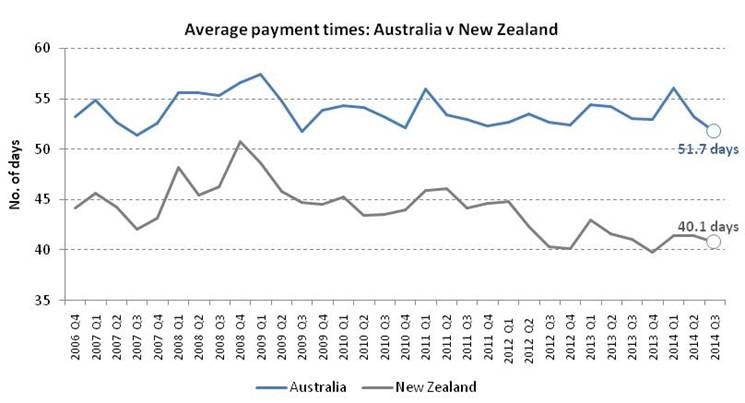

The average time taken for Australian businesses to pay their invoices has fallen to the lowest level since the third quarter of 2007, in signs that operating conditions have strengthened this year and the business sector’s cash position is improving.

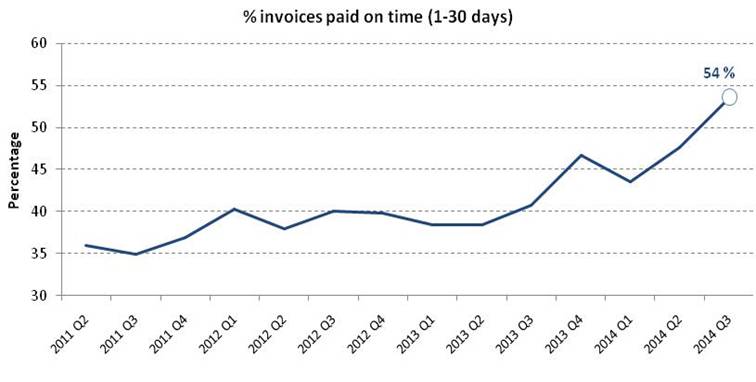

According to Dun & Bradstreet’s Trade Payments Analysis, businesses settled their accounts in an average of 51.7 days during Q3 2014, with the proportion of invoices paid within standard terms (1–30 days) lifting to 54 per cent.

According to Gareth Jones, CEO of Dun & Bradstreet Australia & New Zealand, the steady improvement in invoice payment times since the global financial crisis is reflective of a gradual recuperation in the business sector.

“While acknowledging some seasonality, these latest numbers should be read positively for corporate cash flow; with the average time taken for invoices to be paid reaching the fastest rate in seven years, and dropping to nearly a week faster than the 2009 peak,” Mr Jones said.

“Cashflow is on ongoing concern for businesses of all sizes, and a key factor in their ability to manage is the speed in which they get paid.

“This trend for faster payments is helping move money into the hands of business owners earlier and, in turn, helps them cover their expenses, pay their suppliers, invest in the growth of their business and more broadly, circulate more money in the economy.

“Despite this positive trend, at more than 50 days the Australian payment cycle is relatively slow; being 11 days later than in New Zealand,” Mr Jones added.

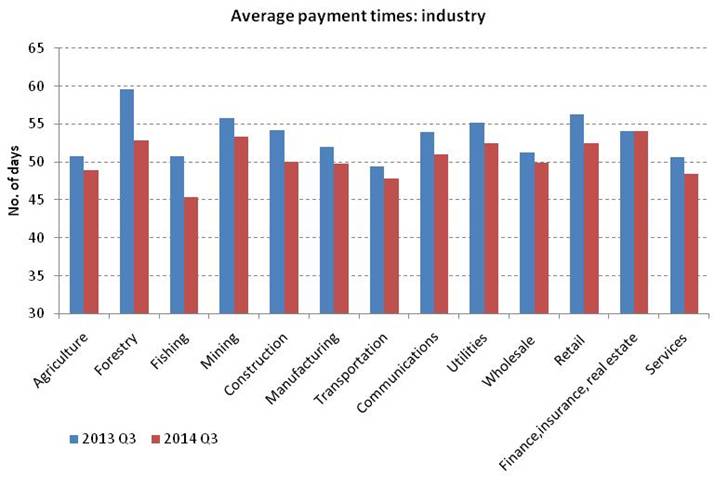

All sectors included in D&B’s Trade Payments Analysis saw improvements in the time taken to settle invoices, with the fishing industry paying bills the fastest, at an average of 45.4 days, down from 50.8 days a year earlier. At 48.4 days, the services sector was the second fastest to pay its invoices, followed by the agriculture industry at 48.9 days.

Businesses operating in the finance, insurance and real estate sector were the slowest to settle their accounts, taking an average of 54 days; a flat result compared to the year before. At 53.3 days, the mining industry took the second-longest amount of time to pay its invoices during the third quarter of the year.

Despite a late-paying mining industry and signs the economic performance in Western Australia is slowing, businesses operating in the west recorded the fastest average payment times (48.2 days), followed by South Australia (49.4 days) and the Northern Territory (49.6 days). The ACT was the nation’s slowest paying region, at an average of 54 days, followed by New South Wales (53.9 days).

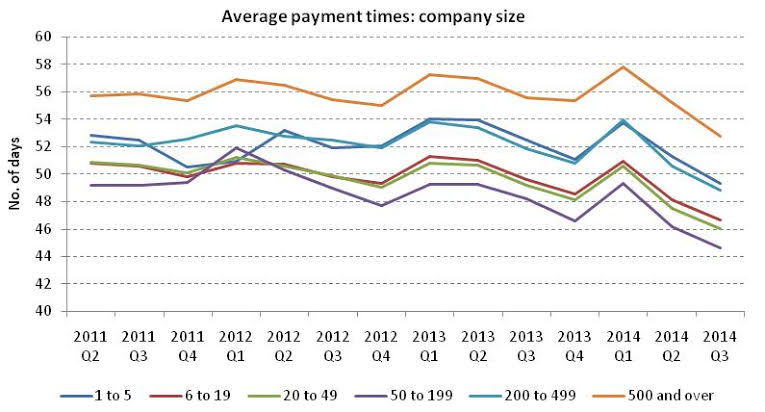

Across the country, big business continued to take the longest time to pay invoices. Despite a three-day improvement on Q3 2013, companies with more than 500 staff made their payments in an average of 52.8 days. The fastest were those businesses with between 50–199 employees, which paid their bills in an average of 44.6 days.

According to Stephen Koukoulas, Economic Advisor to Dun & Bradstreet, the trade payments data suggests that business cashflow has improved.

“The time taken for firms to pay their bills has dropped to a seven-year low, with the proportion that pays on time increasing to 54 per cent. This indicates that low interest rates and favourable underlying economic conditions are providing support to business finances.

“The Trade Payments Analysis suggests the RBA is still some way from adjusting interest rates as it juggles good news from the corporate sector with uncertain global conditions and signs of rising financial stress from consumers,” Mr Koukoulas added.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.