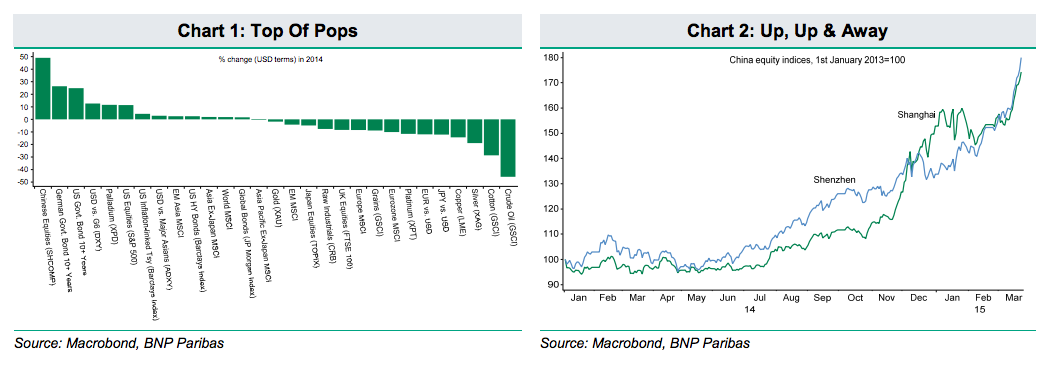

Against all odds, the best performing asset class on the planet over the last nine months or so has been Chinese equities. After languishing for the first seven months of 2014, Chinese stocks have since been on an incredible tear, ending 2014 up a remarkable 49% in USD terms, even outstripping the c.28% annual return posted by Bunds (Chart1). And the strong gains have continued so far in early 2015. Up almost 12% in USD year-to-date at time of writing, Chinese equities continue to sit atop the heap of global asset returns. All told, the Shanghai and Shenzhen markets have surged almost 80% in local currency terms since mid-2014 (Chart 2).

China’s policy makers have largely eschewed broad-based policy loosening although the tempo of monetary easing has quickened in the last few months as the economy has softened. The bottom line is however that the delta on credit growth has been consistently negative over the last year: a phenomenon that should herald lower, not higher, equity prices.

Nominal GDP growth i.e. the sum of the economy’s cashflows is ultimately the driver of profits and therefore long-run equity returns. Continued nominal compression as real growth slows and pricing power wilts under the weight of excess capacity in key sectors also offers little fundamental support for higher equity prices. Nominal GDP growth slowed to 7.7% y/y in the final three months of 2014; the slowest top-line growth since 2009H1. Slowing cashflow growth is inevitably crimping profits growth with a lag. Implied earnings growth of the Shanghai and Shenzhen exchanges is only c.5-6% and likely to slow further. Official data on industrial profits, down -8% y/y in December, has also been unusually weak, underlining that earnings growth is not the driver of recent gains.

Far from a surge in external liquidity [from the from the long-delayed introduction of the Hong Kong/Shanghai ‘stock connect’ last November for example], an increasingly self-feeding domestic frenzy fuelled by leverage appears to be the key driver. Initially, and seemingly deliberately, nudged by state media exhortations over the summer that stocks were cheap and doubtless further pushed by the housing market downturn, retail investors appear to have poured into the stock market with an unprecedented surge in margin debt powering purchases. Combined margin purchases on the Shanghai and Shenzhen exchanges have soared to over RMB200bn per day in the last week or so, leaving daily purchases almost 2x the total value of northbound purchases generated by Stock Connect. Margin purchases have been running well ahead of redemptions ensuring that the outstanding stock of margin debt has ballooned by over RMB1 trillion since August; equivalent to more than 1% of GDP.

Margin purchases are now accounting for almost 20% of equities daily turnover which itself has soared to wholly unprecedented levels in another sign of self-feeding speculative frenzy.

Advertisement

As with the economy’s wider imbalances, the emerging stock market bubble poses an increasingly intractable policy dilemma for the authorities. Soaring equities are not only buoying consumer confidence even as house prices slide but are also playing a key role in providing a partial offset to the aggressive tightening of financial conditions imparted by the CNY’s rapid real appreciation since last July and still rising real borrowing costs as deflation intensifies. By definition, the stock market bubble cannot keep inflating but the authorities’ increasingly cannot afford to let it burst.

It looks like a deliberate ploy by authorities to enable deleveraging in listed firms. It must remembered however that the market is small so will have commensurate macro impact. At current prices its market cap is around $2.5-3 trillion. The US stock market is above $20 trillion.

That’s why the 2008/9 bust was largely irrelevant to growth.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.