Regular readers will know that the Australian economy is not a miracle but a strange and rather unique blend of pre-modern and post-modern business sectors. The pre-modern are the commodity producers. They totally dominate Australian exports and account for a huge proportion of national income. The post-modern is the banking sector and its trick of leveraging up that income in big offshore loans that are re-distributed largely through mortgages to households.

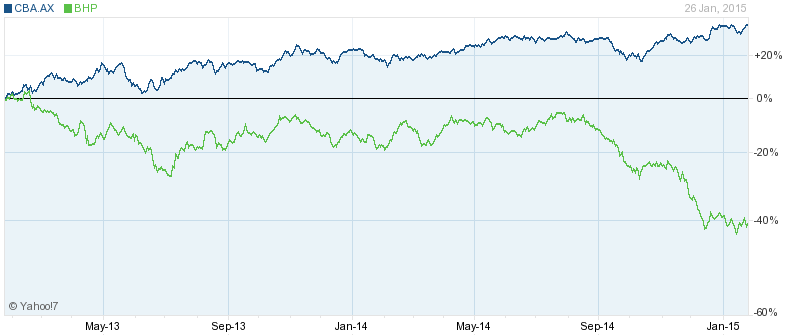

One half of the economy can’t function without the other for very long, which makes me wonder at the sustainability of certain current equity market trends. CBA has hit a record high today while the mining sector is being bashed again. Here’s the divergence in CBA vs BHP since 2011:

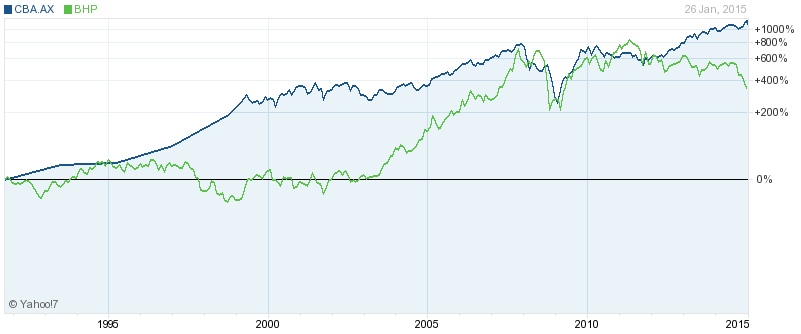

Over the long term, this has happened once before in the late nineties:

The gap is bridged by low interest rates, which fire up the bank’s leveraging process when miners fall. Last time around when the peak was reached in the levergaing, BHP surged to make up the gap as China took off.

This time BHP has no such hope and with house prices and household debt coming off a higher base and interest rates getting close to Australia’s version of the zero bound, the CBA economy doesn’t have as much petrol in the tank, either.

At some point these two stocks are going to converge once more and if BHP can’t rise then CBA…