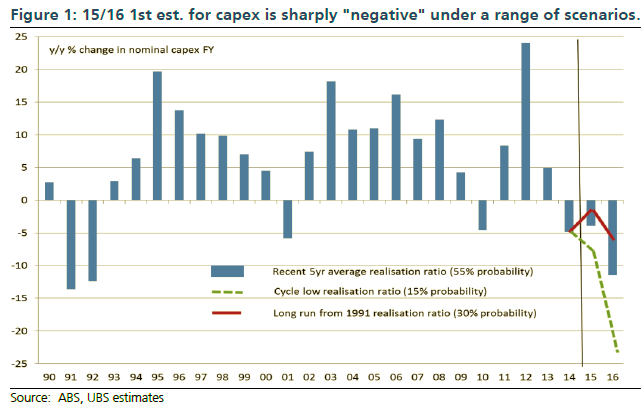

UBS has done some nice scenario analysis of Australia’s capex cliff and it is sobering stuff:

The 2015/16 capex outlook is bleak. Unless investment intentions improve sharply, total (nominal) business capex next year threatens to fall for the third consecutive year – the first time on record in at least 50 years. More worryingly, current plans suggest capex could subtract more than 1½pts off 2015/16 real GDP growth.

The standout in the recent 1st estimate of businesses’ 2015/16 capex plans was not the further 20% fall in mining – being much as expected – but rather the sharp drop in non-mining intentions to -9% y/y, which reversed steady improvement through 2014/15 to reach +9% y/y. Surprisingly, after that release, the RBA’s March meeting press statement made no mention of what was a clearly worse-than-expected result.

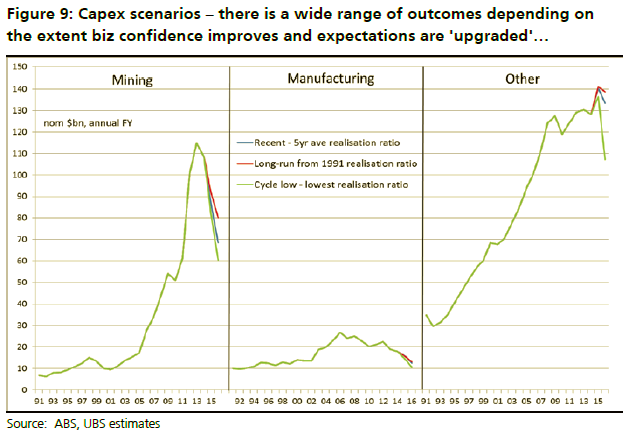

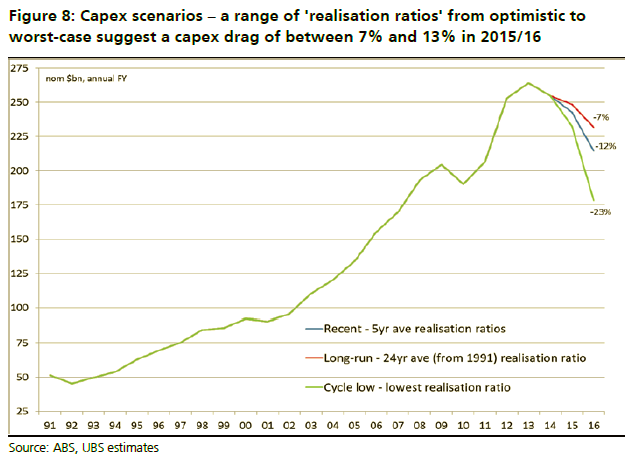

We show in this research note that under any of our scenarios, from a relatively optimistic one (using 24-year average realisation ratios), a central scenario (5-year average realisation ratios, UBS central case), or an unlikely worst case scenario (a cycle low realisation ratio), current capex plans suggest a deepening drag on growth from capex into 2015/16, ranging from -7% to -23% y/y.

This analysis clearly casts doubt on ours (& the RBA’s) forecast for a return to near-trend growth in 2016. Of course, business capex plans can change for the positive. But there is little to justify the idea that the weakness in the 1st estimate of 2015/16 is ‘something to watch’ rather than our view that it should be a ‘signal to act’ (whether that be via an additional rate cut or other growth enhancing reforms).

Doubt indeed. Where is the change to positive going to come from? Politics? Meh. Rate cut? Only for house prices not investment. International. With China slowing and commodities crashing?

The sharemarket is the one possible positive but it’s not going to be able to overcome the others. I’ll go with the five year average with downside risks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.