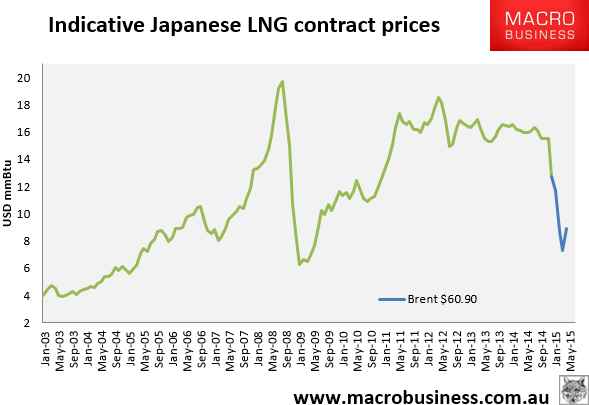

The Brent oil price fell back 1% last night after yesterday’s thin excuse for a rally to $60.90. News was thin. The indicative LNG price contract fell to $8.86mmBtu:

In news, the approaching glut is throwing up forecasts of falling volumes for projects:

NYC-based PIRA Energy Group believes that strategies are emerging for keeping LNG trains operating amid weak seasonal demand.