From BofAML comes some fascinating thinking on the end of QE and equities:

After six years, the Fed finally exited QE last week. Given that investors have had more than a year to prepare for this event, the consensus is that this will have limited market impact. After all, long-term US rates have been falling this year even as the Fed began tapering its asset purchases

We beg to differ. In our view, the end of the QE could usher in a period of higher volatility and higher risk premium. Our view is predicated on three observations.

First, the dependency of financial markets on liquidity, if anything, seems to have grown this year.

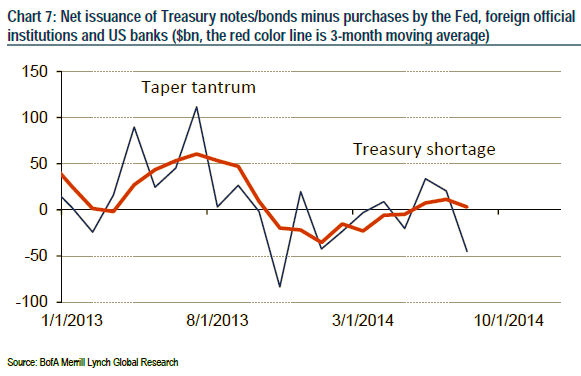

Second, the impact of Fed tapering was temporarily masked by increased Treasury buying by China and US banks that is now slowing.

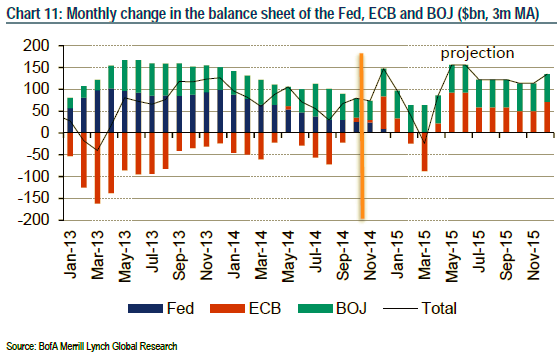

Third, it is unlikely that increased asset purchases by the BOJ and the ECB will be able to provide a full offset to the end of Fed purchases.

In our view, the end of QE has two important market implications:

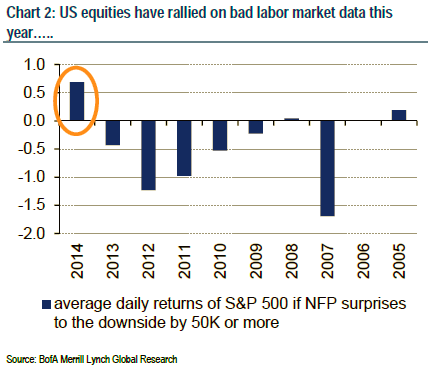

Bad news = bad news

Now that the Fed has officially exited QE, in our view the cost to the Fed to return to QE is considerable. We believe this means that things would have to get a lot worse before the market can count on the Fed to come to the rescue…If bad news is going to be treated by the market as bad news, this argues for higher volatility and higher risk premium.

Higher USD and higher correlation with equities

In many ways, the aggressive Fed easing over the past six years reduced the need for other central banks to ease policy. Now that the Fed has ended QE, the burden will fall on other central banks to do more. This is clearly very supportive for the USD.

I disagree. If Treasury yields start to climb simply on the basis of a rising risk premium absent the Fed, then the whole world is in deep shit. I don’t think this is the case.

Such a risk is more apposite over the very long term as the big surpluses of emerging markets decline (such as China’s “rebalancing”), but that will be accompanied by a corresponding lift in their domestic demand which will also raise developed market exports and activity, so is a functional rebalancing that can handle higher interest rates.

Advertisement

Likewise, we face the “euroglut”, with savings in the old world surging and looking for a home. Treasuries will see their fair share.

Aside from anything else, if bad news is to be bad news once more then bonds will find new buyers when trouble looms and inflation keeps sinking.

But if BofAML is right that the end of QE is the return of market risk premiums – which is a much more solid notion – then there is one other way it might happen: stock market prices could decline faster than Treasury yields do when bad news arrives.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.