In 1972 Zhou Enlai told Richard Nixon “it’s too early” to assess the impact of the French revolution. We need to be faster assessing QE: US QE will likely be back in the next US downturn, and other central banks are replicating the Fed’s balance sheet munificence. I think QE was over-rated: over-rated as an economic stimulant, and over-rated – but not completely ineffectual – as a market stimulant. To be fair, this debate may only be settled in the next downturn, when I expect QE will clearly fail.

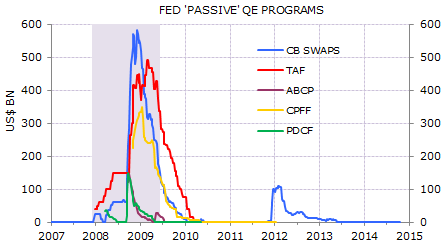

Two preliminary points about QE and the US recovery: First, the emergency liquidity measures after Lehman’s failure were critical. But these programs were not new-age monetary policy, they were classic Bagehot measures. They prevented potential depression. However, the measure of their success was their decline (Exhibit 1).