Via The Australian, UBS reckons not much higher:

Australian shares may be close to a peak after running well ahead of any improvement in earnings expectations after a “decent” earnings season so far, according to UBS.

“Results have been mixed but on average in line with expectations,” UBS equity strategists David Cassidy and Dean Dusanic say.

They retain their 5700 year-end target for the S&P/ASX 200.

“Overall earnings are set to be flat in FY15, although EPS growth in the market ex-resources is still on track for a robust 9%, helped by the fall in the A$ and ongoing cost out initiatives,” the strategists say.

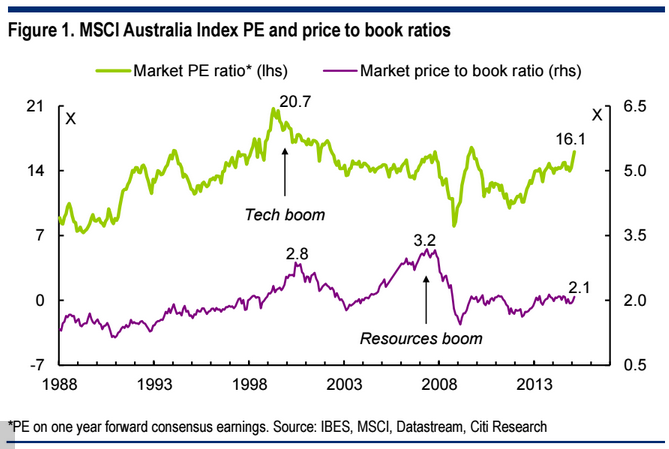

“Nevertheless with the market up 9% year to date, prices are outstripping earnings (and) P/E multiples are continuing to move higher.

While the recent interest rate cut in Australia and the prospect of even lower official interest rates is helping the relative case for stocks, particularly the high yielders and the heavily retail-investor-owned bank sector, the share market will need stable US bond yields and a further rebound in commodities to make decent gains from here, the strategists say.

The recent rally has been entirely about the last point on yields. It began in December when it became clear that rate cuts were coming and the more cuts we get the higher it will go, earnings or not, chart from Citi:

Earnings growth is going to be lousy as commodities keep falling but until the income shock tips over into the banks, which is probably another year away, stocks can march ever higher. The IMF even has new term for it, “rational bubble-riding“:

By process of deduction, this paper seeks to offer an explanation for why asset bubbles have posed—and will likely continue to do so—a threat to economic stability despite financial markets being characterized by more complete information, a greater array of securities through which to express views, and a more pronounced impact of sophisticated institutional investors, than ever before. The arguments advanced here suggest other candidate explanations for the persistence of bubbles, such as limits to learning, frictional limits to arbitrage, and behavioral errors, are unsatisfactory (by themselves at least) as they are inconsistent with the aforementioned trends sweeping across global capital markets. By contrast, investment manager incentives, the nature of the principal-agent relationship, and the growing presence of institutional investors, are all entirely consistent with the persistence of financial bubbles. Importantly, this explanation does not require a baseline assumption of widespread irrationality in the conventional sense. Simply put, it can be entirely rational—from the perspective of business and compensation risk—for asset managers to knowingly ride bubbles because of benchmarking and the short-term performance appraisal periods often imposed on asset managers by asset owners.

To the extent that this diagnosis is close to the mark, it has potentially important policy implications.

First, it suggests that bubble episodes will be at least as frequent as in the past, and quite possibly more so, as institutional assets under management continue to increase in both absolute and relative terms (particularly in the emerging markets).

Second, it suggests remedial policies need to be multifaceted in nature. While countercyclical monetary and macroprudential policy may be best placed to lean against conventional leverage-driven asset booms (notably in real estate markets), they are not particularly well suited to dealing with the challenges posed by the rapidly growing asset management industry. Contemporary discussions of financial instability are heavily conditioned by the build up of leverage that culminated in the 2008 crisis, and understandably, measures aimed at avoiding a similar scenario in the future have been front and center in subsequent policy initiatives. However, subdued leverage is not a sufficient condition for financial stability—if systemic risk, and activity in the wider economy, is shaped importantly by large shifts in risk premia owing to the ‘rational herding’ motivations of asset managers (even in the absence of leverage), then this traditional focus may be too narrow (Feroli and others, 2014; Stein, 2014; Haldane, 2014). Moreover, as risk-taking migrates out of the formal banking sector, policy makers must guard against the risk of ‘fighting the last war.’ Put differently, while they will always comprise a key component of the policy making toolkit, there are likely to be limits to what countercyclical policies can achieve alone. Time-invariant policies related to the design of principal-agent contracts and financial benchmarks—addressing the cause, not simply the symptoms, of institutional behavior—have a key role to play in mitigating the impact of institutional frictions on financial stability.

More broadly, while the behavior and failure of banks has been studied for centuries, similar analysis of the institutional asset management industry is, by contrast, a greenfield site—yet the risks and opportunities presented by asset management could be every bit as important (Haldane, 2014). Whether it be asset management industry characteristics (along the dimensions of size, concentration, and interconnectivity), or asset management activities (duration mismatches, securities lending, fire sales and herding), there are a variety of channels by which the industry could pose a threat to financial stability.Care will need to be taken in distinguishing the degree to which asset managers passively transmit risk (in passing through the decisions of asset owners) as distinct from originating new sources of risk themselves. Nonetheless, if present indications are any guide, these will serve as fertile grounds for future research aimed at safeguarding the international financial system.

I began the year thinking the ASX would fall by December as mining profits kept tumbling. I still think the latter is true but in the meantime we could rationally bubble ride to the moon!