Sense from Credit Agricole this morning:

Overnight the main focus was on Chinese growth data. At 7.3% (cons. 7.2% YoY, prev. 7.3% YoY), Q4 GDP was released above expectations. However impact on sentiment was limited, with the IMF announcing a cut in its 2015 global growth forecasts to 3.5% from 3.8%. In an environment of sliding global growth expectations there is little room of stabilizing commodity price developments, what remains key to currencies such as the AUD.

Given this growth outlook, one cannot exclude further easing from central banks of economies with high commodity price exposure. In particular the risk of RBA turning more dovish, regardless of the recent better than expected labour data, remains intact. As such we are still of the view that the AUD is facing additional downside risk – in particular against the USD.

Add some more right-thinking from Societe Generale:

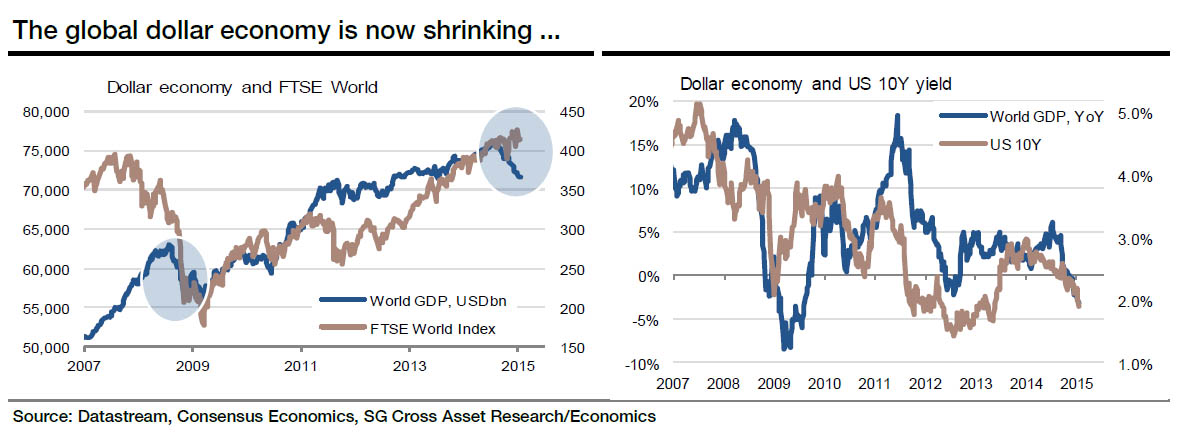

As the ECB prepares to race faster in a bid to export deflation, the risk is that the dollar economy (world GDP measured in US dollars) will shrink further. The dollar economy is down by just over 5% since July, marking a loss of just over $4tn in nominal terms. The last sharp contraction of the dollar economy took place in 2008. Back then the economy shrank by just over $7tn, marking a loss in excess of 10%. The foreign trade mix of the US fairly closely mirrors the composition of world GDP. As such, if the trade weighted dollar is appreciating, then this exerts downward pressure on the dollar economy on a near one-to-one basis. Any offset then comes from nominal GDP growth in local currency terms. Since July, the trade weighted dollar has gained just over 10%.Viewing the global economy from the vantage point of the dollar economy, it is hardly surprising that when the trade weighted dollar appreciates, commodity demand is eroded as economies with depreciating currencies lose purchasing power. To the extent that central banks actively seek currency depreciation, this could see further shrinkage of the dollar economy and add further downward pressure to commodity prices. Analysis by the IMF (WEO, April 2008), suggest that, as a rule of thumb, a 1% appreciation in the trade weighted dollar yields a 0.89% decline in the oil price after 1 month and 1.13% after 12 months.

There also seems to be a link between the size of the dollar economy and long bond yields. Again, this link has a sound economic rational. As major central banks ease monetary policy relative to the US, this not only lowers interest rates in the country in question, but also eases (ceteris paribus) pressure on the Fed to tighten. To the extent that foreign investors expect further dollar appreciation, this also triggers capital flows that exert further downward pressure on US interest rates. A shrinking dollar economy is also a headwind for corporate earnings.

The irony it seems is that as a growing number of central banks actively seek to export deflation, this could further exacerbate the market phenomena that have investors on edge. In a nutshell, if central bank accommodation and lower commodity prices fail to sufficiently boost GDP and inflation elsewhere in the world, the dollar economy is likely to shrink further. From a fundamental point of view, this is a clearly down side risk.

{kind=link}