From Goldman’s Tim Toohey, fast becoming a national treasure:

Relative to the commencement of 2013 and 2014, the main challenges and opportunities for the Australian economy seem better understood by the consensus and by policy makers. The triple threat of an income shock via commodity prices, an investment shock via the mining sector and a fiscal shock via federal and state governments are the threats that present as the key domestic risks for 2015. Although we have consistently highlighted these same themes over the past 2 years it is important to note that the challenges from these 3 themes remain mainly ahead of Australia rather than behind it. In terms of sequencing of the shocks, the 3 shocks are occurring on overlapping but different timeframes.

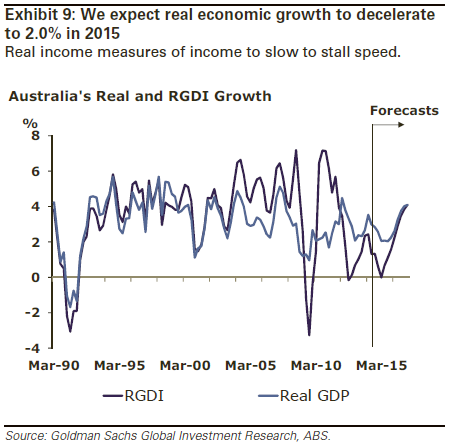

The income shock via commodity prices is now mostly behind Australia; indeed, iron ore prices are currently below our spot forecasts. Although key commodity prices may not fall too much further, the impact of these declines in spot prices on the terms of trade will still be apparent over the next 9 months and impact upon household income growth noticeable for another 12-18 months, if historical relationships again prove accurate.

The consequence is that a weakening in nominal GDP growth will become increasingly apparent as Australia enters 2015, presenting downside to inflation and wage outcomes. We estimate nominal economic growth in Australia will slow to sub-3% in 2015.

The investment shock from declining mining investment is only approximately 1/5th of the way through its adjustment. The long expected LNG-supply led boost to activity is still ahead, but there has been some further slippage in the timing of the production ramp-up into 2016 and the transition from falling investment to full production is likely to be a bumpy process. We estimate that mining investment will subtract 150ppts from real economic growth in 2015 and 100ppts in 2016.

The fiscal shock has only recently commenced. From 1 July 2014, the combination of a deficit levy tax, an increase in the Medicare levy, an increase in the superannuation levy and more recently the re-indexation of petrol excise was phase 1 of the fiscal tightening.

Restrictions to welfare entitlements and proposed co-payments for medical visits remain key elements of the May Budget still yet to pass the Senate and it appears that the Government plans to use an updated Intergenerational Report from Treasury to highlight why further budgetary reform will be required in the May Budget. With the declines in commodity prices set to strip over A$25bn from government revenue over the next 4 years and the lackluster nature of the non-mining economic recovery constraining income tax revenue, the government will likely need to raise A$30bn in new taxes or via expenditure cuts over the Budget horizon should it wish to continue to meet its existing objective of returning the Budget to surplus by 2018-19. We estimate that the fiscal drag will take 0.6% off real economic growth in 2015 and 0.4% off real economic growth in 2016.

In our 2014 Outlook report we wrote:

“The challenge of avoiding a harder landing in Australia is yet to be fully mitigated by a notable acceleration in the non-mining economy through 2013. Relative to the growth profile outlined in our 2013 outlook entitled “Passing the Growth Baton” the non-mining economy does not appear to have dropped the baton, however, it appears to be making slow progress in the initial transition phase. The headwinds of an elevated Australian dollar, ongoing fiscal drag, poor labour income dynamics and a declining terms of trade have weighed upon the non-mining economy’s recovery. Asset price growth, a recovery in home building and solid export volume growth are coalescing with loose financial conditions to provide some support. Nevertheless, it is the very slow transition that poses the central risk to the outlook, especially as the multi-year contraction in mining investment appears to have already commenced.”

While much of that text applies equally for 2015 there are 2 important qualifications. Firstly, the growth impetus from the new housing recovery is set to slow. Indeed, we flagged in our 2014 Outlook that our leading indicator for housing suggested new housing approvals would cease to expand by the end of 2014 without further monetary easing.

Unfortunately this forecast appears to have been realized, suggesting that although housing approvals may remain at a high level in the coming year the contribution to economic growth will progressively diminish. Given this has been the primary source of new non-mining economic growth in 2014, home building will prove less of catalyst during 2015.

Secondly, financial conditions can no longer be classified as ‘loose’. Although this may seem at odds with recent RBA statements, the RBA definition of financial conditions has narrowed during 2014 to focus on lending rates faced by business and consumers. Our definition is a broader concept that encompasses the currency, short term and long term interest rates, corporate bond spreads, asset prices and commodity prices. While it is commodity prices that have provided most of tightening in financial conditions in 2014 our measure of financial conditions excluding commodity prices also suggests that financial conditions have moved from ‘easy’ to ‘neutral’.

Thus into the most acute phase of the economic impact of these 3 key economic shocks in 2015 the 2 primary forces that have provided the impetus to economic growth in 2014 are fading.

Exactly right. Unfortunately I’m more bearish given I see iron ore at $50 by the end of next year. The rate cuts will come therefore and the falling dollar, but one still has to ask, with that kind of income and fiscal shock still brewing, what effect will they have and where on earth will that 2016 rebound come from?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.