I have to commend a letter to the editor in the weekend Financial Times from a Matt Long. He clearly identifies current conditions as entirely consistent with the top of the bubble. This is the sort of incisive analysis that is often so lacking in our industry,

Sir: The next financial apocalypse is imminent. I know this to be true because the (FT Weekend) House and Home section is now assuming the epic proportions last seen before the great crash. Twenty four pages chock full of adverts for mansions and wicker tea trays for $1,000. You’re all mad. Sell everything and run for your lives. Matt Long, Seilh, France.

…What I have never really been able to understand is why vol only rises when the market declines. But the chart and maths tell me that markets must rise in a smoother way than they decline the latter being violent and often disorderly as years of gains are often wiped out in a few months.

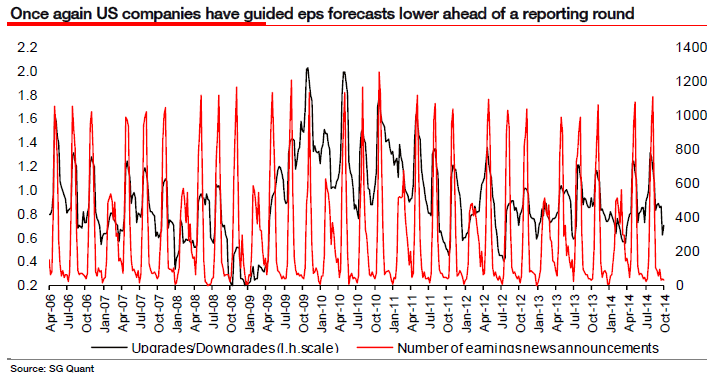

I was chatting to my former colleague Helen Thomas who writes in her Blonde Money blog how volatility is eating itself, i.e. the rise in FX volatility is feeding into higher equity market vol. Helen believes that the missing part of the puzzle has been bond market vol, which has been relatively well behaved. It remains the overwhelming view of the market that US bond yields will rise see for example “Stick with consensus and sell Treasuries” link. I discussed with Helen whether bond vol may indeed rise sharply, but in a way that equities never seem to do in line with prices on the upside as higher FX vol sends equity prices lower. Blonde Money also points out a short study by the New York Fed which notes that when markets watch one another, this can cause volatility to propagate. This reminds me of one of Andy Lapthornes constant refrains in presentations, namely that corporate bond spreads are a function of VIX via the Merton Model. Again I have no idea what he is talking about except that there are a set of dominos out there and when they start falling the whole lot could come tumbling down. Of course a key prop preventing this cataclysm remains the US economy probably the only region where investors still have confidence in a self-sustaining recovery. On that vein we are entering a potentially very tricky US reporting round. US companies have been playing their usual games in the run up to the reporting season by ramping down eps expectations so they can beat the numbers on the day (see chart below).

According to Factset, analysts Q3 forecasts have been sliced from 9% yoy growth at the start of July to 4.6%. Thomson Reuters numbers are a bit higher, with Q3 2014 eps growth expectations having been lopped from 11% on July 1 to 6.4%. But will this be enough in the light of recent substantial dollar strength? Thomson Reuters notes that the Q3 downward ramp is not substantially different from the long-term average decrease of 4.0% in the three months before a reporting round (since Q2 2002). Maybe they should have done a bit more!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.