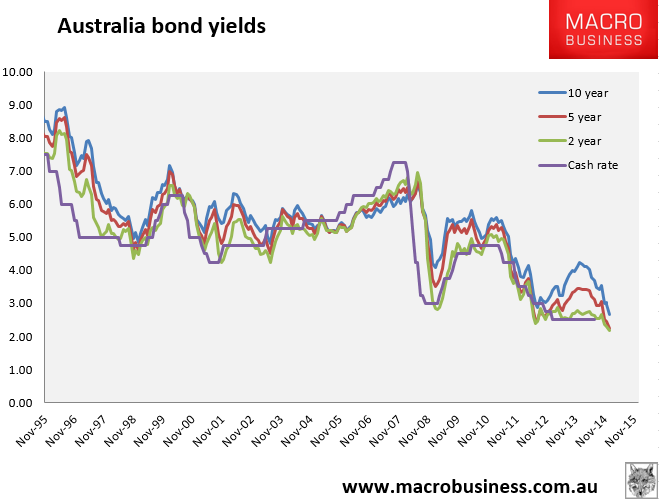

Australian bonds have been moving very sharply in recent times buffeted by lackluster domestic growth and externally by falling commodity prices. We’ve seen record low yields across the curve:

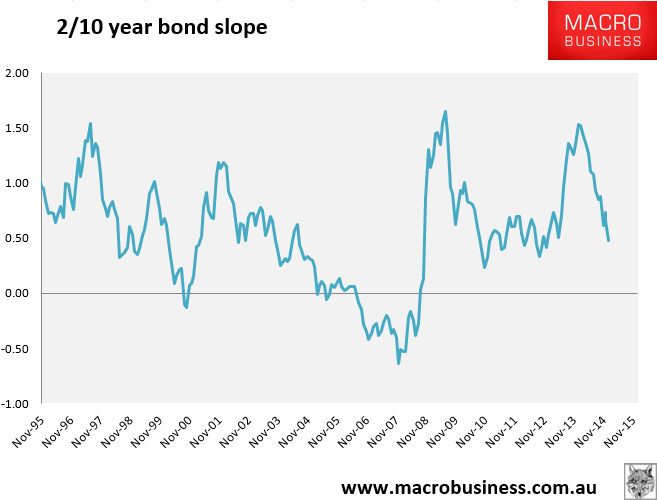

The two year has priced one and a half rate cuts. Just as interesting, the yield curve has been “flattening”, jargon for when short and long terms yields begin to converge:

Advertisement

The current slope between the 2 and 10 year isn’t remarkable at 48bps, though the trend is sharply down, and last week it reached a low of 37bps before rebounding on oil. But it’s an interesting question what it would take for the curve to invert, which is classically regarded as a signal of approaching recession.