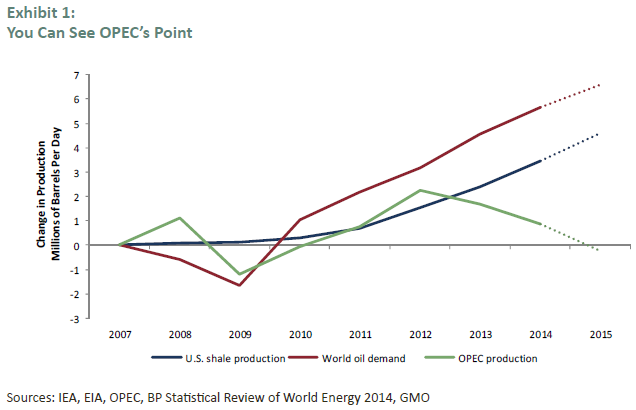

The simplest argument for the oil price decline is for once correct. A wave of new U.S. fracking oil could be seen to be overtaking the modestly growing global oil demand.

It became clear that OPEC, mainly Saudi Arabia, must cut back production if the price were to stay around $100 a barrel, which many, including me, believe is necessary to justify continued heavy spending to find traditional oil.

The Saudis declined to pull back their production and the oil market entered into glut mode, in which storage is full and production continues above demand.

Under glut conditions, oil (and natural gas) is uniquely sensitive to declines toward marginal cost (ignoring sunk costs), which can approach a few dollars a barrel – the cost of just pumping the oil.

Oil demand is notoriously insensitive to price in the short term but cumulatively and substantially sensitive as a few years pass.

The Saudis are obviously expecting that these low prices will turn off U.S. fracking, and I’m sure they are right. Almost no new drilling programs will be initiated at current prices except by the financially desperate and the irrationally impatient, and in three years over 80% of all production from current wells will be gone!

Thus, in a few months (six to nine?) I believe oil supply is likely to drop to a new equilibrium, probably in the $30 to $50 per barrel range.

For the following few years, U.S. fracking costs will determine the global oil balance. At each level, as prices rise more, fracking production will gear up. U.S. fracking is unique in oil industry history in the speed with which it can turn on and off.

In five to eight years, depending on global GDP growth and how quickly prices recover, U.S. fracking production will start to peak out and the full cost of an incremental barrel of traditional oil will become, once again, the main input into price. This is believed to be about $80 today and rising. In five to eight years it is likely to be $100 to $150 in my opinion.

U.S. fracking reserves that are available up to $120 a barrel are probably only equal to about one year of current global demand. This is absolutely not another Saudi Arabia.

Saudi Arabia has probably made the wrong decision for two reasons:

First, unintended consequences: a price decline of this magnitude has generated a real increase in global risk. For example, an oil producing country under extreme financial pressure may make some rash move. Oil company bankruptcy might also destabilize the financial world. Perversely, the Saudis particularly value stability.

Second, the Saudis could probably have absorbed all U.S. fracking increases in output (from today’s four million barrels a day to seven or eight) and never have been worse off than producing half of their current production for twice the current price … not a bad deal.

Only if U.S. fracking reserves are cheaper to produce and much larger than generally thought would the Saudis be right. It is a possibility, but I believe it is not probable.

The arguments that this is a demand-driven bust do not seem to tally with the data, although longer term the lack of cheap oil will be a real threat if we have not pushed ahead with renewables.

Most likely though, beyond 10 years electric cars and alternative energy will begin to eat into potential oil demand, threatening longer-term oil prices.

Exactly right, though in my view the equilibrium price will be more like $50 than $30 for the next half decade.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.