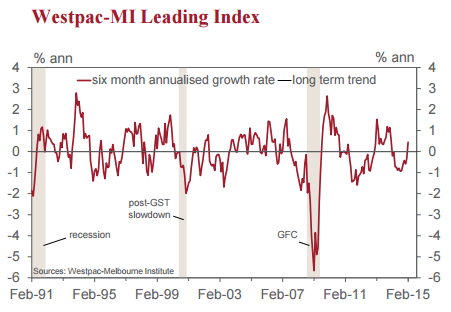

• The six month annualised deviation from trend growth rate of the Westpac Melbourne Institute Leading Index, which indicates the likely pace of economic growth three to nine months into the future, lifted from –0.32% in January to +0.45% in February.

This is the first above trend reading from the Leading Index since January 2014. After showing persistently weak, sub-trend momentum over the last 12mths, this is the most promising result in quite some time. It suggests that the Australian economy will start to regain some momentum towards then end of this year, although it remains to be seen how well this pick-up is sustained.

The 1.36ppt swing in the Index growth rate since September, from 0.91% below trend to +0.45% above trend, has been driven by five of the eight Index components. Just over half of the improvement has come from reduced negative ‘drags’ from commodity prices (+0.54ppts), which have been broadly flat in AUD terms, and from aggregate monthly hours worked (+0.26ppts). The rest of the improvement has come from solid post-rate cut lifts in the Westpac MI Consumer Sentiment Expectations Index (+0.33ppts) and the ASX200 (+0.21ppts), and from a continued surge in dwelling approvals (+0.15ppts).

Contributions from the other three components were unchanged (the Westpac MI Unemployment Expectations Index and the yield spread) or slightly less positive (US industrial production).

The reduced drag from the Index’s commodity price component is particularly interesting. This component is measured in AUD terms, so it captures both fluctuations in international prices and how these are buffered by shifts in the Australian dollar. Through most of 2014 currency moves did little to buffer sharp falls in global commodity prices with prices falling 12.8% in the six months to September in both USD and AUD terms. That dynamic has changed significantly since then. Although commodity prices have continued to fall sharply in USD terms, down a further 13.6% since September, declines have been more than matched by falls in the AUD/USD cross rate, down 16.3% over the same period.

For the February month in isolation, the Index rose 0.27% from 97.94 to 98.21. Seven of the eight components contributed tothe monthly rise with the ASX200 up 6.1%, dwelling approvals up 7.9%, US industrial production up 0.07%, commodity prices up 0.15% in AUD terms, the yield spread narrowing 0.21ppts, aggregate monthly hours worked up 0.81% and the Westpac-Melbourne Institute Unemployment Expectations Index down 2.54% (recall that lower readings indicate a more positive view on the outlook for unemployment). The Westpac-Melbourne Institute Consumer Expectations index fell by 0.27%.

The Reserve Bank Board next meets on April 7. We continue to see a clear case for lower rates. The latest Leading Index report presents some positives, suggesting a declining AUD is doing more to buffer the effect of sharply lower commodity prices, and that the combination of lower interest rates and rising dwelling construction may be generating more traction domestically. However, we remain concerned about the weak pace of growth momentum, the ongoing hit to national income from sharp declines in the terms of trade and the still fragile state of consumer and business confidence. There remains a clear risk that sub-trend growth may persist for longer than had been assumed through most of last year. Accordingly, we continue to expect another rate cut of 0.25% in the April/May ‘window’.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.