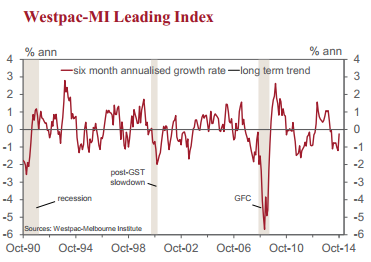

• The six month annualised deviation from trend growth rate of the Westpac Melbourne Institute Leading Index which indicates the likely pace of economic growth three to nine months into the future rose from –1.20% in September to –0.25% in October.

This is the ninth consecutive month where the growth rate in the Index has been below trend. That follows thirteen consecutive months to February this year when the growth rate was above trend. The index continues to indicate that we can expect growth in the Australian economy to stay below trend in the final quarter of 2014 and into the first half of 2015. However the near 1ppt improvement in the negative deviation, on face value, gives some cause for optimism that momentum might be lifting sometime in the June quarter.

An improved growth profile is certainly consistent with Westpac’s own view of certain key sectoral dynamics. For instance, we expect that the pace of consumer spending growth will pick up from a 2% annualised pace in the first half of 2014; to 2.8% in the second half and 3.5% in 2015.

Similarly we expect a lift in nonmining equipment investment growth from a modest contraction in the first half of 2014 to around a 6% annualised pace in the second half of 2014 and 8% in 2015. On the other hand residential investment will be flat but largely maintain the high levels of activity which have recently been achieved.

Strength in those components of activity is very important for the labour market. Under the above scenario we expect the unemployment rate to be edging down through the second half of 2015 to around 5.9% by year’s end.

Overall we expect Australia’s growth rate in 2015 to reach an above trend 3.2% despite a larger drag from mining investment.

Over the last six months the index’s growth rate has remained at a below trend growth pace. In May, when the Index’s growth rate was 0.75% below trend, the key drivers were: the Westpac –MI Consumer Sentiment Expectations index (–0.23ppt’s); the RBA commodity price index in AUD (–0.41ppt’s); the yield curve (–0.19 ppt’s) and dwelling approvals (–0.17 ppt’s). Offsetting those negative effects were US industrial production (+0.22ppt’s).

The Westpac MI UE index; monthly hours worked; and the ASX 200 had minimal impact on the growth rate.

In October the growth rate in the Index lifted a little to be –0.25 ppt’s below trend. The major contributors are still: commodity prices (–0.44ppt’s); the yield spread (–0.32ppt’s); and dwelling approvals (–0.10ppt’s). Offsetting those drags on growth are aggregate monthly hours worked (+0.33ppt’s); US industrial production (+0.10ppt’s) and the Westpac – MI CSI expectations index (+0.14ppt’s).

One word of caution with this month’s print on the index is around the “aggregate monthly hours worked” series. That series moved from subtracting 0.35ppt’s from the growth deviation in September to adding 0.33ppt’s in October. Of course any “noise” around series associated with the ABS’ Employment Report during that period looks suspicious. Indeed by smoothing out that “effect” it might be more reliable to consider that the deviation from the trend growth rate “improved” from –1.03 ppt’s in August to –0.85ppt’s in September and –0.58ppt’s in October – a more modest improvement but still indicating an improving trend.

We do not expect to see the Reserve Bank changing rates until well into 2015. Indeed, the minutes to the November Board meeting again confirmed the Bank’s intentions for a period of stability in rates. Westpac expects that, with improving growth momentum in consumer spending; non mining business investment; and the labour market , the next move in rates will be a tightening but not until the second half of 2015, with August currently appearing to be the date for the first move.

Buckley’s, Bill. With a 2015 iron ore forecast at $120ish, our Bill is in the wrong ballpark. It will be half that in August 2015 and rate rises will the last thing on anyone’s mind.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.