I won’t be too hard on the latest from “Mad” Adam Carr because it makes at least one good point when looking at the Aussie:

There’s been a lot of celebration about the weak Australian dollar recently — especially from the tourism and education sectors. Unfortunately, much of it is extremely premature…

Key to that is the rapid appreciation of the Australian dollar against the yen and the euro, which together account for just under a quarter of the basket. The dollar is up over 9 per cent against the yen this year and 8 per cent against the euro. Otherwise, and against our other major trading partners, the Australian dollar has been steady.

Under current circumstances, that stability would appear to be one of the best scenarios that we could hope for. There’s certainly not a lot on the horizon that points to a weakening currency. Indeed, news yesterday that Japan had entered another recession — the fourth in about five years — makes it extremely unlikely…Japan will probably print even more money.

The pressure on the Australian dollar to appreciate is strong. The question is, what, if anything, the RBA is going to do about it.

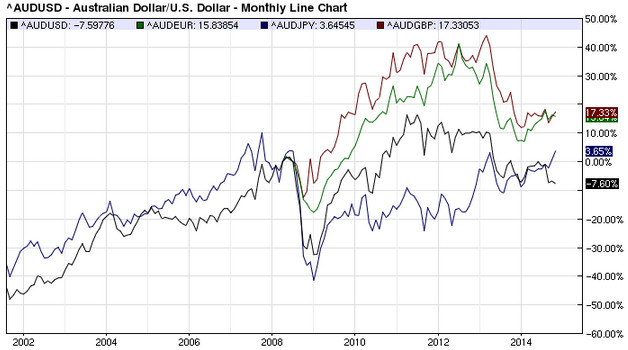

To the charts, which really do reveal Carr’s biases. Here’s the Aussie versus developed market economy currencies:

As you can see, if you don’t cherry pick your data, the Aussie remains in broad downtrends against everyone except the Japanese yen. Certainly the US dollar appears the most convincing weakness but the GBP and EUR aren’t tearing it up against the Aussie even if they are falling more slowly. However, he may well be right about the Euro if it prints.

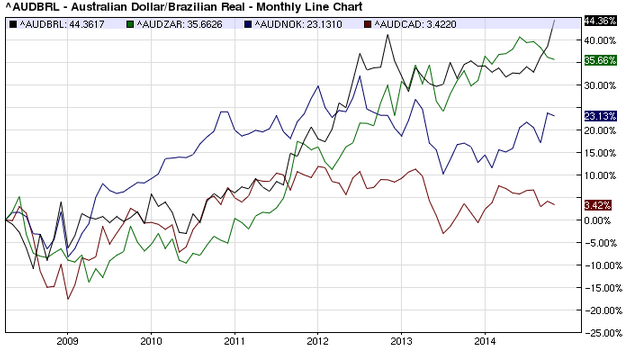

Moreover, against the developing market and commodity producer basket, the Aussie looks much less weak:

Against Norway and Canada it’s a shaky downtrend but against direct bulk competitors in Brazil and South Africa the Aussie is rising strongly and, needless to say, putting Australian production at a severe disadvantage in the global market share battle now underway.

In “mad” Adam’s world Australians don’t need to compete for anything and there is no issue with debt, so simply expanding domestic spending via leverage ad infintum is both possible and awesome, and the resulting purchasing power for households rocks.

In the real world, his point about Aussie strength against the crosses is doing real and lasting damage to the export economy as we rise ever closer to peak debt.

And that’s what can be done about it. Stop the debt rising with firm macroprudential then cut interest rates and join the global currency war.