From Morgan Stanley’s China deleveraging scorecard:

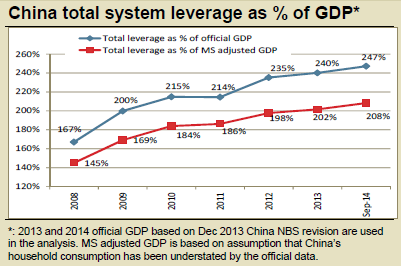

Total leverage to official GDP has risen to 247% at Sept 2014, still rising but at a slower pace than in the 2008- 2011 time frame. Our score of progress on 10 dimensions of successful deleveraging drops back to 48 from 51 out of 100, erasing the improvement made in our last review. China’s deleveraging looks set to stay a long and bumpy ride.…However, we maintain OW on MSCI China over EM equities as it trades at a 13% forward P/E discount to EM, where in many cases the growth models are facing more critical challenges.

On credit, our change in score favors investment grade over high yield, and banks over non-financial corporates. First, the old-economy sectors challenged by overcapacity, sluggish earnings and highly leveraged balance sheets – steel, cement, mining – dominate the high yield universe in China. Second, elevated real rates increase refinancing risks for high yield corporates, which have been free cash flow negative historically.

Yep, although I’d be cautious on banks!