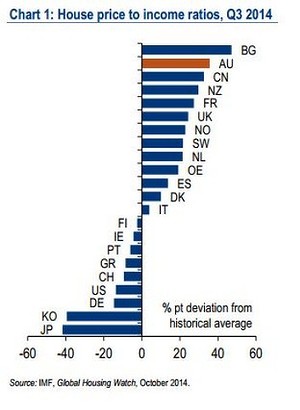

From the SMH blog, here are Saul Eslake’s six reasons for the property bubble:

• First, research suggests homes in cities with populations of over 1 million tend to attract a premium, and the “proportion of Australians living in cities with populations of over 1 million is higher than in anywhere else in the world, apart from Hong Kong and Singapore”.

• Second, Aussies cities are spread out, and public transport and arterial roads in the outer suburbs are “generally inadequate”. Hence city dwellers prefer to spend more on housing to live nearer the centres of work to cut commuting time.

• Third, our properties are bigger than other countries.

• Fourth, we have become a lot richer over the past two decades. And rich people like expensive housing.

• Fifth, we have a shortage of housing. Supply has not kept up with our relatively large immigration intake.

• Finally, Aussies are more likely to invest in housing than other populations thanks to “substantial incentives” from the tax system.

Eslake adds that all this doesn’t mean house prices are set to rise further, or that they are likely to fall, although he notes that to see a decline “it would require a combination of circumstances that are difficult to envisage occurring any time soon”.

Apologies for another housing bubble post today . It’s not me! Anyways, my riposte is:

First, the “cities attract a premium” argument makes no sense when you’re surrounded by huge quantities of land with nobody living on it. I mean, ask yourself, a premium to what? It’s absurd to compare Australian cities with Hong Kong or Singapore on that basis. Saul’s point should be that the supply side is choked by constipated planning rules rendering the land mass redundant.

Second, sure, but that’s self-fulfilling. Bidding up house prices close to the city has priced Australia out of many tradable industries that used to occupy the suburbs, as well as exaggerating the importance of finance as a growth driver, pushing more people to live near the city where the finance jobs are. It’s not about infrastructure, it’s about macroeconomic settings.

Third, high valuations relative to income make the size of the house irrelevant.

Fourth, we may be richer but that does not imply high property prices. See Germany. The high prices are a result of investment incentives.

Fifth, yes.

Sixth, yes.

Advertisement

In short, many of the allegedly natural reasons for high house prices are no more than an expression of the bubble’s size and spectacular public policy support (none of this is meant as having a go at Saul who is one of the few to make that very point).

As for any reversal, lets see how we go when we lose the AAA sovereign rating and the major banks are all downgraded during the next global bust with monetary policy exhausted at 1.5%.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.