The quarterly NAB property survey is a canvassing of real estate professionals and they appear to be losing confidence in the house price cycle.

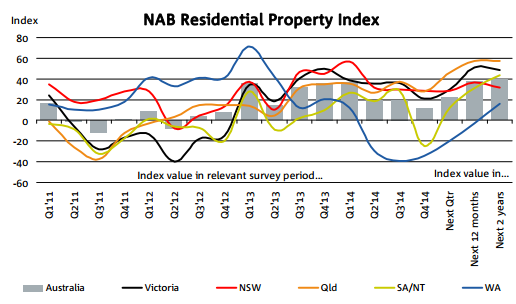

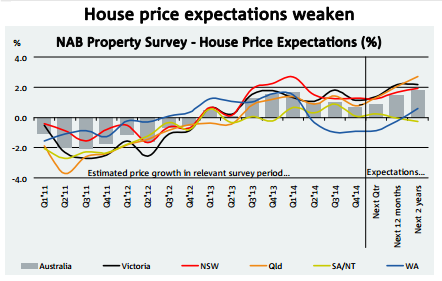

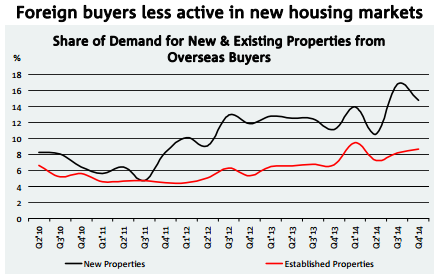

NAB Residential Property Index falls as house price expectations pared back and rents weaken. Sentiment softer in all states (and still deeply negative in WA). Almost 10% of all property is being purchased by first home buyers as an “investment”. Foreign buyers less active all states except VIC (now 1 in 3 of all new property sales). Over half of all foreign transactions are apartments, one-third houses and the balance re-development. Around 70% of all foreign purchases are properties valued less than $1mn; 5% in excess of $5mn.

Survey highlights:

NAB Residential Property Index fell to +12 points in Q4 (+19 in Q3). NSW overtook QLD as strongest state; sentiment notably lower in SA/NT and still deeply negative in WA. QLD and VIC most optimistic looking forward and WA weakest by some margin.

Outlook for house prices over next 1-2 years pared back in all states (NAB also expects price growth to slow). Expectations for rents unchanged, with mildly stronger expectations in VIC and QLD masking softer outlooks in NSW and SA/NT.

Foreign buyers in new property markets less active in all states, except VIC where they accounted for 32.5% (or 1 in 3) of all sales – a new high. Around 17% of FHBs in the new property market were for owner occupation and 8% for investment.

Around 53% of foreign purchases were for apartments, 31% for houses and 16% for re-development. By price point, 40% of purchases were between $500k to <$1mn and 29% less than $500k. Around 5% were for premium property (+$5mn).

Housing affordability, construction costs and a lack of development sites seen as the biggest constraints in new housing market, while employment security and price levels the biggest impediment to buying established property.

Established property dominated by owner occupiers (42.6%). Local investors account for 22% of total demand, with FHBs(owner occupier) 16.1% with FHBs (investor) 9.3%. Foreign buyers more active (8.7%), led by NSW (11.3%) and VIC (12.8%).

Prospects for capital growth over the next 12 months were pared back at all price ranges in both the established housingand apartment markets in Q4, except for apartments valued between $1-2mn.

In short, fading price hopes, fear developing in WA, QLD hopes lifting, foreign buyers building out the Melbourne ghost city and increasingly influential in existing property. Not much new but firm confirmation. Full report here.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.