While both agencies shrugged off remarks last week by Prime Minister Tony Abbott that debt equal to 60 per cent of the economy would be “a pretty good result” by world standards, they highlighted the nation’s reliance on foreign creditors.

Moody’s senior vice president Atsi Sheth said that such a level of debt – which the government has vowed to avoid and would only occur near-term if there was an economic disaster – could lead to a sharp shift in attitude among offshore investors.

Fitch’s senior Asian sovereign analyst Andrew Colquhoun echoed the point…”One could argue Australia’s debt tolerance is weaker than that of the larger advanced economies, including the relatively high importance of commodities for Australia, implying a lower debt ratio than 80 per cent might become an issue for an AAA rating.”

Fitch repeated S&P’s recent outlook that for two years there’ll be no change.

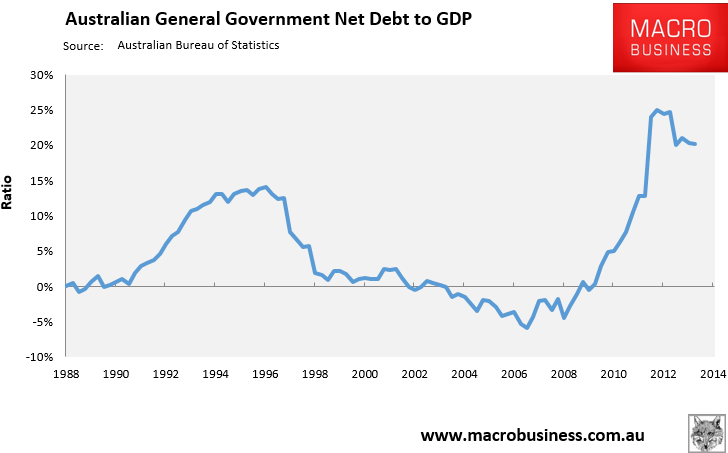

The issue is being distorted through the prism of the IG report though the agencies appear to be onto that. The long term is largely irrelevant. What matters is the next shock and whether Australia has the fiscal firepower in reserve to stimulate and/or guarantee the banks. Here, again, is the net debt ratio to GDP:

S&P has a hard cap of 30% for the AAA so it’s as good as gone. The other agencies (which are less important) see a little more leeway. But note, if we were to repeat the GFC experience in which Australia had no recession, we would see net debt rise to 50% of GDP or more in under three years. The above Moody’s and Fitch numbers are gross debt ratios which is much higher than the chart so a GFC rerun implies losing the AAA swiftly from them as well. But all will see the trajectory long before that so I’d guess the downgrades begin within one year of the shock. With monetary policy approaching exhaustion, it is the stuff of an historic and sustained external shock.

The Abbottalyse sell out on this is a AAA betrayal of Howard/Costello economic growth model, it’s a AAA betrayal of those that would see that model reformed at a manageable pace, it’s a AAA betrayal of everything that the Liberal Party stands for.