Fresh from our Bill at Westpac:

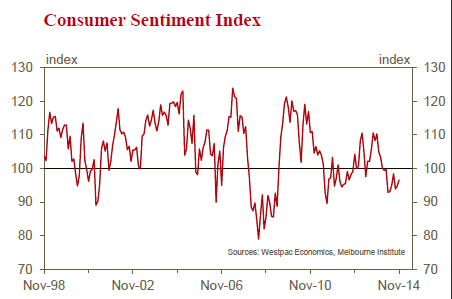

• The Westpac Melbourne Institute Index of Consumer Sentiment rose by 1.9% in November from 94.8 in October to 96.6 in November.

This is an unsurprising but still disappointing result. The Index is 12.5% below its level of a year ago and 3.6% below its level before the lead up period to the Commonwealth budget in May. In fact, we have now seen nine consecutive months where pessimists have outnumbered optimists.

That is the longest run of pessimists outnumbering optimists since the Global Financial Crisis and before that the recession of the early 1990’s.

The modest increase in the Index may be attributed to more positive news on the financial markets. The Australian share index has lifted by an impressive 5% since the last survey, while the Australian dollar has stabilised following its 7% plunge in September. The Reserve Bank’s decision to hold rates steady came as no surprise with households generally comfortable that low interest rates are likely to persist for some time.

News on housing continues to be positive. Although price appreciation has slowed, auction clearance rates are high.

Households will not have been impressed by the confusing news around the official employment reports. Following major data revisions from the Australian Bureau of Statistics the unemployment rate was revised up from 6.0% to 6.2%. Previous assessments that the unemployment rate may have stabilised around 6% have now had to be reconsidered.

That disappointment is likely to have impacted the Westpac – Melbourne Institute Unemployment Expectations Index. The Index increased by 2.7% in November (a higher print indicates that respondents are more pessimistic about the labour market).

That result is particularly disappointing given that it followed a promising fall of 3.9% in October. This Index is now 5.5% above its level of a year ago and 17.2% above its level of three years ago when the Reserve Bank started its most recent cycle of rate cuts.

The components of the Index which assess the outlook for the economy both increased. As discussed, that improvement probably reflects the recent increases in share markets; the associated positive economic news from overseas; and the stability in the Australian dollar. “Economic conditions next 12 months” increased by 10.8% while “economic conditions next 5 years” was up by 2.1%. Respondents’ assessments of their own financial position were mixed.” Family finances vs a year ago” fell by 4.2% whereas “family finances next 12 months” rose by 3.1%.

Confidence around the future relative to assessments of the last 12 months are quite different. The future outlook component is broadly steady on a year ago whereas the assessment of finances compared to a year ago has fallen by 15.7% over the year.

The November Consumer Sentiment Index is watched closely as a lead indicator for prospects for the Christmas selling season.

In that regard the 0.8% fall in the component “good time to buy a major household item” is disappointing particularly given that this component is now down by 13% over the last year.

There is further disturbing news on prospects for the Christmas season. Since 2007 we have asked the following question in November. “Do you think that you will spend less, about the same, or more on Christmas gifts compared to last year?” For this year 38% registered “less”; 50 %, “same” and 12% “more”. The net balance (more minus less) of minus 26% is the worst since 2008 (minus 34%) which was in direct response to the Global Financial Crisis. Over the subsequent five years the net balance has been tightly clustered around minus 22% so the result for 2014 is a marked deterioration relative to the last five years.

Prospects in the housing market improved in November. The Index, “Whether now is a good time to buy a dwelling” increased

by 3.1%, although it is still down by 13.3% on a year ago. House price expectations increased in the month by 1.4% but this index is still down by 14.3% over the year. Most of this fall has occurred since September. Up until then expectations were fairly solid but over the last two months the Index seems to have established a base which is down by around 10% since September.The Reserve Bank board next meets on December 2. Rates have been on hold since August last year. We can confidently expect that rates will remain on hold at the December meeting. For most of this year Westpac has been of the view that rates would not be increased until August 2015.

Critical to that view is a lift in consumer spending which in turn will encourage businesses to invest and employ. The Consumer Sentiment Index has lifted modestly from its post Budget lows but the pace of improvement has been very disappointing. Strengthening balance sheets and an improving world economy are likely to be key to further recovery in Consumer Sentiment. However, in the near term, prospects for a boost in consumer spending going into the end of the year are not encouraging.