There’s lot’s of cynicism around APRA’s new macroprudential regime, for good reason in some ways: it’s late, it’s weak and it’s opaque. But a clear view of this still suggests the conclusion that it will work to slow investment property lending and house prices. There are three reasons why.

The first is tackled by Jonathon Mott of UBS:

Strong growth in lending to property investors – APRA is concerned about growth in investment property portfolios materially above a 10% threshold. This will be an important risk indicator for APRA in considering if additional action is required.

We see this having significant implications for the banking system. The 10% threshold has been selected after discussions with the Council of Financial Regulators which took into account a range of factors including income growth and recent trends in the housing sector. It is not a hard limit but is a key risk indicator for more intense supervisory action. Such supervisory action may include increased reporting obligations, mandated reviews by external parties and higher capital requirements.

This focus by APRA is very important, in our view, as system investment property lending is currently growing at 9.9% year on year and is continuing to accelerate.

Over the last 3 months system investment property lending growth has grown at 10.9% annualised. As a result any bank which is winning or even maintaining market share risks breaching APRA’s guidelines.

Although bank Boards and Management have been asked several times by APRA not to loosen underwriting standards, we believe they are likely to heed formal announcement and act to actively slow Investment Property credit growth.

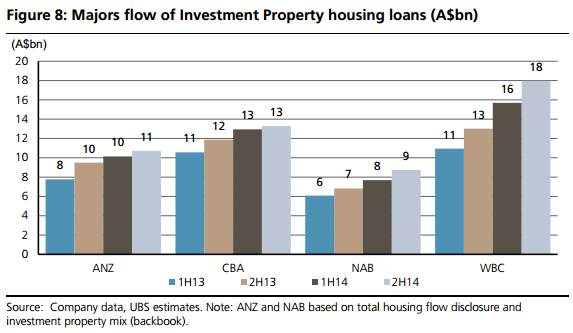

APRA data suggests Major banks have grown the flow of lending to Investment property by 25.2% in the last 12 months

Westpac has shown the strongest growth in flow, +40.5% y/y CBA has grown flow the slowest of Major peers, +17% y/y

However, it must be noted that growth in Investment Property credit (and all credit) is an output which is outside the direct control of the banks. While banks can manage loan approvals and funding flows, other mortgage flows such as mortgage redraws (which are often part of a contractual facility), property sales, external refinancing and property paydowns are largely outside their control.

Although data specifically on Investment Property mortgage flows is not readily available (only total housing credit is) from APRA and bank data we estimate that banks will need to reduce new Investment Property approvals (funding flows) by around 10% to reduce credit growth by 2%.

Such action is unlikely to have a material impact on bank earnings as we estimate a 2% reduction in investment property lending would only slow total credit growth down by ~40bp. This would reduce EPS ~50bp, all else equal.

However, by reducing investment property funding availability by 10% this is likely to have a cooling effect on some of the hottest parts of the housing market which we believe is sound ‘macro prudence’.

So, point one is the rate of change in investment property loans is about to slow materially. Investor loan stock has been growing at APRAs 10% but the flow is much faster and accelerating. That’s about to end with a big thump.

It is also fair to assume that the boom in interest only lending will stall, given a large part of that growth will be driven by investor loan growth.

Advertisement

Point two is that the one outstanding major bank that will be most affected by the rule change is not mentioned here. In the September quarter, Macquarie Bank’s total loan book was roughly $20 billion but it was growing at almost 40% per annum. It’s investment loan book was growing at nearly 50% per annum. These are not large figures in the scheme of things but given Mac Bank’s use of brokers (which have historically been less rigorous in underwriting standards) and its relationship with Yellow Brick Road, it’s reasonable to conclude that it has been funding a larger portion of the marginal buyers in the market. If there is one bank in the cross-hairs of APRA’s 10% threshold it is Mac Bank, with its 50% growth.

The third reason to expect macroprudential to slow the property market is that the Murray Inquiry will reduce credit flow a little generally and the Foreign Buyer Inquiry will also slow the foreign marginal buyer in the market.

In short, given much of the price gains have been driven by a very narrow set of cashed up foreigners and mad investors, these subtle moves could actually have an over-sized impact. That’s another reason to expect rate cuts, which will obviously support prices in some measure.

Advertisement

Gauging the impact of these changes is not easy. There’ll be time delays and further policy argy bargy. But throw in the relentless fall towards the zero bound (or our equivalent) in Australia’s monetary policy price deck, the huge headwinds turning to gale-force in the mining and manufacturing busts, the fading prospects for fiscal stability and the AAA rating, and the global cycle looking more ominous by the day, and it’s really a bit of a no-brainer.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.