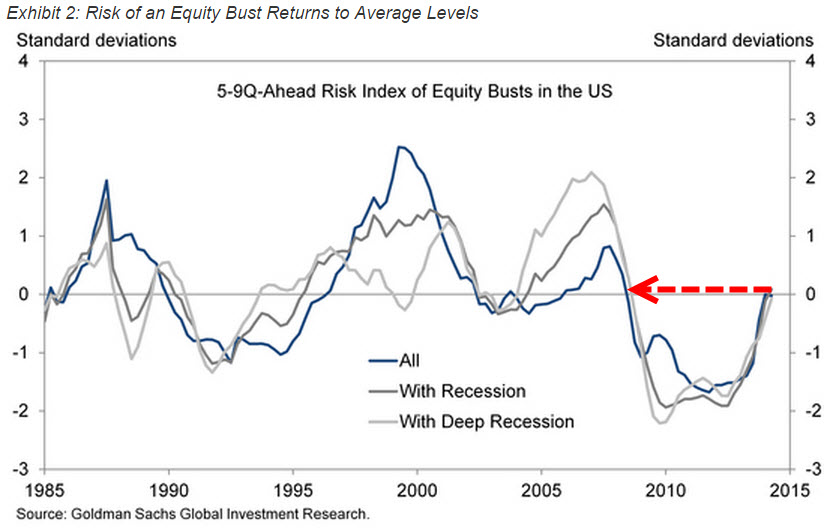

Earlier this year, we presented an analysis of the predictability of equity and housing market busts in advanced economies, focusing particularly on asset price downturns that are associated with a recession. With stocks back to near-record levels, it may be a good time to revisit that analysis.

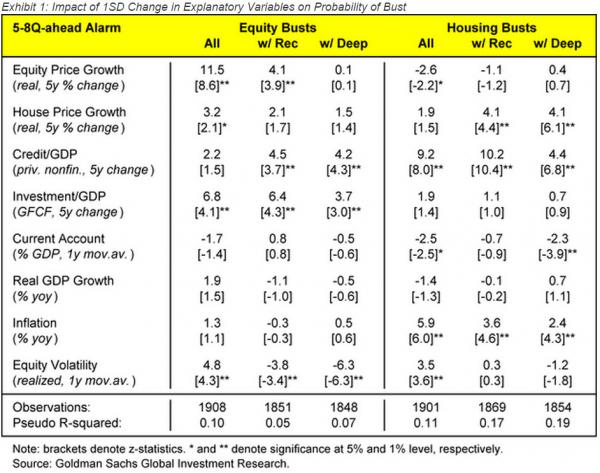

To recap,our analysis uses quarterly data for 20 advanced economies on house prices, equity prices, and a set of economic and financial variables that have been found to correlate with the risk of future busts.We define an equity bust as a year-to-year decline in the quarterly average of real equity prices of at least 20%, and a housing bust as a decline of at least 5%. If the condition for an equity or housing bust is met in quarter t, we date the crisis as having started in quarter t-3. A recessionary bust is defined as a bust that involves a year-to-year decline in real GDP either in the same quarter or up to four quarters later. A deeply recessionary bust additionally requires that the year-to-year decline in real GDP exceed 2%. Our empirical analysis then tries to identify economic and financial variables that predict–or generate and “alarm”–for a bust 5-9 quarters later.

Exhibit 1 shows that the single most important predictor is past equity price appreciation, followed by a rising investment/GDP ratio and high equity volatility. Our interpretation is that many equity busts are simply the counterpart of prior periods of strong price appreciation, and in this context it is not surprising that big moves downward are more likely when volatility is high. The sizable effect of a rising investment/GDP ratio may reflect a negative impact from excessive capital spending on corporate profitability or the broader dangers posed by an unsustainable homebuilding boom.

…The expansion has already lasted longer than the median expansion historically, but we still seem to be quite far from the overheating or financial imbalances that historically precede most US recessions.

Thus, we expect the current expansion to last longer than average and view the risk of recession over the next few years as fairly modest.

Just so long as equity prices don’t keep rising that is…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.