Australia’s strong growth in residential property prices over the past 18-24 months has triggered a growing debate around the heightened risk to financial system stability. In particular, the debate has centered on whether additional regulatory intervention in the form of so-called macro-prudential tools are required to stem the growth in property prices. Standard & Poor’s considers that a sustained and strong increase in property prices adds to the imbalances in the economy, in that it increases the risk of a rapid downturn in property prices, which could eventually destabilize the financial system and the broader economy. A post-application analysis on the implementation of macro-prudential limits in New Zealand and recent initiatives from the Bank of England and Central Bank of Ireland on their macro-prudential fronts have also contributed to the heightened focus on this type of policy tool as an adjunct to monetary policy to manage financial system stability.

While unconventional macro-prudential tools–such as limits on high loan-to-value lending–are still a work in progress within the developed markets, we believe a number of macro-prudential tools are both currently utilised and available to Australian regulators. The recalibration of prudential settings as a result of system-wide stress testing is one such tool. We believe Australian regulators will expand the use of macro-prudential measures to address the increased risk associated with strong growth in house prices, particularly with interest rates expected to remain low. We believe that strong property price growth is typically an indicator of increased risk, and the surrounding fundamentals of soft employment and anemic real wage growth heighten the risk, in our opinion. These conditions expose highly leveraged households with high gearing and debt-to-income ratios to loan serviceability challenges if interest rate increases and lower equity positions if property prices fall.

In Standard & Poor’s opinion, the focus of macro-prudential tools will be on ensuring Australian banks and households are well positioned to absorb any potential fallout from a rapid fall in property prices. To this extent, we believe any resultant retrace in residential property price growth may be viewed as a secondary outcome; we consider that strong growth in Australian residential property prices can be partly attributed to factors other than lending practices and credit growth and, to an extent, outside of the direct reach of prudential oversight. These factors include rising demand as a result of strong immigration inflows, supply constraints, and favourable tax treatment for residential property investment–which in-effect lowers the borrowing costs for these types of loans (see Australian Bank Ratings Holding Up As Cheap

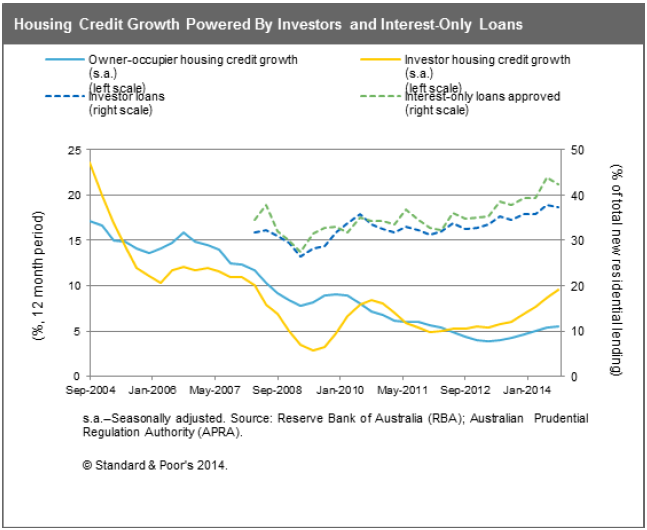

· In Standard & Poor’s opinion, it’s increasingly likely Australian regulators will look to address the growing risks to financial system stability stemming from strong residential property prices and investor lending demand by employing macro-prudential measures.

· We do not expect the application of macro-prudential measures, by itself, to have any immediate impact, either upward or downward, on our ratings on Australia’s financial institutions.

· Nevertheless, we believe application of macro-prudential measures could contribute to a dampening in emerging pressures on economic imbalances and credit risk within the Australian economy, reducing the potential risk to financial system stability by reducing the risk of a material fall in residential property prices.

· We don’t expect Australian regulators to introduce prescriptive measures, such as limits on high loan-to-valuation lending. Instead, we believe Australian regulators are likely to focus on increased capital requirements for residential mortgage lending and strengthened affordability requirements.

· We believe macro-prudential measures will trigger a slowdown in investor and interest-only residential mortgage lending, although we believe any resultant retrace in residential property price growth may be a secondary outcome.

So, S&P sees macroprudential slowing the marginal buyer in the market but no direct price impact…yeh, right.

Combined with the new foreign property regime, the coming crapola economy and the approaching end of the business cycle, the only conclusion to draw is: hit the bid, peeps!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.