Occasionally on this long journey, readers have accused me of an iron ore obsession. It’s true but the implied criticism is wrong. Iron ore and associated coal is 40% of Australia’s terms of trade, and although that will diminish as the crash proceeds and LNG rises, to not obsess over such a dependence as an economic adviser would be negligent.

The real question is why nobody else ever obsessed over it. The answer to that takes us deep into the labyrinth of Australian economic institutional capture which we do not have time for today. Let’s stick to the practical implications of the unfolding crash.

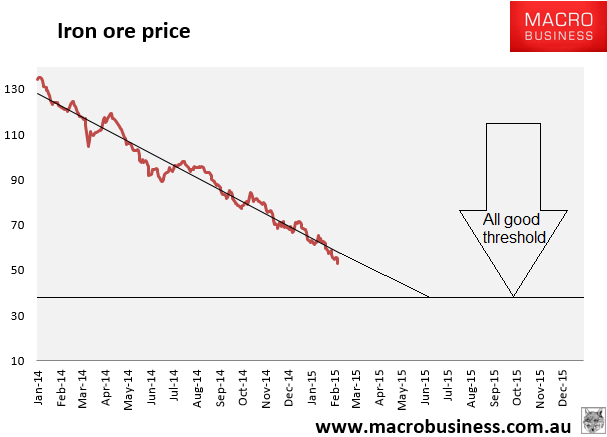

For those insiders that have missed the iron ore story, today let me put your minds at ease, an end to the pain of the iron ore price crash is in sight. Here is the trend since the arrival of the Fortescue glut in late 2013:

The “all good threshold” is around $37. At that price RIO ceases to be profitable and as the world’s cheapest producer that’s also when Australia’s iron ore price pain can’t get any worse. The income shock will be over because there is zero income. At the current rate of decline we’ll be there by July, which isn’t absurd given RIO will dump another big lump of new supply on the falling market in May. Bloomie seems to think we’ll get there too:

The iron-ore industry will face a “breaking point” if output continues to climb and prices are driven below $30 a metric ton, according to Bloomberg Intelligence.

That’s the level where many of the world’s biggest producers would be at or below cost and forced to shut mines, according to Kenneth Hoffman, an analyst at Bloomberg Intelligence in Skillman, New Jersey. It’s about 44 percent lower than current levels.

“Miners are saying they will ramp up production as much as possible to lower their overall unit costs, which will likely continue to force prices significantly lower until they reach a breaking point,” Hoffman said Friday in pa report.

Force mine closures by the majors? Not in the immediate future. But it sure will shut mines for everyone else.. From Sky:

Morningstar analyst Matthew Hodge says higher cost miners like Fortescue and Roy Hill will soon be ‘running to stand still’.

‘There has to be some rationalisation,’ Mr Hodge told AAP.

‘Someone needs to go broke, or some miners need to merge production because what’s happening at the moment is unsustainable.

‘Things are bad and there’s no real sign they’re going to get any better soon, unless there’s a bit more enthusiasm around forming a cartel.’

Fortescue has just finished a massive expansion program and Rio Tinto plans to expand by another 50 million tonnes while Roy Hill will begin ramping up to 55 million tonnes in September.

Not “someone”, everyone but the majors. Will the shut-ins be in China? From the FT:

About three-quarters of Chinese iron ore mines are in the red, according to remarks on Friday by Yang Jiasheng, chairman of the Metallurgical Mines Association of China.

While many smaller, private iron ore miners may be willing to sell or at least mothball production, state-owned mines are locked into contracts with mills and will keep digging.

Local governments also generally oppose closures that might raise local unemployment rolls.

State-owned metals trader Minmetals, for example, has been unable to get permission to close a costly mine in northern China, in spite of the availability of cheaper imported ore.

“Many of the iron ore mines have signed contracts with steel factories,” said Wang Min, analyst at Lange Steel Information Research Center in Beijing. “Many are still operating because they want to make sure they have stable supplies for steel factories.”

Shi Zhenglei, iron ore analyst at Mysteel, reckons that about half of China’s estimated 1,500 iron mines will be forced to close this year.

However, this will only remove 20 to 30 per cent of national capacity. Many Chinese mines produce low grades of ore.

Chinese production is currently around 33o million tonnes. Authorities will want to preserve a substantial local iron ore industry for strategic reasons so 250mtpa is the low for me, more likely over two years.

Let’s do the numbers then. Here are today’s expansion plans through 2017:

- current glut estimate 70 million tonnes per annum (mtpa)

- RIO: 60mtpa

- BHP: 40mtpa

- VALE: 90mtpa

- Roy Hill: 55mpta

- Minas Rio: 25mtpa

- Sino Iron 25mtpa

Steel production in China is also going to fall. Let’s be generous and say 6% over three years. That subtracts 80mtpa from seaborne iron ore demand, with some offset from developed markets let’s call it 50mtpa globally.

That means a total of 415mtpa grade-adjusted seaborne production must close to balance the market through 2017. By my reckoning the following closures are baked in over the next two years:

- Australian juniors 50mtpa

- global juniors 50mtpa

- China 80mtpa

That still leaves us nursing an extraordinary 235mtpa surplus in 2017. There is no way to balance the market without shutting-in major mining output and until then the surplus is so huge that all of the iron ore cost curve could remain in the red.

The rather obvious candidate for bankruptcy is the heavily indebted FMG. Sino and Anglo’s Minas Rio are higher cost but aren’t big enough to make a difference and have deep-pocketed parents. If FMG doesn’t die then iron ore will sink to unimaginable lows and the pain for everyone will be infinite.

The economic impacts for Australia once past the “all good threshold” are:

- an huge hit to Comrade Colin Barnett’s lunatic royalty forecasts;

- a much larger hit to the Federal budget which loses $300 million for every one dollar fall in the iron ore price. At $37, the Budget will have lost $7 billion per annum since the MYEFO in the forward estimates;

- with juniors going bust, Sino and Roy Hill moving to production and the major’s cost-cutting with a chainsaw, 10k jobs will be lost in the iron ore sector through 2017 and double that with multipliers, and

- the RIO and BHP share prices are going to crash at the “all good threshold”, hitting superannuation and broader household confidence.

The iron ore price agony will soon end, but iron ore industry and wider destruction is about to begin. This ensures more interest rate cuts are coming. Who knows the precise timing? They’ll just keep coming this year and next.

This and a falling dollar should be enough to prevent contagion in national housing markets for a little while, with the significant exception of Perth. South eastern cities may even blow off further.

But there is also a growing risk of a “tipping point”; an unforeseeable moment when the system lurches from one form of stasis to another. Australian households could look up and suddenly wonder whether we can prosper without iron ore. The trigger might be the ruined Budget, crisis engulfing FMG, crashes in big iron share prices or one rate cut too many. If it comes, greed will turn to fear and that will manifest in a sudden freeze in housing markets and spending nationally.

Even if households do ignore the cracks spreading through the base of national iron ore income, pushing harder into the soaring superstructure of housing leverage, in truth, it is only a matter of time now.

With the end of the global business cycle likely to arrive before the end of 2017, and with today’s iron ore price crash draining away Australia’s remaining fiscal and monetary firepower in advance, the next external shock will be an epochal event Downunder.

Hit the bid, peeps. Hit it hard.