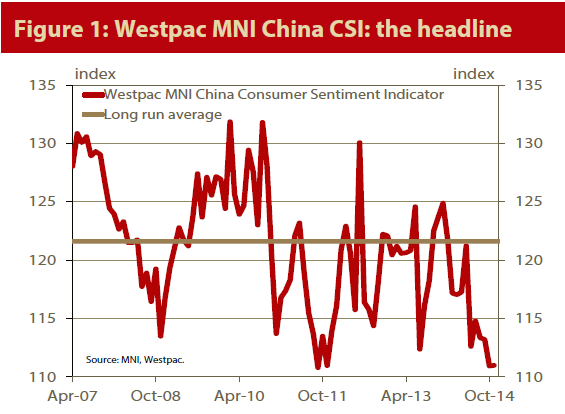

The Westpac MNI China Consumer Sentiment Indicator, hereafter the Westpac MNI China CSI, was essentially unchanged in November, printing 111.0 versus 110.9 in October, a +0.04% change over the month and –10.3% over the year. The November outcome is 8.7% below the long run average. The survey indicates that the anxieties that have been gnawing away at the Chinese consumer throughout the year remain in evidence. However, there are some tentative signs that the dominant themes of late – pronounced pessimism regarding the housing and labour markets – are shifting in a more favourable direction.

• Four of the five components that go into the calculation of the Westpac MNI China CSI improved from the previous month. Current and expected family finances moved higher, by 0.8% and 1.3% respectively, while ‘time to buy a major household item’ increased by 1.9%. ‘Business conditions one year ahead’ were the weakest link in November, down a striking 4.1%, with the ‘five years ahead’ index up 0.6%. Current business conditions (not a part of the headline composite, but tightly correlated with official industrial production data) declined narrowly. Consumers seem to be unimpressed with the state of the economy generally, but they are somewhat more positive with respect to their own finances. This apparent inconsistency is due to a perception that inflation is less of a ‘tax’ at present; in addition to the aforementioned shifts in job and housing sentiment (discussed in more detail below).

• The employment indicator has been weak from June through October, during which time it presented a watertight case that the policy support for growth should be strengthened. The downtrend was finally broken this month, with a welcome 4.7% gain. However, the indicator is still 12.4% lower than a year ago, implying absolute job security remains in short supply.

• The consumers’ attitude towards real estate showed signs of improvement in November, with favourable directional shifts across a range of measures, although to be fair the scale of the moves are small. Expectations for house prices broke a string of four declines dating back to June; the share of respondents reporting it was a ‘good time to buy a house’ rose a little, while 17.0% of consumers now nominate domestic real estate as the ‘wisest place for their savings’, up from 15.6% in October. The exception to the trend of improvement was that the proportion of consumers nominating a housing purchase as their primary motivation for saving fell again. This slightly more optimistic overall appraisal of the housing market is an extremely welcome development, as it indicates that the September 30 policy support package is beginning to gain some traction following a lukewarm initial reception in October.

• Overall, the tentative consolidation evident in this survey is consistent with our view that growth bottomed out in late Q3. In addition to the more positive housing data coming from other sources and the symbolic import of the interest rate cuts (which post-date this survey), we argue that the distribution of risks regarding the 2015 outlook are more balanced than the pessimistic rhetoric of the analyst community would suggest.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.