From Westpac comes the bible of consumer attitudes today and it settles some of the more fanciful notions abroad last week about what lifted consumers.

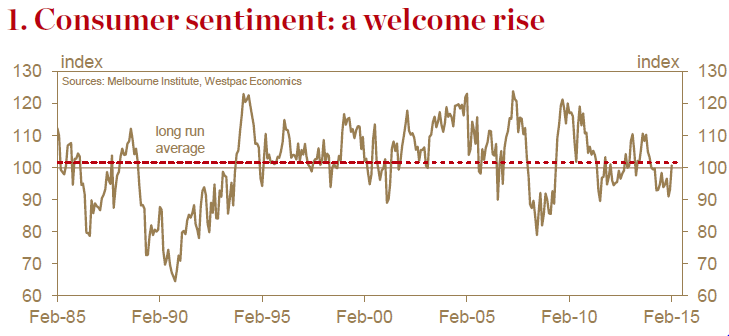

― The Westpac–Melbourne Institute Index of Consumer Sentiment jumped 8% in Feb from 93.2 in Jan to 100.7. This is the first month since Feb 2014 that optimists have outnumbered pessimists, albeit only just.

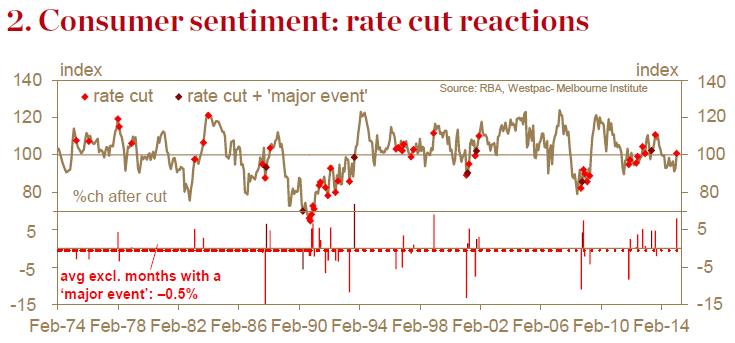

― A surprise 25bp interest rate cut from the RBA, sharply lower petrol prices and surging equity markets helped drive the surprisingly strong gain, more than offsetting a drag from political concerns. These themes showed through strongly in the survey detail.

― Additional questions on mortgage rate expectations show a big shift since Aug with only 40% expecting interest rates to rise over the next 12mths compared to a clear outright majority (63%) back in Aug. This in turn suggests the RBA’s rate cut move gave an added boost to sentiment via its impact on expectations.

― CSI± measure, our modifi ed sentiment indicator that we favour as a guide to actual spending, posted a milder 4.9% rise in Feb but this followed a somewhat stronger 3.6% gain in Jan. Overall, CSI± has recovered from the sharp fall in late 2014 suggesting any associated hit to actual spending is likely to have been brief. CSI± is still only pointing to flat per capita spending, implying total consumption growth around 1.5%yr, a weak pace by historical standards.

.

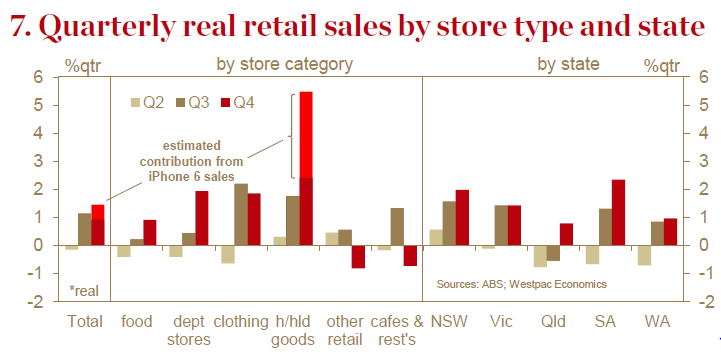

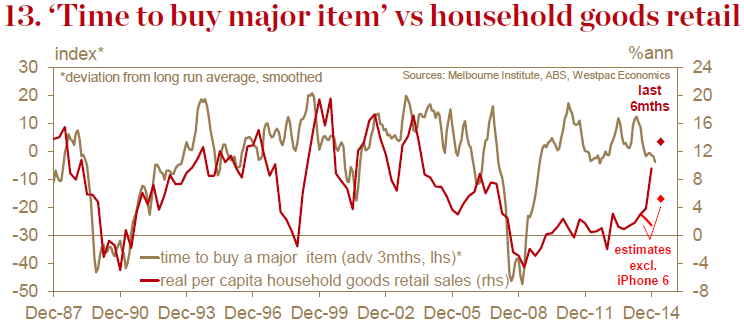

― Latest partial data and business surveys are painting a more upbeat picture on spending although the impact of the iPhone 6 launch means recent strong gains in retail sales should be treated with caution.

― The sub-index on ‘time to buy a major item’ rose just 0.5% in Feb but posted a much stronger 13.6% bounce in Jan to be back at its Nov levels after a disconcertingly sharp drop in Dec.

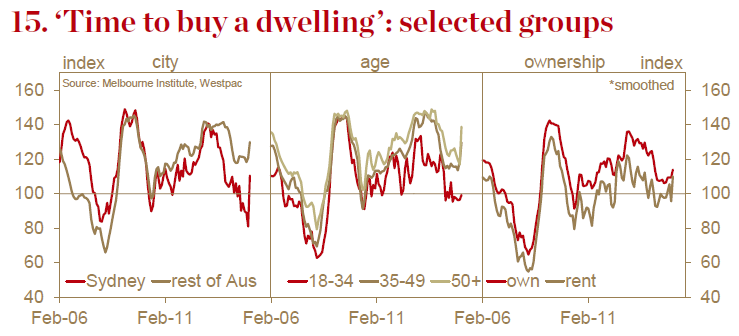

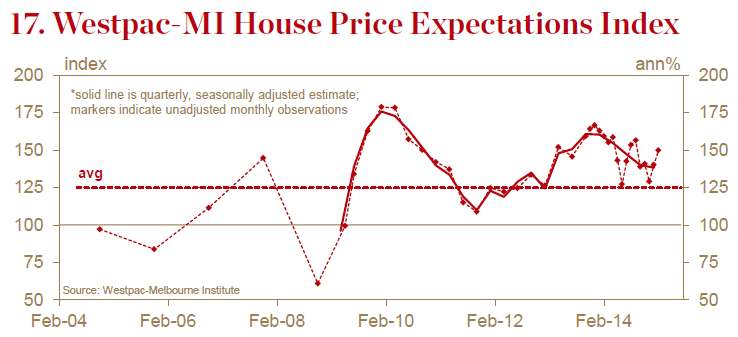

― The RBA’s rate cut gave a strong boost to confidence in the housing market. The index tracking views on ‘time to buy a dwelling’ jumped 9.7% to reach its highest level since February 2014. Similarly, the Westpac Melbourne Institute House Price Expectations Index jumped 6.9% to reach its highest level since September 2014.

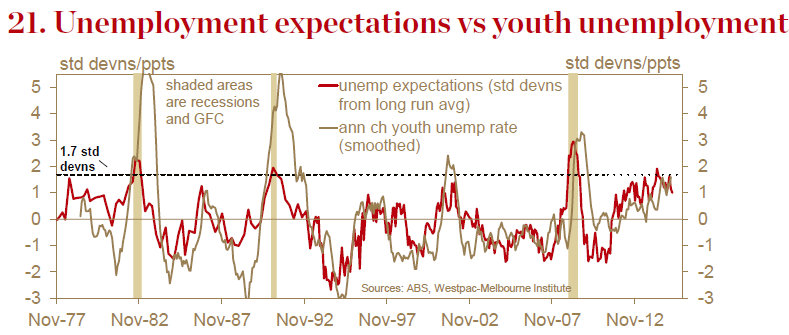

― Job loss fears remain the main weak spot for consumer confi dence. The Westpac Melbourne Institute Unemployment Expectations Index declined 1.5% in Feb following a 5.5% fall in Jan (recall that a lower level indicates fewer consumers expect unemployment to rise over the next 12 months). While that marks a signifi cant improvement, the Feb decline was disappointing given the surge in confi dence overall. At 147.8 the Index remains in deeply pessimistic territory.

The MB take? I went into this document looking for signs of some weakening of consumers conservatism, given the good headline bounce and the associated run in mortgage credit already apparent in December when rate expectations shifted. I couldn’t find it.

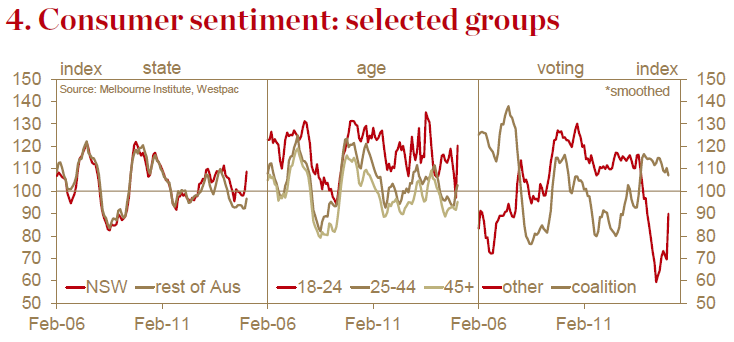

The shopping measures dislocated from purchases some time ago and remain so. The rate cut clearly lifted housing sentiment for the aged and adipose but nobody else. Unemployment expectations remain locked in uptrend with a hint of divergence in Sydney.

I remain on alert, however, because the yield-juiced stock market is off and running and this is a new factor for households. Could double-bubbles in housing and stocks reinforce the illusion of wealth enough to trigger spending where only one bubble has failed? It’s a question worth asking but is too early to answer.

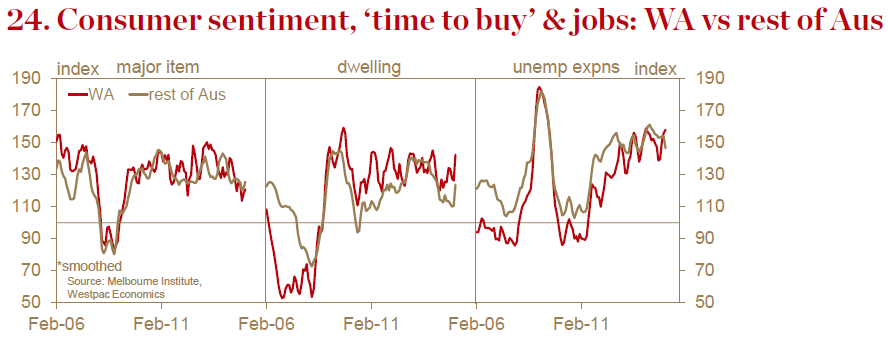

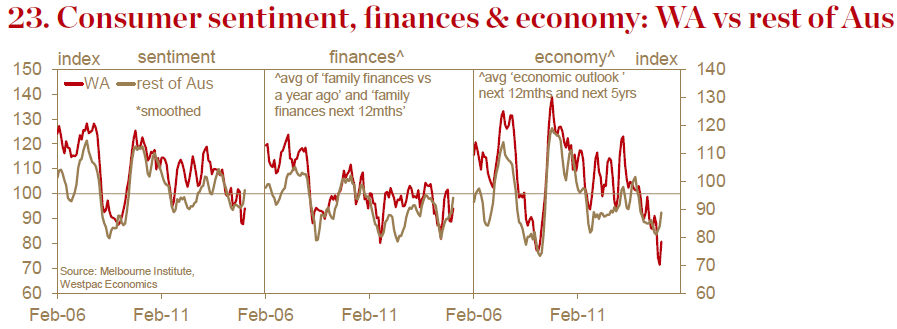

One final point of note. The survey contained some nice breakout material on WA:

Versus the nation, WA benchmarks are perhaps surprisingly correlated. Economic outlook is the only clear divergence and only in degree not kind. It rather raises the question: can the nation diverge from its mining powerhouse as it sinks over the next eighteen months? Full report.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

.