It’s been some time since my last “five drivers” of value post for the Australian dollar. An update is timely given the extreme settings developing around the currency. The five drivers are:

- interest rate differentials;

- global and Australian growth (more recently this has become more nuanced for the Aussie to be more about Chinese growth);

- investor sentiment and technicals; and

- the US dollar

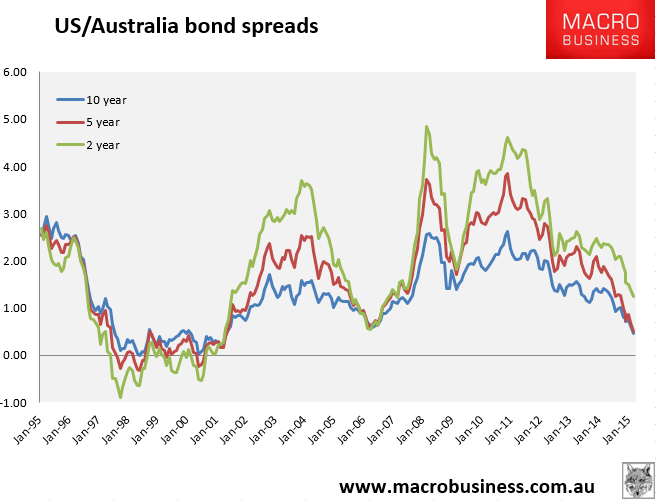

For the first, local interest rate hikes are going lower this year with falling terms of trade, the capex cliff and a soft labour market outweighing the bloom in activity in cyclical sectors. The bond market is pricing another one and half cuts and the spread to US bond yields has collapsed:

The primary target of RBA rate cuts is non-mining business investment. Whether via confidence, housing-led demand or a lower dollar, it will not stop cutting until it sees a lift in that key gauge. The April meeting is difficult to call but I suspect the bank will want to cut again having squibbed it in March. The only impediment is house prices but that will probably not stop it. Panic could make it wait until auction clearances settle.

On driver two – global, local and Chinese growth – the jury is in. Global growth will be luke warm this year but Chinese growth is going to slow moderately below 7%. Mini-stimulus and monetary easing has stabilised activity for the next three to six months but the ongoing housing shakeout will pressure growth all year. Everything points to an ongoing structural adjustment to slower and less commodity-intensive growth in which policy is deployed to maintain a manageable glide slope.

Australia’s terms of trade will remain under a lot of pressure. Iron ore has crashed to $58 and won’t rebound for long. We have only a few months before RIO unleashes a new wave of supply. Coal has been smashed too and the falls in the terms of trade are well into “external shock” proportions. The dollar has been falling in lock-step with iron ore for six months.

Australian growth will follow suit. All things equal, we can expect another year of firmly sub-par growth, perhaps under 2%%, as the capex cliff, falling terms of trade and weak national income outweigh the cyclical forces around house prices.

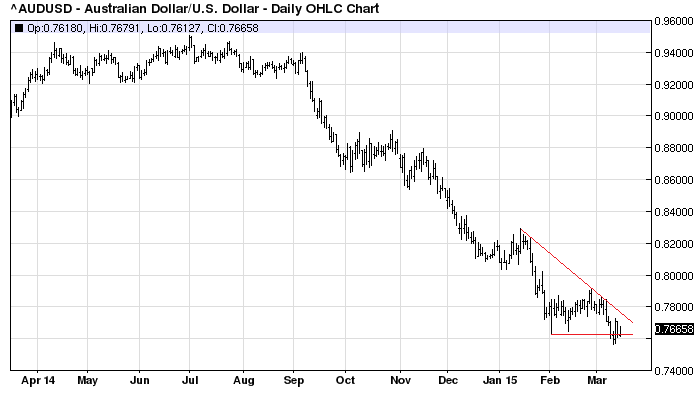

Drivers three and four look mixed. In technical terms, the Aussie has broken the base of its bearish triangle pattern but it has failed to follow through so far:

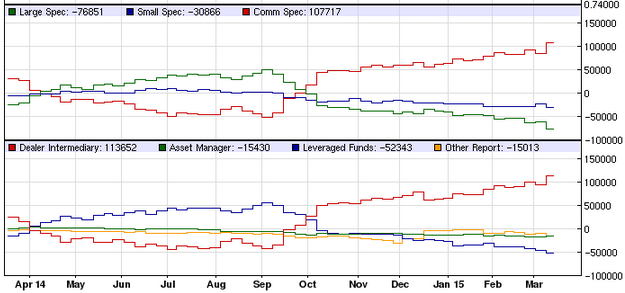

Perhaps the major reason why is that sentiment is so bearish that there aren’t enough sellers left. The Commitment of Traders report last week showed that the large and small speculators that control the market are the most short that they’ve been in recorded history:

That doesn’t mean that the market can’t get more short but these levels are extreme and have in the past signaled bottoms not tops.

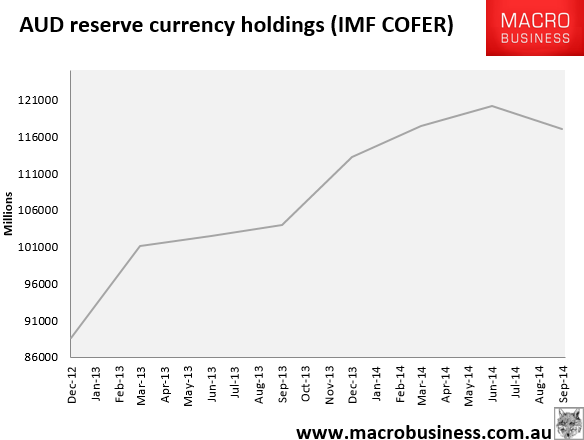

There is one other possible positive for sentiment. We know that central banks have been adding Aussie to there reserve portfolios for a few years. That has been a significant real support to higher valuations and general market sentiment around the currency. Unfortunately, the IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) report is six months behind but up until Q3 2014 it showed that as the Aussie regained its cyclical mojo and got cheaper, official buying slowed to a trickle:

I will be surprised if this slowing trend has changed much since.

The final driver, the valuation of the US dollar, has torn the roof off. As growth improves through the year and rate rise bets have been brought forward, and alternative currencies such as the euro and yen are being actively debased, the US dollar rally has approached ludicrous speed:

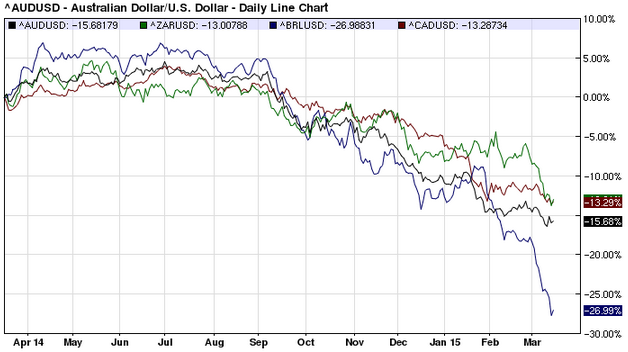

But the Aussie has actually held up well against this headwind in recent weeks and there is nothing to really separate it from any other commodity currencies:

As well, I’m less hawkish on US rate hikes than markets. The Fed clearly wants to normalise rates but it is best to assume caution in the Fed, especially when Q1 data has been universally weaker than expected (except for jobs) and the dollar is doing the tightening already. It is surely due for a period of consolidation.

The upshot is that the fundamental conditions for Australian dollar weakness remain strong. The weakening of the drivers is most apparent in the fundamentals of Chinese rebalancing and local slowing which will keep the RBA loosening. Potential US tightening is another strong downwards pressure.

However, it is also clear that markets have moved well ahead of policy in shifting positioning so a technical rally appears imminent. Given this contradiction, it’s probably better to be taking a medium term view of the Aussie right now, which still points materially south.