Negative catalysts continue to circle the domestic property market making for a rather surreal backdrop. The sharpening of FIRB’s ‘teeth’, along with pending curbs on investors and (emerging) curbs on interest-only loans for owner-occupiers are likely to continue to see the market soften.

Impact

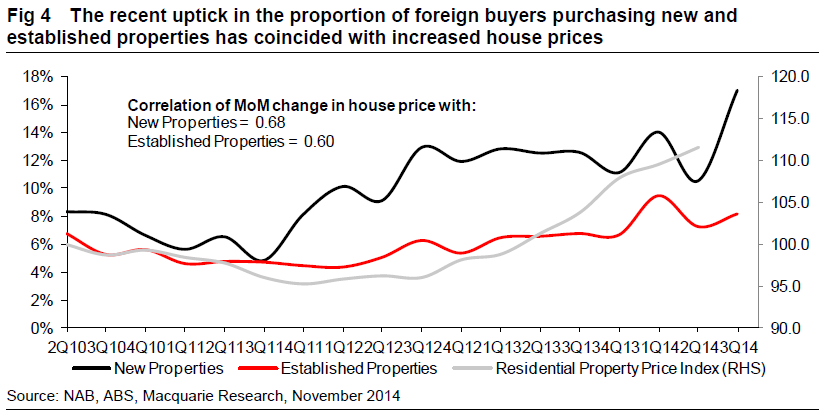

Kelly O’Dwyer’s Report on Foreign Investment to give FIRB sharper teeth – The much-awaited O’Dwyer report was released today. There will be a national land register that records citizenship, which will be cross-referenced with various Government data (Immigration, etc) that will ensure that visaholders who leave the country sell their properties. FIRB will also get more resources, funded by a modest administration fee of $1500 per FIRB application. A civil penalty regime has been recommended, which will apply to not only the offenders but also those that aid breaches of the law – real estate agents and banks could have to pay as well. Penalties will be directly related to the value of the property concerned, thus addressing the view that current fixed fines are ‘a cost of doing business’. All this, if adopted (hard to see why it wouldn’t be), will aid the cooling of the property market currently in train.

RBA reinforces risks it’s seeing in property markets zeroing in on Interest Only (IO) loans – The RBA continues to warn about the risks present in the Sydney/Melbourne property market, with the latest report focusing on the inherent risks in interest-only loans (Philip Lowe, ABE Dinner) for investors. No doubt the FSI will discuss the tax incentives that drive this dynamic and why IO loans are riskier (flagged by the RBA a number of times).

In our view, IO loans also represent, for the owner-occupier at least, a form of reset loan (similar to those that caused havoc in the US) with owners givenlong-term ‘honeymoon’ repayments, only for this to revert to much higher levels when the principal must be paid down over a shorter period (or the can is kicked down the road via a refi). In the presence of rising rates and/or income pressures, this situation could become quite toxic.

We believe macro-prudential may focus on interest-only restrictions for Owner Occupiers as well – As suggested by our economist, the introduction of macro-prudential may be a precursor for rates heading substantially lower from here. We’ve flagged the risk that investors may have to pay more for their loans and/or experience a greater ‘buffer’ interest rate on their serviceability calculation. We believe there is also a chance that there is measured action against interest-only loans for owner-occupiers.

Outlook

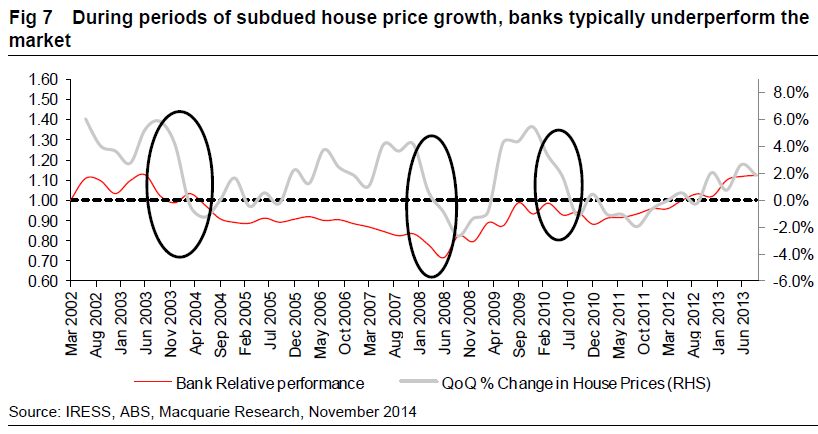

Given the RBA’s impending intervention in the Sydney/Melbourne property market as well as a tightening up of FIRB’s policing arrangements, this will likely put pressure on the domestic property market. This will likely lead to a period of subdued house price growth and in recent times, during these periods, banks typically underperform the market.

And that, my friends, is all she wrote. Add the coming end of the global cycle (in the next two years or so) and you will begin to fathom why I say “hit the bid”.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.