Today’s move came as no surprise following the particularly weak prints of January inflation, and another soft reading expected for February. Both CPI and PPI slipped to a 5-year low in January, to 0.8%y/y and -4.3%y/y respectively. Although the shifting timing of Chinese New Year was to blame, underlying sequential momentum of core inflation (e.g., seasonally and CNY adjusted 3-month growth) did sink to the slowest pace since global financial crisis. We expect February inflation to have not rebounded above 1% either, adding further deflationary concerns.

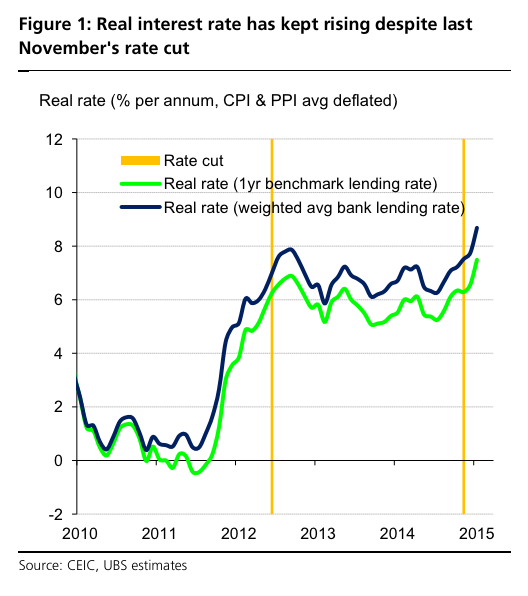

The decline in inflation has rapidly pushed up real interest rate. The average of CPI and PPI has dropped substantially by 170 bps since Q4 2014 and 250 bps during the past 6 months, while nominal interest rate has remained sticky despite the November rate cut, with average bank lending rate edging down only around 20 bps and our estimated overall financial cost barely moving. As a result, real rate has moved up by +100 bps since Q4 2014 according to our estimation (Figure 1). Rapid increase in real interest rate means a tightening of monetary conditions, which stands in sharp contrast with softening real activity growth. Moreover, financial burden on corporate sector has been aggravated. With industrial profit growth already mired in recession (total profit -6%y/y and principal business profit -9%y/y in Q4 2014), risks are quickly building up at financial system, prompting more monetary accommodation to mitigate massive tightening and contain financial risk.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.